You are currently browsing the monthly archive for April 2011.

Tyler Cowen reposts the question

Have you ever forgone health insurance for yourself to cover your pets?

I don’t know about forgone per se. However, for a few years my dog had health insurance and I did not.

I ultimately got rid of the pet insurance not because I didn’t get vet services but because filing the claims were too complicated.

At heart my consumption of Vet services was a asymmetric information problem. I felt comfortable managing my medical care and refusing much of what doctors would offer. However, I could not talk to my dog. Sometimes she would yelp in pain and I wouldn’t know what was wrong.

Taking her to the Vet was sometimes the only way to find out.

I had an offline discussion with Matt Yglesias that prompts this critique of Bryan Caplan’s basic thesis. Bryan seem to be saying – I haven’t read the book though I have followed his discussion of the idea for years – that knowing that your kids future isn’t dependent on you doing everything just right should make you want to have more.

What is it about downward sloping demand that you disagree with, I think I have heard Bryan say.

Well lets look at a more complete model where the demand for kids is itself a function of your control over what your kids will become and what Bryan is really talking about is the marginal cost curve for raising kids.

Lets build an ultra simple framework where you have only two models you can ascribe to. In the first model your parental efforts influence what type of kids you wind up with and you always want to set effort to HIGH. In the second model your parental efforts don’t matter and you always want to set effort to LOW.

The supply and demand in these two cases look might like this

How plausible is this? Well, perhaps not implausible at all if kids are a status marker. If a big part of what modern upper-middle class parents get from their kids is bragging rights then a full acceptance of Bryan’s thesis might decimate their demand.

In this vision of the world kids are just one more area where driven parents get to “win.” If they do all the right things then they can show off how much better their kids are than the neighbors. Yet, what if there is no winning? What if kids just are who they are?

Then even if the cost is lower the net benefit for competitive parents might collapse. I’ve drawn smooth supply and demand curves but this is for the aggregated market. In reality we would imagine a lot more parents defaulting to zero once they know that there is no status gain to be had from their kids.

Note that this might be a happy story. Consumer surplus increases because parental effort collapses. The parents are better off knowing that what they do won’t matter. Yet, it doesn’t make them want to have more kids.

There are worse things than inflation and we have them

~James Tobin

From the NYT

Using more comprehensive data to nail down economic trends, the new study found a clear correlation between suicide rates and the business cycle among young and middle-age adults. That correlation vanished when researchers looked only at children and the elderly.

Jim Manzi writes on the Krugmanesque Nostalgia

I’m somewhat younger than Krugman, but as they say, the future arrives unevenly. I grew up in a small town with an experience not unlike this. I’m very sympathetic to Krugman’s choking nostalgia. It’s difficult to convey the almost unbearable sweetness of this kind of American childhood to anybody who didn’t live it.

The safety and freedom that Krugman describe are rare now even for the wealthiest Americans – by age 9, I would typically leave the house on a Saturday morning on my bike, tell my parents I was “going out to play,” and not return until dinner; at age 10, would go down to the ocean to swim with friends without supervision all day; and at age 11 would play flashlight tag across dozens of yards for hours after dark. And the sense of equality was real, too. Some people definitely had bigger houses and more things than others, but our lives were remarkably similar. We all went to the same schools together, played on the same teams together, and watched the same TV shows. The idea of having, or being, “help” seemed like something from old movies about another time.

Almost anybody who experienced it this way (and of course, not everybody did), intuitively wants something like it for his own children. The tragedy, in my view, is that, though we all thought of this as the baseline of normality, this really was an exceptional moment in our nation’s history.

To but a negative spin on it: what both Paul and Jim hate is freedom.

I say this because I want people to understand why so many people around the world hate freedom and why they probably do to.

A free society is one where these is enormous opportunity for expression and technological advancement, but is that anywhere in these descriptions of childhood Eden? Or is Eden comprised of shared experienced, certainty, stability, safety and a feeling of commonality with your fellow man.

Is this version of Eden in an Iphone, a Prius, a 200 mph train? Is it in modern art or spoken word? Is it found on the pages of the Nation or the National Review? Can you get it on 500 channels of cable TV? Is it more deeply felt when you believe the President is an honest hero or when you find out that like all men, he lies when he feels he can get away with it.

Is Eden in the constant dynamism of an economy in which you make make twice the median income one year, but may be unemployed the next. Is it Eden when criminals you though were guilty go free or when murders are swiftly brought to justice. When DNA evidence leaves you wondering where the real killer might be, does Eden feel more or less real.

What this highlights and what’s so important about our modern world is that people often have more intense preferences over their beliefs about reality than reality itself. A society that constrains them, that lies to them, that oppresses them in so many tangible ways but leaves their cherished beliefs untouched may be a society that they love.

We are quick to assume that men would rather trade al of this away for their freedoms, economic and social. Yet, how many bemoan the crushing poverty we all experience in relation to what most humans are likely to experience.

Unless things go wrong before even I suspect, the vast majority of people will live lives much wealthier than ours with cultural and social opportunities we can scarcely imagine. Yet, few begrudge them.

While there are always a few tortured souls, constrained by society and the state, most people do not know what they do not know. They are a reflection of what they see in their family and friends.

The ever widening diversity of human experience and our ability to connect to people everywhere will mean that that reflection is more and more tailored to what makes you, you.. The fetish that you didn’t even know you were repressing will become your great great granddaughter’s afternoon diversion.

Every part of the human experience is set to expand. Yet, where in that is Eden? Are, the inhabitants of Jim’s small town or Krugman’s Long Island sad that they will never know such things? Or are they happy in their world, infinitely smaller than what stretches out before a dynamic human race.

I have always been a stranger in strange land. My childhood is not full of the happy memories that Jim and Paul express. It is full of bullies and taunts and neither teachers nor parents who understood. Some of my best memories are of an escape into the world of ideas and freedom from the incomprehensible world of other people.

From Ezra Klein

Tom Gallagher, a fiscal and monetary policy specialist at the Scowcroft Group, e-mails to say that I’ve been too harsh on Ben Bernanke, and his rhetorical emphasis on inflation is a way of buying time and political space to ignore inflation . . .

The chart he’s talking about tracks the index for dollar futures, which fell on Wednesday. I couldn’t get Gallagher’s out at a sufficiently high quality, so I snagged a 5-day track from marketwatch.com. As Gallagher says, the index falls around the time of Bernanke’s speech, suggesting the market heard less about inflation than it had hoped

I am not sure about this. I want to take time to go through the testimony word-by-word and do some analysis but one thing I can tell you straight from memory is that Bernanke’s bit about the dollar was embarrassing for every economist listening. That could have had an effect.

I don’t mean that as a “dis” of Bernanke’s knowledge. Its just that his actualy words were so vacuous as to border on deception. He passed the buck to Tim Geithner’s whose dollar policy, everyone knows, consists of repeating the phrase “The US has a strong dollar policy” while simultaneously trying to convince other central banks, to weaken the dollar.

Then Bernanke ran the tired line about the US having the deepest and most liquid capital markets in the world. Yeah, the dollar was surging just as the US capital markets were on the verge of imploding, the overnight rates were spiking out of control and Wachovia literally could not float commercial paper to save its life. Liquid capital markets, that’s what was going on? Really?

That was flight to Treasuries, pure and simple.

The problem is that doesn’t make sense to many observers who are attached to the view that the US is in fiscal crisis. The idea that US bonds are what you buy when you are scared is hard for them to square.

In part, because they have false beliefs about the actual state of US finances and in part because they misunderstand the concept of existential risk.

However, rather than go into that Bernanke spun the issue. Again, I have done the same myself, especially when I’m in the room with business folks and I don’t have a lot of time.

