You are currently browsing the tag archive for the ‘NGDP’ tag.

From the Washington Post:

The European Central Bank offered new emergency loans to banks on Thursday to help them through the turmoil of the government debt crisis, but decided to keep interest rates on hold despite fears of an economic slowdown.

Remember what happened last time a central bank failed to let rates fall to zero (nay, failed to let rates fall at all!), failed to commit to an explicit level target, and instead made what were widely understood to be temporary injections into the banking sector? Here’s a hint, it happened in October 2008, in the United States.

Also, this is nearing sadistic:

“Have we delivered price stability? Yes, we have delivered price stability,” he (Trichet) said. “Are we credible in delivering price stability over the next 10 years? Yes. These are not words, these are deeds.”

[h/t Matt Yglesias]

There has been a lot of praise about Obama’s jobs speech that he delivered last night, both in style and in substance. I thought the style was just fine, and has set Obama up in a position where he can clearly smack Republicans in the general election should they resort to obstructing the American Jobs Act. And they shouldn’t! It’s a very Republican-friendly plan and I do have to say that I admire many of the different projects on merits, but I can’t help by think that the plan and the subsequent cacophony of commentary is fiddling around the edges while dodging what has been the fundamental problem of the last few years — a problem that only the Fed can remedy — and that is abysmal growth in nominal spending.

The plan broadly consists of three classes of measures, the first is cutting the payroll tax on both the employer and employee side. Along with my co-blogger Karl, I am in favor of this proposal as a measure to remove supply side barriers to new hiring. While Karl’s preferred plan is to cut the payroll tax to zero, this plan is none-the-less fairly bold…however, I am skeptical that it will deliver the amount of new hiring that Obama is promising.

The second measure is tax incentives for hiring specific classes of people. In this case, there is an incentive for hiring veterans, the long-term unemployed, and for giving raises to current employees. I am roundly not in favor of this type of policy, especially the incentive to artificially prop up wages. The last time this was tried as a counter-recessionary measure was the 1933 National Industrial Recovery Act (which subsequently choked off the fastest recovery in American history). Now, it is hardly the case that money wages will jump 20% overnight after the passing of this bill, but if you’re in the business of wanting to to jump-start new hiring, incentivizing higher wages (and thus, necessitating higher productivity) is clearly the wrong way to go about it.

The third part of the plan is direct spending on infrastructure — namely schools and transportation. Sure, great, do it! Real rates are at zero or below all the way out to 10 years…that means (as has been pointed out ad nauseam) it’s cheaper to borrow than to tax now, and defer taxation to the future, when there will presumably be robust growth. I don’t know the specifics, but I’ve heard talk about an infrastructure bank that will provide safe, liquid assets to private investors and provide loans to contractors. It is all well and good that the government maintain infrastructure that is already in the public domain…after all, we’ve already built it, and built our lives around it, might as well maintain it until such a time we devise a different arrangement. My problem is with characterizing infrastructure spending as “stimulus” that will “employ millions of people”. There are plenty of hurdles to jump there, and the spending is slow. Worthwhile “shovel-ready” projects, while much talked about, always fail to materialize at the time they are needed.

Whatever the well-meaning intentions of the designers of these plans, I heard nothing from Obama or anyone else regarding the real issue, depressed nominal spending. Imagine a scenario in which the AJA takes effect, and achieves the maximum spending multiplier ever dreamed up in a model. All of this extra nominal spending (demand) would eventually lead to rising prices, most immediately in sensitive commodities such as food and energy. Now, imagine that the monetary authority views sub-2% inflation as optimal…and is internally pressured to begin unwinding their balance sheet (tightening policy). Rapidly rising prices would be a great cover that would allow them to choke off any good created by the miracle supply-side fiddling that you engaged in with your jobs act. I was disappointed by the prospects of further monetary easing in Bernanke’s Jackson Hole speech. However, there has been a lot of clamoring around the blogosphere (even making it to the WSJ) regarding the actions of the Swiss National Bank. Perhaps I’ll be gleefully proven wrong!

Obama’s plan will succeed to the extent that the Fed allows it…and just for reference, here is the Cleveland Fed’s expected inflation yield curve:

[Click Image to Enlarge]

Today, Barney Frank introduced legislation in committee to remove regional Fed presidents from the FOMC:

U.S. Rep. Barney Frank (D., Mass) Tuesday introduced a bill that would let interest rates be set only by Federal Reserve officials picked by the government, a new attempt to move power away from regional Fed officials chosen by the private sector.