Though, I do enjoy saying “If you are selling Treasuries then what are you buying? Ammunition and Water Purifiers?”

However, that line often doesn’t go over well with a certain class of business folks who are under the mistaken impression that all of them can simultaneously run to gold despite the fact that only 5 billion ounces have ever been mined in all of human history and over half of that is currently being used as jewelry.

Arnold Kling refers to Soros’s talk yesterday at Cato

Soros framed the choice as one of believing that markets always work or believing that markets sometimes fail and therefore we need government. Afterwards, a few people said to me that they wanted to intercede with the line "Markets fail. That’s why we need markets."

The Masonomic taxonomy is:

- The Chicago school says markets work so lets use markets

- The Cambridge School says markets fail so lets use government

- The George Mason School says markets fail so lets use markets

I have tried to push the notion that sometimes markets and government simultaneously fail, so lets get drunk. A higher status interpretation might be the serenity view. One of my favorite expressions of it

For every ailment under the sun

There is a remedy, or there is none;

If there be one, try to find it;

If there be none, never mind it

Whether bad things are happening is in-and-of-itself of no consequence. Whether we have the power to make things better, whatever their current state, is everything.

Brad Delong offers a playfully cheeky response to my GDP decomposition

However, there are some important things I want to highlight. Looking at Personal Consumption and Industrial Production, the US experience seems to be increasingly diverging from the disaster that was Japan.

I am by no means averse to the US-Japan comparison. I employed it many times in the early days of the crisis. Yet, whether the comparison is no longer apt because of deft Fed policy or because it was never apt to begin with, the point remains: the US is diverging from the Japanese Scenario.

This is not to say more cannot and should not be done. It is to say, the “extraordinary measures” employed by the Fed look to have done something, if still not enough.

Here are retail sales growth in the years leading up to and right after the Japanese asset bubble burst

Here is the same series for the US

Here is total industrial production in Japan, again just before the bubble burst and just after

Here is the recent US

“A slow sort of country!” said the Queen. “Now, here, you see, it takes all the running you can do, to keep in the same place. If you want to get somewhere else, you must run at least twice as fast as that!” -Lewis Carroll, Through the Looking Glass

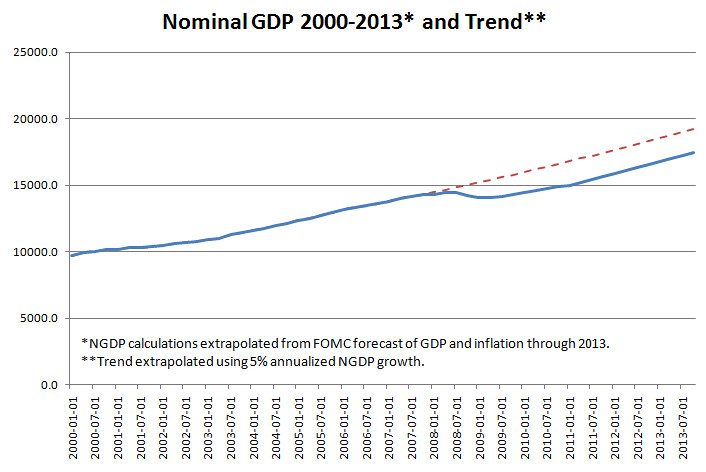

I have constructed a chart extrapolating the trend growth in nominal GDP* through 2013, along with the FOMC’s forecast of nominal growth through 2013.** Have a look:

[Click Image to Enlarge]

As you can see, by the Fed’s own forecast, we will remain under trend growth in NGDP through 2013. Indeed, by the fourth quarter, we will be 10.2% below the trend. That is roughly $1.7 trillion in potential output! I regard this as the “one chart to rule them all”, and it is what I point to when people ask me why we are experiencing a sluggish “jobless” recovery.

Always keep in mind, though, prediction is a fools errand over anything but the shortest of time spans. The key here is that there is only one way the prediction can be off such that it would benefit the economy. Those aren’t good odds to take.

*FRED

**Average of the central tendency.

Arnold writes

Once upon a time, everyone worked for the MyTeaEst corporation, which produced one million loaves of bread in the year 2000. It paid its workers in bread, and they ate the one million loaves.

MyTeaEst also gave half of its workers a pension plan, promising them one million loaves of bread in 2025. It gave the other workers a 401(K) plan, where the workers deposited bonds issued by MyTeaEst that promised one million loaves of bread in 2025.

The year 2025 came. MyTeaEst still produced one million loaves of bread, with a new generation of workers. Those workers expected to be paid, in the aggregate one million loaves of bread. The older generation of workers on the pension plan expected one million loaves. And the older generation of workers with the 401(K) plan expected that their bonds would be repaid.

What do you suppose happened?

In 2001 analysts note that MTE has not increased capacity over last year and has no plans to do so. Cannot be considered a growth stock. Given its lack of earnings the stock price collapses and MTE is shifted to the pink sheets.

With equity trading on the pennies the bond fund manager sees the writing on the wall and begins to buy up MTE stock. For fun we’ll also speculate that MTE has a unionized pension plan. The Union sees what the bond holders are doing and starts a proxy battle for MTE

The two have an equal financial stake in MTE. However, the union also has strike power, which lowers the bond holders willingness-to-pay.

Bondholders sell out or otherwise concede to the Union. MTE becomes Union owned. At this point the Union creates MTE-U and signs a pension contract making it MTE-U’s senior creditor. MTE-U then acquires MTE’s assets in exchange for MTE-U debt.

2025 comes. MTE-U defaults on its obligations to MTE. This leads MTE to default to its bond holders. The bondholders take possession of MTE and its MTE-U bonds. MTE-U then defaults. However, its pension holders are senior. They take the assets of the company and divide them amongst themselves.

The new crop of workers is fired and the original bond holders get nothing.

I, for the life of me, can not understand where Stephen Williamson is coming from in the recent posts he’s done claiming that Quantitative Easing is ineffective, and that the Fed is completely out of tools which it can use to boost the economy. Here are the points he made from his most recent post, entitled “Mark, Brad, and Ben“:

- Accommodative monetary policy causes inflation, but with a lag. I think Brad’s inflation forecast is on the low side, as maybe Ben does as well. The policy rate has been at essentially zero since fall 2008. Sooner or later (and maybe Ben is thinking sooner) we’re going to see the higher inflation in core measures.

- Maybe Ben is more worried about headline inflation (as I think he should be) than he lets on.

- Maybe in his press conference Ben did not want to spend his time explaining why the Fed spends its time focusing on core inflation. What every consumer sees is headline inflation, and they are much more aware of the food and energy component than the rest of it.

- As with my comments on Thoma, there is really no current action that the Fed can take to increase the inflation rate. More quantitative easing won’t do anything, so the Fed is stuck with saying things about extended periods with zero nominal interest rates in order to have some influence through anticipated future inflation on inflation today.

Most of the list simply baffles me. First of all, accommodative monetary policy can cause inflation. And of course in the long run, a stable monetary policy only affects prices…but the blanket statement that monetary policy causes inflation is misleading, and highlights a problem with even talking about inflation. In a standard AS/AD model, the determinant of the composition of NGDP growth is the slope of the SRAS curve. In recessions, it is generally understood that the SRAS curve is relatively flat. In that case (arguably the case we are dealing with right now), an accommodative monetary policy which shifts the AD curve to the right would result in much higher output growth than inflation. As for the lag part, monetary policy has an almost immediate (< one quarter) impact on many markets; including interest rates, stock/commodity prices, inflation expectations, etc. Here is a chart of those market reactions to both QE's courtesy of Marcus Nunes:

[Click Image to Enlarge]

In each case, you can see that asset prices had a quite immediate response to quantitative easing. QE2 performing poorly doesn’t indicate that QE doesn’t work, it highlights problems with how the policy was implemented. Specifically, the Fed structured the policy around purchasing a specific quantity of Treasuries ($600bn) instead of setting a target level of nominal spending, or even a price level target, and then commit to purchases until that target has been reached.

Second, why would Ben Bernanke be worried about headline inflation when nearly every forecast from the Federal Reserve views the current rise in headline as temporary? Here is the SF Fed, which I posted earlier:

[Click Image to Enlarge]

Indeed, the FOMC’s own report states as much. Furthermore, we have a good idea of what is causing the bump in headline inflation, and that is the energy prices. We also have good reason to believe that this is due to rising demand in the briskly growing emerging markets, and the inability to ramp up supply. What in the world is monetary policy supposed to do about that? Is Williamson advocating tightening policy while NGDP is still FAR below trend, and we are not experiencing enough growth to catch up to the previous trend?

I don’t have many quibbles with the third point, but the fourth point is the one that floored me the most. I’ll outsource commentary to David Beckworth in a comment on Williamson’s post:

Steve,

Why do you keep saying there is nothing the Fed can do? You acknowledged in the comment section in your last post that the Fed could do something more via a price level or ngdp level target. By more forcefully shaping nominal expectations with such a rule the Fed could do a lot.

It is worth remembering that folks were saying the same thing about monetary policy in the early 1930s. They were certain there was nothing more the Fed could do and as a consequence of this consensus we get tight monetary policy and the Great Depression. Then FDR came along and change expectations by devaluing the gold content of the dollar and by not sterilizing gold inflows. His “unconventional” monetary policy packed quite a punch.

And here is my comment:

I’m with David on NGDP targeting. But even if the Fed didn’t do that, it has its interest on reserves policy, and the last I checked, it hasn’t set an explicit inflation level target, and there is ~$14 trillion in outstanding Treasury debt held by the public that the Fed does not yet own…something Andy Harless has pointed out on numerous occasions.

Robin Hanson asks

The question is: are the lives of the workaholics around you are within an order of magnitude of being worth as much as typical human lives?

Why ask this? Because this is a key issue for judging if the coming em (whole brain emulation) revolution is glorious or horrifying.

….

And among all the humans available for scanning, the first generation of ems would select for humans who are both very productive, and willing to work very hard. So ems would be world-class-capable workaholics who stop working not much longer than needed to recuperate and rest.

For those not up on the lingo, Ems are robots made by copying human brains. There are reasons to think copying human brains may be a lot easier than programming smart robots from scratch.

The thorny issue is that then the minds of these Ems will have all of the properties of human minds, including the capacity for joy and suffering. If we think most of these ems will lead good lives then that’s a wonderful thing. If we think most of them will lead bad lives then it’s a horrible thing.

What economic analysis suggests is that most of them will live lives that are relatively heavy on work and short on play. Is that a good life?

Well as Robin suggests if we get ems that are workaholics it probably will be. In my mind this puts some premium on making sure we Em the right people and that we understand what makes them tick.

If I am reading Robin correctly he’s suggesting that either that it will be natural to pick people who like to work, or that through competitive pressure Ems made from those people will come to dominate the population of Ems.

This makes sense but there is an alternative concern. What about folks who are willing to work hard and be productive under stress but don’t really enjoy it. They would rather live lives of philosophical contemplation but if the choice is work or starve (or be deleted) they will work hard and work well.

Its not immediately clear that choice by the original scanners or competitive selection pressures will drive these people out of the population. It could also be the case that selection chooses people who are driven by discontentment to strive for economic status that it will be impossible for everyone to share.

Bill McBride, aka Calculated Risk, looks at vacancy rates and concludes

This suggests there are still close to 1.4 million excess housing units.

One of the difficult things in making economic forecasts is trying to figure out how far to drill down. Most forecasts revolve around the notion that there are fundamental behavioral regularities in markets, firms and individuals.

Right now Bill is looking at how many homes are empty. There are more empty homes than usual and this suggests that there are more homes than folks looking for a home. This in turn suggests that the impetus for building new homes will be mild and we should expect mild residential construction over the near term.

This is what I would think of as a medium drill down and it has certain forecast risks. The most obvious is that something odd may be affect the number of people looking for a new home. If that changes suddenly and more people start looking for a home, then you could have a shocking fall in vacancy rates, which then produces a rise in the demand for new construction.

I have been using a slightly deeper drill down that looks at population and the flow of housing. Under that comparison people per home is starting to rise above its historical average, and at the current pace of construction is set to make records over the medium term. Thus I see a strong demand for new construction building.

This drill down has risks as well, and they are basically the inverse. What if there is a “new normal” in household size. In that case I will be waiting for a boom that never comes. What changes instead is the way people live.

In either case the forecast risk is that you have picked the wrong regularity to hang your hat on. This runs across virtually all forecasting domains that I can think off. In every case you have to assume that certain things are attractors to which the economy will always be brought back and certain things bounce around from shocks.

There are worse things than inflation, and we have them

~Jim Tobin

From USA Today

With three college degrees including an MBA and a resume boasting volunteer work and a 25-year stint at one company, Linda Keller is devastated by what employers see in her.

"She’s lazy. She’s not doing anything. Her skills are out of date. She’s out of touch with reality," Keller rattles off. "That’s what hiring people think."

That’s because Keller, 53, has one strike against her that’s hard to overcome in today’s ultracompetitive job market. She’s unemployed — and has been for 19 months.

She’s among 4.4 million people nationwide who have been out of work for a year or more. The group makes up more than 40% of the total unemployed, the highest percentage since World War II.

Even among folks that I respect there seems to be this weird fear that the US government is going to attempt to inflate away its debts. There are a couple of problems with this from my perspective.

First, its actually not that easy from a technical point of view. A significant portion of the US debt is in very short term securities, like 90 days. If I remember correctly the bulk of foreign holdings is in securities with a maturity of less than a year. This is because they are using Treasuries as a liquidity vehicle and under those circumstances you want the shortest maturity possible.

So what happens with this massive inflation? It simply drives up the interest rate of Treasuries. You get to screw investors for 90 days and then much of the jig is up.

Second, large domestic holders of Treasuries are folks the US government has implicitly agreed to backstop: pension plans, major US banks, insurance companies, state and local governments. What is the point of screwing these folks out of their money if you are just going to turn around and give the money right back to them?

Third, why is this better than a structured default? Its not as if people are going to be oblivious to the fact that they were screwed. Having done it raises the risk premium on US debt. Not the default risk premium but the inflation risk premium. What do you really accomplish with inflation versus structured default?

Fourth, what do you accomplish period? Structured default scares everyone because of the prospect that it will bring a crushing recession. An effective attempt to screw holders of US Treasury bonds should accomplish the same thing. Whose interest is that in? The Fed? Politicians? Bureaucrats?

I just don’t see the internal constituency for saying, yeah lets inflate away the debt.

Right now, there is a serious debate over whether or not the Fed should aggressively return to 2% inflation in a effort to bring down unemployment. The radicals are suggesting that the Fed should make up for the extremely low inflation that we have experienced. Way out on the bleeding edge are folks like myself who are arguing that we should carefully and deliberately establish a higher long run target of 4%. The Fed would move to this target slowly, over time giving the markets a full opportunity to adjust and price in movements.

Yet, in spite of this the Fed is dragging its heels.

So, at this point there is a reasonable argument that the majority of stakeholders could benefit from an increase in the US inflation rate to 2%. What’s stopping the Fed is its concern over whether or not such a move would spook the credit markets.