The bill would remove from the 12-member policy-setting Federal Open Market Committee the five members who represent regional Fed banks. Only the seven-member board in Washington, which currently has two vacant seats, would get to vote on interest rates. The congressman said this would make the Fed more democratic and increase “transparency and accountability on the FOMC” by eliminating those officials who are effectively picked by business executives

Now, I have never been a fan of Barney Frank, but I do see merits in this legislation. However, first a contrary opinion, courtesy of Mark Thoma:

I can support – and have advocated — reforming the way in which regional bank presidents are selected. But this proposal, which removes geographical representation even though recessions do not hit each area of the country equally, is a bad idea (the Board of Governors can already veto the appointment of a regional bank president, though I don’t know of any instances where this power has been used). It takes us further away from the populist roots of the Fed’s structure, a structure that tried hard to represent all interests in policy. It also furthers the concentration of power in Washington that has been occurring slowly but surely ever since the Bank Reform Acts in the wake of the recession established the Fed’s current structure. In addition, it takes another step toward increasing the power of Congress over day to day monetary policy…I hate to even imagine how bad things would be if Congress had been in charge of monetary policy.

…reform the selection process for regional bank presidents, but don’t increase the concentration of power in Washington…I would like to see, at a minimum, less representation of business so that the public interest generally can take center stage.

While I can stand broadly stand behind the anti-concentration of power sentiment, if you have regions of a country which fluctuate so wildly from baseline that their performance creates a necessity for special accommodation from monetary policy in general, that is an OCA argument against having a single currency area. David Beckworth has argued that the “rust belt” in the US could have possibly benefited from its own currency over the last decade, and I agree!

Do we need regional Fed presidents at the table? After all, in the Great Contraction of 2008, and the ensuing recession, it has been the regional presidents that have provided the voice of hawkishness, even through tumultuous 2009! So when the chips are down, and adequate monetary policymaking is at its highest stakes, these guys were wrong…and being that they largely represent banking interests, they are likely biased against inflation at all costs. This certainly hasn’t been any help to our recovery!

Thoma is worried about Congressional power eroding sound monetary policy decision-making…but our current Fed structure doesn’t prevent that, indeed, it probably enhances it!* After all, Bernanke held the first press conference amid rising populist fears stoking an encroaching Congress’ ire regarding monetary policy. When Mark hopes that public interest would take center stage — and I do as well — but I don’t see how reforming the Fed presidents’ selection process is superior to having a board that is wholly selected by the President, and approved by Congress. If you want to do 12 members that way, so be it!

However, while Barney Frank’s motivation is mostly suspect, sometimes even then you stumble upon a good idea…but this idea isn’t good enough. If you are in a position where your legislation has little chance of making it out of committee, my play would be to lay all of my cards on the table: rewrite the Fed charter such that it requires the Fed to set one nominal target, and keep it on a level growth path. I would prefer NGDP, as I believe that targeting nominal spending is far superior to targeting inflation. This is obviously not Frank’s goal, and it would likely go against Franks (poor) instincts as it removes the unemployment portion of the mandate…but the level of employment in an economy is a real variable.

So what if trend NGDP was perfectly on target, but unemployment remained uncomfortably high. Is that a reason for monetary policy to act? Well, it could be…but there are other questions to ask of other policymakers. What are the structural problems? If there are supply side rigidities, look at removing them (not just removing specific laws, but increasing education, etc.). If you are uncomfortable with removing them, then live with higher joblessness. If there happened to have been an extremely productivity-enhancing technological development (like mass teleportation?) that is causing persistent unemployment because it significantly increases the return on capital investment vs labor investment, then perhaps the long-run growth potential of the economy has been increased — if that is the case, monetary policy may need to target a higher growth path for NGDP.

So, to sum it up, I think removing regional Presidents does make the board more accountable, and it would probably also improve the decision-making process. And if you really wanted to reform the Fed with an eye toward independence, remove the dual mandate and institute a explicit nominal target.

*Imagine a Congressional hearing under an NGDP targeting rule. What would it consist of?

Congressman: “Is NGDP on target”?

Fed Chair: “Yeop”.

Congressman: “Lets get lunch”.

That is obviously a joke, but it is the wiggle room created by the confusing dual mandate that allows Congress to leverage nearly all of its power against the bank.

David Frum, commenting on the Keynes vs Hayek rap video released last week, makes a point that I noticed throughout the video as well:

The economic question we have faced since 2008 is not: “Shall the government of the United States dictate prices and production throughout the US economy?” Who advocates that? Not Larry Summers. Not Tim Geithner. Not Ben Bernanke. And if there’s any tiny remaining sliver of Barack Obama’s being that wishes for central planning, it to this day remains profoundly hidden beneath all his contrary appointments, policies, and pronouncements.