Yet, at the same time some folks are worried that the US government would engineer a default through inflation, a situation which would benefit almost no one and works only by completely catching the markets by surprise.

These just doesn’t seem like a justified fear to me.

As before Russ Robert’s production is a thing a beauty and if it gets more people interested in economics then I am all for it.

As must probably be the case here a lot of the tension in the video seems to resolve around issues for which there has largely been synthesis.

I think of myself as a New Keynesian yet I agree with the Hayek character at least as much as the Keynes one.

Can’t we have an organic emergent economy in which an excess demand for money leads to insufficient demand for real goods and services?

Arnold Kling throws out

If you believe the Recalculation Story, then a lot of future profits are in businesses that do not exist today. There firms that turn out to be valuable years from now may not be the ones with shares outstanding at the moment.

- I have been meaning to mention that I hope Arnold keeps recalculation alive. This debate should keep going

- I don’t know how far you have to go into recalculation per se, to believe this though. Maybe it’s a cohort thing but the idea that most of future profits are in firms that don’t exist seems perfectly natural to me.

- There is also the issue that an increasing number of new profits will be held in private equity. I don’t know that this is bad from an efficiency point of view, but it makes the 401(k) pyramid scheme worse. If all retirees hold are stocks in dead companies there will be hell to pay . . . oh yeah and taxes. Broke old people just doesn’t play well.

Yglesias notes the status quo bias on display in New Jersey

Nancy and Eric Olsen could not pinpoint exactly when it happened or how.All they knew was one moment they had a pastoral view of a soccer field and the woods from their 1920s colonial-style house; the next all they could see were three solar panels

Now to borrow The New York Times’ photo:

This is not a pastoral view disrupted by solar panels. It’s a view of utility polls, street lights, and overhead electrical wires—now with solar panels! It would be interesting to see if people actually preferred a pastoral view free of the accoutrements of electrification but I doubt anyone actually prefers that. Instead, the customary interjections of technology into the suburban landscape are normalized while any deviation from the postwar pattern is anathematized. Had people 100 years ago had this attitude, I suppose nobody would have telephone service or electricity at all.

So we can point out how people are irrationally attached to what they have. And the blogosphere generally has had a lot of fun pointing this out and noting that the world would be a right and just place is everyone came around on this.

However, it is time for new fun. In particular, I want to point out that rather than bias we could be seeing a diversity of preferences, suddenly exposed to the material means to sort on the basis of those preferences.

So before you had to live with the people you were born with or the people who you worked with and they might not have been much like you preference-wise. Yet with expansion in transportation technologies people could more effectively sort into new neighborhoods with people who came from difference places and work in different places.

Through the magic of peer effects this is going to intensify your preexisting preferences until it becomes a burning desire not to change anything. You’re here because you like it here, and so is everyone else, and you have no interest in upending this pleasant equilibrium.

Call it sorting to stagnation. Once you find a group of likeminded people who all choose the same mode of living they will naturally resist changes in their mode of living. Of course, changes in the mode of living are what economists like to call economic growth.

Bernanke

- Like most I was disappointed at the tone of Bernanke’s speech and in particular a few points were he strayed into obfuscation, seemingly in an effort to quite inflation hawks.

- Conversely there times when you are trying to explain economics to an audience and you know they aren’t going to understand your “real” answer, so you make up something that will make sense to them but also get them to the right answer. Bernanke also went this route a few times response to inflation but not so much in response to unemployment. These responses seem to reveal a deeper concern about how his remarks will be interpreted by inflation hawks.

- I couldn’t really get a sense for what he thinks inflation expectations mean. There seems to be a split among economists, between those who believe that “expectations” means what’s priced into financial assets and, others who take expectations more literally and think of it as something like “what the average person believes” I tend to side with the financial market view. Bernanke’s posture seemed to give credence to the second view.

GDP

- The headline on this report is sobering but the internals don’t look as bad.

- Government knocked over 1 point off GDP. About .69 of that was defense spending. State and local continued to drag at .41 percent. This represents important drag but when thinking about the conditions facing private business, GDP looks better.

- Equipment and software continues to be strong, adding .8 points to GDP. We have experienced a strong rebound in equipment and software, that would be indicative of a mini-boom if there wasn’t the drag from construction.

- Residential and non-residential structures continued their drag on GDP, knock .7 or so off of growth.

Growth

- The path doesn’t look that bad.

- The fundamentals still seem like they are shifting towards stronger growth. We are not seeing depressed personal consumption expenditures. We are not seeing industrial production stall out. We are not seeing no new investment in equipment and software.

Here is a word cloud of words used by Bernanke during the press conference which was held today:

[Click Image to Enlarge]

As you notice, inflation was mentioned quite a bit, which, really, is something that you should expect from a QA with a monetary policymaker. Many are lamenting the fact that unemployment took a back seat, and Reuter’s itself challenges us to find the word “jobs” in the word cloud. Personally, I enjoyed the fact that Bernanke basically said jobs are someone else’s policy purview — which I view as the right response. However, the fact remains that monetary policy is not on target, and that is a problem for Bernanke. A bigger problem may be that 2% inflation isn’t a target at all! Could the US be following Japan’s lead into self-induced paralysis?

In any case, here is the question (and rest of the e-mail, references removed) that I sent to be asked, which did not get asked:

First, thank you for sending me your e-mail address. I’m tepidly excited about Bernanke’s press conference tomorrow…but I have a lot of reservations. You could probably call me old-fashioned, but I’m always leery of public policy “rock stars”, like the “Committee to Save the World”, and Ben Bernanke being “Man of the Year”. In any case, I think there is going to be a strong focus on grilling Bernanke on employment levels (I see that David Leonhardt wrote a column urging that to be so). I view this as very counter-productive.

But I did tweet you my question, which was this:

“As recently as 2003, Bernanke [You] championed price level targeting as a remedy for the ‘liquidty trap’. Many other economists also endorse this idea. Given the failure of monetary policy in preventing a sharp fall in GDP in Oct 2008 w/ inflation targeting, what are your thoughts on NGDP lvl targeting? Implementation challenges? Benefits or costs that you see?”

I wanted to provide some background for this question, because it can seem like it is kind of out of left-field, given a “mainstream” interpretation of events. As you may know, many prominent economists (Krugman, DeLong, Blanchard) have publicly advocated an explicit inflation of greater than 2%. A subset of this work was done by Lars Svensson[1] and Ben Bernanke himself[2], only instead of using inflation targeting, both economists have advocated setting an explict price level target in order to escape the “liquidity trap”. Another strain of this work that has been popularized recently by Scott Sumner, David Beckworth, Marcus Nunes, Josh Hendricksen, and myself, (among others!) involves monetary policy targeting nominal cash expenditures in the economy, or NGDP. More “academically”, Robert Hetzel[3] and Michael Belognia[4] have advocated that cash grow at a steady pace.

A common theme among those who push the “NGDP level targeting” view and others is that we tend to believe that causality in this recession runs (roughly) this course: mild supply shock (subprime) > tight money (Jun – Nov 2008) > large crash (Oct 2008) > inadequate Fed accommodation (2009/2010) > sluggish and “jobless” recovery. Indeed, even Christina Romer seems to be on board with something like this interpretation[5]. In my opinion, the Fed should target like a laser on the long-run growth path of NGDP, and keep it growing on a stable path (5% was the trend of the Great Moderation, but some economists advocate a transition to 3% nominal growth), making up for slack and overshooting when it happens by loosening or tightening money (respectively) such that the market forecast and the Fed’s forecast are basically one-in-the-same. This leaves little room for paying much attention to the level or rate of employment in the economy. The only time that should concern the Fed is if there is a large enough structural change that they should revise their NGDP target based on a sustainable increase (or decrease) in productivity (be it labor, capital, or TFP).

As an aside, David Beckworth has urged the Fed to target the cause of macroeconomic instability, and not symptoms of it[6]. Unemployment is one symptom, as is inflation/disinflation/deflation. From this perspective, NGDP level targeting is far superior to price level (and inflation) targeting.

I hope that gave you a brief (but adequate) overview to acquaint yourself with the NGDP level targeting position if you were unfamiliar, so you’re not shooting in the dark. I know you probably won’t get to the references. As a tactical request, if you see it fit to use my question, I’d work hard to get an answer out of Bernanke regarding NGDP targeting rather than price level targeting. The reason I bring this up is that if you mention “price level targeting” in the question, while you make the question more likely to get answered (price level targeting is more mainstream), you also give Bernanke an out in that he can simply muse about price level targeting and avoid the NGDP targeting question altogether, even though they’re different concepts. It’s a tricky pole to balance.

Thanks for allowing me to participate!

Niklas Blanchard

http://www.modeledbehavior.com[1] http://papers.ssrn.com/

[2] http://www.federalreserve.gov/ and http://people.su.se/

[3] http://www.richmondfed.org

[4] http://mpra.ub.uni-muenchen.de/

[5] http://emlab.berkeley.edu/

[6] http://macromarketmusings.blogspot.com/ and http://macromarketmusings.blogspot.com/

Sadly, there were no intrepid reporters in the audience venturing these grounds.

[h/t Paul Krugman]

Kevin Drum recently set off a round of debate in the blogosphere lately with a post about the price elasticity of oil and carbon taxes. He cited an IMF study that showed a long-run price elasticity of oil demand of -0.035. What this means is if oil prices go up 10%, then the long-run demand for oil goes down 0.35%. The implication he draws is that any reasonably priced carbon tax isn’t going to have much of an impact on demand, and so it’s not going to be an effective policy for reducing carbon emissions. There’s obviously some problems with this, some of which has already been covered by Ryan Avent, Megan McArdle, and Kevin Drum himself, with Jim Manzi and Kevin Drum, again, on the other side. Importantly, as Alex Tabarrok pointed out, this is but one estimate of the price elasticity of demand for oil, and it’s smaller than what you find in the literature. The following table from a James Hamilton paper, also linked to by Alex, reports the results of several literature reviews of oil and gasoline price elasticities:

As you can see, all of these elasticities are significantly above the IMF estimate. However, there have been several recent studies, including the Hamilton study, that argue that the price elasticity of demand has decreased in the past decade. Hamilton, in fact, argues that markets were surprised by how low the global price elasticity of demand was, and the unresponsiveness of demand explains the high gas prices of 2007-2008.

Another recent studyby Hughes, Knittel, and Sperling, found short-run gas price elasticities of -0.034 to -0.077 for 2001-2006 compared to the much larger elasticities for 1975-1980, which range from -0.21 to -0.34. While these numbers are larger than the IMF numbers, they are never the less low and indicate that the average elasticities found in past studies may be too big.

However there are important caveats to these estimates that suggest the real current elasticity is higher. First, the evidence has indicated that the response of demand to price changes is asymmetric: price increases cause a larger response to demand than price decreases. This is because price increases are more likely to cause shifts to newer, more energy efficient technologies than price decreases are to undo such shifts. Any estimate of the average price elasicity then will be a downward biased estimate for the likely response to a price increase.

A recent paper by Davis and Killian The Journal of Applied Economics covers some other econometric issues in the literature. For instance, we know price and quantity demanded are jointly determined, which means that there will be a correlation between the price variable and the errors such that single equation or panel data methods, like those used in the reported IMF estimates, will bias estimates towards zero. Some studies attempt to use exogeneous oil shocks as instrumental variables. This approach is used in the appendix to the IMF study. But this requires the assumption that consumers will respond the same to these shocks as to normal real price appreciation. If consumers expect shocks to be more temporary than a demand led increase in price, this is a questionable assumption.

As Killian and Davis point out, another serious problem with these estimates is that they estimate the price elasticity of demand, and not the tax elasticity of demand. They argue:

“…the response of gasoline consumption to a change in tax is likely to differ from its response to an average change in price. Price changes induced by tax changes are more persistent than other price changes and thus may induce larger behavioral changes. In addition, gasoline tax increases are often accompanied by media coverage that may have an effect of its own.”

To overcome these issues, they look at U.S. state level demand for gasoline. Their results shed some interesting light on how the econometric mispecifications affect elasticity estimates. Using a single equation model they estimate an elasticity of -0.10. Using a panel data method, as done in the IMF study, the elasticity increases to -0.19. And finally using changes in state level gas taxes as an instrument they find an elasticity of -0.46, which more than four times larger than the single equation model.

They conclude with an important caveat about the literature:

Overall, our results indicate that gasoline consumption is more sensitive to gasoline taxes than would be implied by recent estimates of the gasoline price elasticity. Even under the largest plausible estimates, however, gasoline tax increases of the magnitude that have been discussed would have only a moderate short-run impact on total US gasoline consumption and carbon emissions based on our estimates. A natural conjecture is that the long-run elasticities will be larger, but standard econometric models based on historical data do not allow the prediction of such long-run effects.

The International Handbook on the Economics of Energy also puts these estimates in the correct context:

Whatever their scope and origin, estimates of price elasticities should be treated with caution. Aside from the difficulties of estimation, behavioural responses are contingent upon technical, institutional, policy and demographic factors that vary widely between different groups and over time. Demand reponses are known to vary with the level of prices, the origin of the price changes (for example, exogenous versus policy induced), expectations of future prices, government fiscal policy (for example, recycling of carbon tax revenues), saturation effects, and other factors (Sorrel and Dimitropoulos, 2007). The past is not necessarily a good guide to the future in this area, and it is possible that the very long-run response to price changes may exceed those found in empirical studies that from relatively short time periods.

The evidence certainly seems to suggest that more recent estimates are better than earlier ones, but for a variety of reasons these will underestimate the long-run elasticities.

From WaPo

The supply has not kept up with demand in part because of a shortage of apartments, a key source of new rentals. Developers cut back on such projects when the economy deteriorated in 2009, which drove down vacancies and boosted rents. Analysts say they expect rents to keep climbing as developers try to ramp up new projects and catch up with demand.

The scarcity of affordable rental units was most pronounced in the West, where only 53 units were available for every 100 very-low-income households that are looking to rent, according to the study, which analyzed federal survey data from 2009. That compared with 65 in the South, 66 in the Northeast and 87 in the Midwest.

Semi-retired blogger Scott Sumner commented on Karl’s post about how the CPI calcuates inflation of owner-occupied housing. So long as he keeps commenting around the econ blogosphere, we can effectively keep him from retirement by hoisting these comments. Here is Scott on Angus, to whom Karl was responding:

I read his argument differently. Reading between the lines, here’s what I think he meant:

1. The Fed doesn’t care about the “cost of living” per se, they care about the price level because supposedly a stable price level produces macroeconomic stability.

2. The price of new homes is an important part of the overall price of goods and services produced in the US.

3. If the Fed stabilizes a price index, that index should include the price of new homes.

4. It’s fine if we have a cost of living index that excludes the price of new homes, just don’t have the Fed target that index.

I don’t see your argument as being inconsistent with what he wrote.

I think Scott’s point here is that there’s a distinction between what should go in a cost-of-living index and what the Fed should target. I’m pretty skeptical of this idea, so I’ll run through some reasons why.