Throughout the video, “Keynes” asserts that in a depression, we need to start the flow of spending, to boost aggregate demand to a level in which the economy can sustain itself. Keynes, and modern Keynesians, believe(d) that fiscal policy could take up the torch of private spending while household balance sheets were mended, and that the boost in GDP would help us recover more quickly. And, while “Hayek” had some really brilliant lines throughout the video (“…if every worker was staffed in the army and fleet/we’d have full employment and nothing to eat…“, and my favorites: “…jobs are a means, not the ends in themselves/people work to live better, to put food on the shelves/real growth means production of what people demand/that’s entrepreneurship not your central plan…” and “…the economy’s not a car, there’s no engine to stall no expert can fix it, there’s no “it” at all…“), you’ll notice that through nearly all of the video, he is making a generalized argument against central planning. They’re talking past each other, or at the very least perceiving themselves as having two different conversations.

However, Frum runs into trouble with this:

The Hayek character says, “I feel for the suffering, I’m not some kind of jerk.” The Keynes character answers, “Now my old friend, I’d never reject you as if you were heartless, you know I respect you.”

But the suffering want more than “feeling.” They want a policy response. And it is precisely a policy response that our modern self-described Hayekians preclude. Monetary policy? No can’t do that – it only leads to inflation and more bubbles. Stimulative government spending then? No that’s out, it leads to inflation, bubbles, etc. Tax cuts for the ordinary working person such as the payroll tax holiday? No way – we must balance the budget. So that leaves only supply-side tax cuts aimed at the upper-income brackets. balanced by large immediate budget cuts in Medicaid, food stamps, unemployment insurance. Does anybody believe that such a policy mix will lead to rapid employment growth? The Heritage Foundation claimed so, for approximately 48 hours, but now even they have abandoned that assertion.

To the question: What do you do in a deflation, Keynes offered an answer. He intended his answer as a means to preserve exactly the kind of spontaneous order praised by Hayek. Keynes lived and died a liberal in the old sense of the term. There are many criticisms of the Keynesian answer, mostly having to do with that long term that he so famously shrugged off. But some answer is better than no answer – and much better than the answer offered by the modern self-described Hayekians.

I don’t know about “modern, self described Hayekians” (actually I do, but I don’t want to speak for them), but this wasn’t Hayek’s position at all. As Larry White has pointed out in a JMCB article:

The Hayek-Robbins (“Austrian”) theory of the business cycle did not in fact prescribe a monetary policy of “liquidationism” in the sense of doing nothing to prevent a sharp deflation. Hayek and Robbins did question the wisdom of re-inflating the price level after it had fallen from what they regarded as anunsustainable level (given a fixed gold parity) to a sustainable level. They did denounce, as counterproductive, attempts to bring prosperity through cheap credit. But such warnings against what they regarded as monetary over-expansion did not imply indifference to severe income contraction driven by a shrinking money stock and falling velocity. Hayek’s theory viewed the recession as an unavoidable period of allocative corrections, following an unsustainable boom period driven by credit expansion and characterized by distorted relative prices. General price and income deflation driven by monetary contraction was neither necessary nor desirable for those corrections. Hayek’s monetary policy norm in fact prescribed stabilization of nominal income rather than passivity in the face of its contraction.

The bolded line is important, because if you take the Sumnerian theory of the Great Recession seriously, or even the most common explanation of events leading to the Great Contraction (’29-’32), the problem is that the monetary authority (the Federal Reserve) allowed NGDP expectations to fall off a cliff in late 2008 by passively tightening monetary policy…and that is exactly the opposite of what Hayek would have considered proper macroeconomic stabilization policy. As I understand Hayek’s NGDP rule, the central bank should stabilize M for any given V, consistent with zero aggregate growth in in the price level (PY), which would result in the type of deflationary growth that Hayek (and George Selgin) advocated.

No need to take White’s interpretation, though, here’s Hayek himself, agreeing with Keynes on the matter of deflation (though not the prescription of government expenditure, which is redundant with a NGDP level target):

On the first issue — whether to use one’s money or whether to hoard it — there is no important difference between us. It is agreed that hording money, whether in cash or in idle balances, is deflationary in its effects. No one thinks that deflation is in itself desirable.

Really, on the issue of monetary policy, I see Keynes and Hayek arguing together against the ever-popular real-bills doctrine

The debate about central planning was indeed contemporary in the 30’s, and today I think many libertarians don’t recognize or appreciate the extent to which we’ve won on that point…Hayek, indeed had a good (and I believe superior) answer to Keynesian fiscal policy…but you unfortunately won’t find it in the Keynes/Hayek video.

Note: I’m not foremost expert on Hayek, but I’m sure that if Greg Ransom (and others!) reads this blog, he will correct my errors in the comments!

Update: Tyler Cowen makes the same point in a single sentence…bet you wish I had put this update at the top ;].