One conceptual problem is that house prices reflect value of the flow of housing services consumed and the investment value of the home. As Karl points out, why should housing investments be counted in a cost-of-living index while other investments are excluded?

A 2005 survey of OECD countries found that 13 out of 31 statistical agencies used the owners-equivalent method for their CPI, and the next most popular method, used by 9, was to just leave owner-occupied housing out. Only two countries, Australia and New Zealand, utilize the acquisition approach, which measures house prices changes the same way you would with non-durable goods. Below is a graph from The Economist of the ratio of house prices to rents from Q1 2000 to Q4 2010 for Australia, the U.S., and New Zealand (the United States is the lowest one at the end, it’s a little hard to tell with the colors).

While the other two countries have thus far avoided a massive crash, they didn’t avoid massive appreciation. You could argue that this just means the changes in prices in these two countries was real and driven by fundamentals. But given these massive differences in the real paths of price-to-rent ratios, what level should the Fed target? How do they distinguish price appreciation drive by real changes in cap rates from pure nominal or speculative inflation? I’m not sure how Australia and New Zealand handle this.

Another problem with the acquisitions approach is that the sale of a home is frequently an exchange between households, and so a sold house is both a cost and a revenue for the household sector. According to the BLS, when statistical agencies use the acquisitions approach they control for this by only looking at home sales to the household sector from other sectors. In practice, this usually amounts to new housing units. This may reflect the cost of new goods and services produced in the U.S., but clearly doesn’t represent a measure of the cost of goods and services being consumed by households. How would the Fed weigh the tradeoff between a price measure that was a true COLI and one that included houses? Say demographics or something else permanentely shifts average cap rates down and thus real house prices up while the cost of living is unchanged. If the Fed tries to tamp the house price inclusive price index down won’t inflation and thus nominal GDP be too low? Of all people I’d expect Scott to worry about this.

Let me end by saying that I am pretty skeptical about the inclusion of house prices as a component of a cost-of-living index. I’m also skeptical about the idea that the Fed should target a non-COLI price level that includes house prices, but less so than in the former, and I’m not strictly closed to the idea.

Michael Petrelli has ten proposals that he thinks should be part of federal education reform that are worth reading:

Expect states, as a condition of Title I funding, to adopt rigorous (i.e., “college- and career-ready”) academic standards in reading and math (either the Common Core standards or equally rigorous ones).

Likewise, expect states to adopt rigorous “cut scores” on tests aligned with those standards—making sure these cut scores signify true readiness for college and career.

Require states to develop the capacity to measure student growth over time.

Demand regular testing in science and history, not just reading and math, in order to reverse curricular narrowing and foster a more complete education in key subjects.

Eliminate Adequate Yearly Progress (AYP) and instead require states, as a condition of Title I funding, to adopt school-rating systems that provide transparent information to educators, parents, taxpayers, and voters. Such state reporting systems would have to be pegged to college and career readiness and, for high schools, to graduation rates. They would have to rate all schools annually on their effectiveness and include disaggregated data about subgroup performance.

Eliminate all federally mandated interventions in low-performing schools. Allow states to decide when and how to address failing schools—and other schools.

Eliminate the Highly Qualified Teachers mandate.

Rather than demand “comparability” of services across Title I and non-Title I schools, require districts to report detailed school-level spending information (so as to make spending inequities across and within districts more transparent).

Offer states the opportunity to sign flexibility agreements that would give them greater leeway over the use of their federal funds and would enable them to target resources more tightly on the neediest schools.

Turn reform-oriented formula grant programs into competitive ones. Specifically, transform Title II into a series of competitive grant programs, including Race to the Top, i3, charter-school expansion and improvement, a competitive version of School Improvement Grants, and an expanded Teacher Incentive Fund.

For innovation to affect the lives of ordinary citizens the innovation must be in things ordinary people by. This causes a problem when those with a natural propensity to tinker to impress live in a different social class that the mass of their fellow citizens

The company has launched a new site called eBookToss.com, a virtual “e-book swap” that will facilitate the direct lending of e-books between consumers using the lending features enabled by platforms like the Kindle, and the Nook.

BookSwim CEO George Burke said:

“We’ve been talking to publishers about the concept of e-book rentals, but we don’t really know how possible that is. But, based on the announcement from Amazon in December [about enabling loans], we think we’ve found a model.”

eBookToss.com pools users to create an online list of lendable e-books and will facilitate free loans directly between users (contingent on features enabled by e-book providers, of course). The company is not the first to come up with the concept, though. A Web site called ebooklendinglibrary.com has been quietly operating a forum and a bulletin board for people to lend e-books, but it’s not very sophisticated and has generated only light traffic thus far. Probably because they’ve been trying to retrofit a message board into a swapping community, which is prone to problems.

Angus at Kids Prefer Cheese is shocked at the disconnect between housing prices and CPI

Chairman Ben’s point of view is that the Fed should do so only to the extent that the bubble bleeds into overall inflation.

Here’s a graph, courtesy of Dr. Housing Bubble (clic the pic for a more glorious image):

The red line shows the growth rate in the Case-Shiller housing price index, the blue line shows the growth rate of housing component of the CPI.

YIKES!!!

From 1998 to 2006, there was a complete disconnect between housing prices (rising like crazy) and the BLS measure of owner equivalent rent (which never went up more that 4% in any of those years).

Hard for a bubble to bleed into inflation when it’s been defined out of the index!

Stock and bond prices aren’t in the CPI. In theory, however, exploding stock and bond prices could lead to increased spending and to inflationary pressures.

We can argue that one should target asset bubbles, but not having housing prices in the CPI is appropriate. If all people cared about was finding a cheap place to live then they could rent. People buying homes in the bubble were making bets on housing prices, interest rates and/or future rents.

Alan Greenspan via the Journal

In an appearance Sunday on NBC’s “Meet the Press,” Mr. Greenspan used his strongest words yet to urge lawmakers to let them expire. The risk of a U.S. debt crisis, he said, is just too big. Mr. Greenspan, who retired from the Federal Reserve in 2006, had endorsed the cuts back in 2001 championed by then-President George W. Bush.

“This crisis is so imminent and so difficult that I think we have to allow the so-called Bush tax cuts all to expire. That is a very big number,” he said, referring to how much the U.S. government could save from letting income taxes go back up to levels last seen under former President Bill Clinton

I concur with Mark Thoma that a debt crisis is not imminent for the United States. I doubt even that such a crisis will occur in a decade, even with no policy change.

However, it does seem likely to me that the Bush tax cuts will be allowed to expire in the near future.

I am sure there has been some more serious work on this but I am toying with the idea that Government generally and public policy in particular is for the most part a reflection of social ethos. Where government’s in policy and in structure differ is in their “response function.” Are they swift or slow to respond to respond to changing ethos? Do they respond in violent fits and starts or in calm reform, etc.

In its most radical of forms this would say that the average treatment effect of absolute dictatorship or direct democracy on the lives of the typical citizen is zero. Dictatorships have a different response function than democracies and this leads to wider variance, but not to different average outcomes over the long run.

In addition, the consistent differences between life under the two forms of government represent selection effects rather than treatment effects. Societies with rapidly changing ethos will tend to “snap” more rigid forms of government.

Rapid growth in technology, particularly transportation and communication technology will tend to create more ethotic churn. Rigid governments in these places will snap. Since, democracies tend to be less rigid there will be – at least in the short term – an evolution towards democracy.

Thus when we observe the world we see that rich, pluralistic countries are democratic. We may mistakenly believe that democracy then leads to wealth and pluralism. However, it is that democracy is more “evolutionarily fit” to withstand the ethotic churn associated with wealth and pluralism.

I don’t know where this fits in the canon of political theory and if its all been said before, and better.

To the extent there is something here though, there are some implications.

For example, focusing on the regimes and policy in a government in order to change the lives of the people over which the government rules is extremely limited in its effectiveness. At most you can change the response function. This might have some important short term implications but because (a) governments over the long run are a veil and (b) governments must be “evolutionarily fit” to survive, these strategies cannot make a huge difference.

Real differences come from changing the ethos. In a practical sense this means religious or quasi-religious movements. The fact that religion does the heavy lifting in a society and that church and state have rarely been separated in history, also explains some of the over focus on government itself.

In this reading Communism, to the extent it had as large of an effect as it did, did so not because it was a new form of government but because it had the structure of a religious movement. People came to Communism as they would come Christianity or Islam.

This is why Marxism emerged as the strain of communist/socialist thought that was able to have such sweeping effects. Marxism was much more amenable to becoming a quasi-religion.

Though wise men at their end know dark is right,

Because their words had forked no lightning they

Do not go gentle into that good night.~Dylan Thomas

Arthur Brooks rages against the dying of a light

We are not a perfect opportunity society in the United States. But if we want to approach that ideal, we must define fairness as meritocracy, embrace a system that rewards merit, and work tirelessly for true equal opportunity. The system that makes this possible, of course, is free enterprise. When I work harder or longer hours in the free-enterprise system, I am generally paid more than if I work less in the same job. Investments in my education translate into market rewards. Clever ideas usually garner more rewards than bad ones, as judged not by a politburo, but by citizens in the marketplace.

There is certainly a role for government in this system. Private markets can fail due to monopolies (which eliminate competition), externalities (such as pollution), the need for public goods (such as education, which is indispensable in an opportunity society), corruption and crime. Furthermore, most economists agree that some social safety net is appropriate in a civilized society. When the government focuses on these things, it assists the free-enterprise system.

But when a government that has overspent for years turns to tax increases instead of spending cuts simply for the sake of “fairness,” it weakens free enterprise, lowers opportunity and impoverishes us in many ways.

It takes only one graph to show this

As you can see the United States spends more resources per capita on health care than any country in the world. If you were worried about possible government distortion compare the light blue and dark blue bars.

The light blue are private expenditures on Health Care, the dark blue are public expenditures. As you can see private US spending easily outstrips every other country in the world.

That in-and-of itself establishes the US as the most efficient system. One does not need to look at outcomes to determine Why?

Well, we know that patients like to spend money on health care. We can see that as they are provided more insurance, they spend more money. We can see that as they become wealthier, they spend more money. We can see that as they are exposed to the market mechanisms – compare private insurance to Medicare – they spend more money. Spending more money on health care seems to be inline with satisfying consumer preferences.

Yet, couldn’t this all be a waste. Don’t outcomes matter for efficiency? No, they don’t.

They don’t because patients themselves do not look at outcomes and satisfying consumer preferences is the gold standard of efficiency.

From Death and Reputation: how consumers acted upon HCFA mortality information

From 1986 through 1992, the Health Care Financing Administration (HCFA) released information comparing patient death rates at individual hospitals. This was viewed widely as an effort to aid consumers in selecting hospitals. This study evaluates how the release of this information affected hospital utilization, as measured by discharges. It finds a very small, but statistically significant effect of the HCFA data release. A hospital with an actual death rate twice that expected by HCFA had fewer than one less discharge per week in the first year. However, press reports of single, unexpected deaths were associated with an average 9% reduction in hospital discharges within one year. HCFA was justified in eliminating its mortality report, not because it was being used by consumers to choose hospitals, but because it was not. Implications for report cards are discussed.

Patients in this study did not really care if the hospital killed them.

From Is More Information Better? The Effects of ‘Report Cards’ on Health Care Providers

Using national data on Medicare patients at risk for cardiac surgery, we find that cardiac surgery report cards in New York and Pennsylvania led both to selection behavior by providers and to improved matching of patients with hospitals. On net, this led to higher levels of resource use and to worse health outcomes, particularly for sicker patients. We conclude that, at least in the short run, these report cards decreased patient and social welfare.

Patients in this study, used increased information to choose more resource intensive hospitals, which were in fact more likely to kill them

From CONSUMER REPORTS IN HEALTH CARE: Do They Make a Difference?.

Studies were selected by conducting database searches in Medline and Healthstar to identify papers published since 1995 in peer-review journals pertaining to consumer report cards on health care. The evidence indicates that consumer report cards do not make a difference in decision making, improvement of quality, or competition.

The authors engage in some PC handwaving at the end but the core conclusion of their data is that consumers don’t use information on effectiveness.

The best that can be said for patients and health information is the following From Systematic Review: The Evidence That Publishing Patient Care Performance Data Improves Quality of Care

Forty-five articles published since 1986 (27 of which were published since 1999) evaluated the impact of public reporting on quality. Many focus on a select few reporting systems. Synthesis of data from 8 health plan–level studies suggests modest association between public reporting and plan selection. Synthesis of 11 studies, all hospital-level, suggests stimulation of quality improvement activity. Review of 9 hospital-level and 7 individual provider–level studies shows inconsistent association between public reporting and selection of hospitals and individual providers. Synthesis of 11 studies, primarily hospital-level, indicates inconsistent association between public reporting and improved effectiveness. Evidence on the impact of public reporting on patient safety and patient-centeredness is scant.

We can go on and on with this and rest assured, I will.

However, ask yourself this question. When is the last time you heard someone say: I chose Surgeon Johnston because he has lowest mortality rate in the country.

The issue is this: the word efficiency has positive affect. It makes you think of something good. Yet, the US health care system looks like its doing something bad. Thus people reject the notion that it is efficient.

But efficient does not mean doing something good. Efficiency is a measure of good a system is at satisfying consumer preferences. Consumers seem to value spending money on health care. They very much want to do it and are upset when they cannot do it.

Yet, consumers do not seem to value better health care outcomes. When given the alternative between a system with good outcomes and one with bad outcomes they behave as if they do not care which one they get.

Thus a system that spends lots of money with little regard to outcome is highly efficient: it gives people more of what they want.

I was happy to see Robin present a post on long run health care costs. Though unfortunately he seems to get caught in the same rut as the rest of the intelligentsia.

He asks us to imagine a fountain of youth pill that kept everyone thirty forever. Unfortunately, as your true age got older you would need evermore pills. He says

a fountain of youth pill whose required dosage doubled every decade would either have to be banned, or given to everyone over thirty with insurance. And if everyone were required to have insurance, that would be everyone over thirty. But then the per-person expenses of this system would almost double every decade, growing about 7% per year. Every decade that passed, the oldest folks would be ten years older, and require twice the dosage. But per-capita economic growth rates today are far below 7%. So eventually we’d run out of money to pay for these pills; we’d have to say no to some people, and then they’d quickly die. And the longer we waited before admitting to ourselves that we couldn’t afford to give effective treatments to everyone, no matter what the cost, the worse it would be.

Why would it be worse the longer we lived in self-deception? That really needs to be spelled out because off the top it sounds like Robin is describing a scenario in which we maximize the the total amount of human life we can support. We are also doing this without implicitly valuing anyone’s life over anyone else’s. We save everyone we can, as long as we can, until we hit capacity. This could easily be a utopian scenario.

Again, its probably not the scenario I prefer but one has to be explicit about exactly why throwing everything we have at an extremely effective method of preserving enormous amounts of human life is bad idea. It seems like something the average person would regard as a great idea.

Good thing we don’t have a fountain of youth pill, right? Actually, our real situation is worse. Per capita medical spending in the US doubles about every fifteen years, which is still much higher than our economic growth rate.Yet we struggle to see any substantial correlation between health and medical spending – our medicine is mostly useless on the margin. Its nothing like a fountain of youth pill.

Its not clear why it’s a good thing we don’t have the pill, seeing as how the nightmare scenario seemed pretty good.

However, the analogy with current US spending seems to have a few problems to me.

Implicit in Robin’s story is that the pill had some irreducible non-zero real cost and that we were paying that in order to obtain clear benefits. Once you have you that, it’s a necessary condition that the cost of producing the pill will eventually outstrip our capacity to produce it.

Is this the case in Medicine? Robin, of course, recognizes that there is no clear benefit. And as, such there is no clear resource that one must obtain to keep this process going, aside from human time.

Lets try to stay with the pill story but instead of it being a glorious fountain of youth it goes like this: There are pills which people believe to help ward off death. In fact these pills are just a placebo. Yet, they do have an effect because the placebo effect is an effect.

Because the pills are only a placebo they are simply made out of whatever matter is available plus some human time devoted to stamping the label pill-XXXX on them.

Training is required to become a pill stamper. It is easy for smart people to get this training and harder for less smart people.

This dynamic causes the cost of bringing new pills to market to steadily rise. We need more pill stampers. All of the easy pill stampers have been taken and so now we are forcing more and more people through the pill stamping training so that they can stamp pills.

As the number of pills rises we begin devoting larger and larger fractions of our economy to pill stamping. By necessity this means the pill stamping industry must be growing faster than the overall economy. Else it would be shrinking as a fraction, not growing as a fraction.

Wasting all of this time and effort just to get someone to stamp placebo pills seems like a waste of time and I would argue that it is. But, is it sustainable. As far as I can tell its utterly sustainable.

Under a completely totalitarian system we would eventually lock everyone into the pill stamping industrial complex. From birth they would their lives would be channeled towards the eventual goal of either becoming a pill stamper or producing the bare necessities to support the pill stamping industry.

In a slightly more free economy, resources either through taxation or insurance mandate would be constantly flowing towards the pill stamping industry. This would lead to many many folks seeking jobs as pill stampers and parents likewise funneling their children through pill stamping pre-schools.

All resources would not eventually flow to the pill stamping per se because as it grew to enormity, the price of goods and services needed to support the industry would rise. The pill stampers would still need to eat. The would still need shelter from the elements. They would still need some way to dispose of human waste products.

These functions could come about as separate entities or they could be subsumed into the pill production supply chain. For example, every pill facility could have its own dorms, cafeterias, plumbing system, perhaps even in house facilities to produce cheap uniforms for the stampers.

In any case economic growth would come to be dominated by pill stamping and the economy and pill stamping would be two different names for the same thing. Society and life would revolve around the process of stamping pills.

In imagining this scenario, I my hope is that it is clear it is undesirable. It is a place were all of human hopes and dreams have been pushed aside in favor of “useless” pill stamping.

However, it should hopefully also be clear that it is completely sustainable. Humanity could go on like this forever. There is nothing that I see that would stop this, accept of course for extinction level events that would occur anyways.

The problem with this scenario is not that its impossible or that one day it will hit cliff that we will all fall off of. The problem in its most raw sense is that it takes things that I –Karl Smith – value and trades them away for things that I –Karl Smith – do not value. Thus it is a world that is to me undesirable.

However, there is no law that society or the propagation of the species will breakdown if everyone devotes themselves to something that I think is useless.

I didn’t do anything cool, or come up with any neat, contrarian, controversial, or interesting points to tell you about Earth Day (luckily there is always Mark Perry). So an old postcard that I designed will have to do.

[Click Image to Enlarge]

The picture of earth was a bump and shadow map, and the text was custom (and quite time consuming to make), the postcard was a stock image, but the postage stamp and ink stamp were added =].

If you have any such points about earth day, share them in the comments!

A couple of points thoughts today

- I’ve said that the ability of the US to borrow cheaply has primarily financed tax cuts for wealthy Americans. I want to be clear. I do not mean that wealthy Americans should have been taxes so as not to increase the deficit. I mean that if I do my best to imagine a world in which cheap borrowing was impossible that the result I get is not a much smaller welfare state but higher taxes on high income Americans.

-

I want to reiterate that its not clear to me that this has made America poorer. Indeed, using your high credit rating to borrow cheaply and lend dearly is a time honored way of getting rich. It seems to me that America has used this method and that the national as a whole is likely wealthier than it would have been if it had run balanced budgets.

-

This entire complex seems inextricably bound up in the phenomenon Mike Mandel is trying to detail. I think I understand his point to be this: we look at our national statistics and think that we are getting better at turning raw materials into goods and services using traditional engineering expertise. Instead, we are getting better at using our special economic position to engineer favorable terms for goods supplied to US Multi-nationals. While the first represents a knowledge base that is more or less stable, the second depends on our unique position in the world, which is not likely to last.

-

Its not clear to me that this has worked out well for lower skilled Americans. We have a tendency to think that productivity gains will just flow down to the bottom. Yet, there is no magical reason for that. It has traditionally happened because spillover effects could not be captured, knowledge built on knowledge, etc. However, a world in which gains are being created in ways that can be captured is not necessarily a world in which the poor benefit from those gains. Thus, despite our strong intuition otherwise, the counterfactual in which the US didn’t have this special position might be better for low income Americans.

-

This position – at least at first glance – seems good for the world as a whole. In some international finance discussions it is noted that the dollar regime may have been crucial to allowing nations to safely build up large current account surpluses. It occurs to me that this may be a general phenomenon. We think of the economic advantage of banks is that they allow more investment by providing relatively cheap loans. However, they may also “allow” more work in that they make it safe for individuals to run large current account surpluses at a given time. If there were literally no way to do this then there would be a strong decreasing marginal return to work simply because there was nothing to you could do to store the proceeds. Even holding it in precious metals risks theft. A safe storage vehicle is then a compliment to supplying labor.

Because I didn’t want to register with the UK government site on which Leigh Caldwell posted his ideas for behavioral analysis in the structure and deployment of services, I’ll comment here.

The rationale for Leigh’s wild and irresponsible proposals*:

While some behavioural interventions are being explored through the Cabinet Office’s Behavioural Insight Team (with some success) these tend to be relatively simple adjustments to framing of specific choices available to citizens. A deeper re-examination of the economic assumptions used in public service contracting and forecasting could lead to real improvements in outcomes and efficiency.

Some specific sectors that Leigh targets:

- Health care, where behavioral modelling of the consumption of health services may lead to more efficient deployment and use of resources.

- Education, where behavioral analysis could help bring incentives and signalling in line with cost savings in order to reduce spending while maintaining quality.

- Welfare and social security, where structuring incentives could help raise people out of poverty by building productivity, and encouraging formation of savings. Thus, reducing dependence on the state in the long run.

Now, I’m only a smidgen a behavior economist (having read varied works from the Santa Fe institute), but I’ve always been at least cautiously optimistic about the prospect of what Richard Thaler refers to as “libertarian paternalism“. Leigh is a crazy lefty*, but I trust that he believes in choice, and understands that choice is often not the problem in and of itself. Choice sets often are given various cognitive biases. Thus, choice architecture can preserve the ability of the individual to make a choice, but incentivize choices that are in the best interest of the decision maker.

I’m not too familiar with the first two categories Leigh lists, but I am broadly familiar with the third (which is the most “popular”). There are several ways in which the government could better structure incentives to produce superior long-run results, but I want to focus on one real-world example. The Oportunidades program, an the anti-poverty program in Mexico. The program is centered around providing cash transfers that are linked to incentive goals: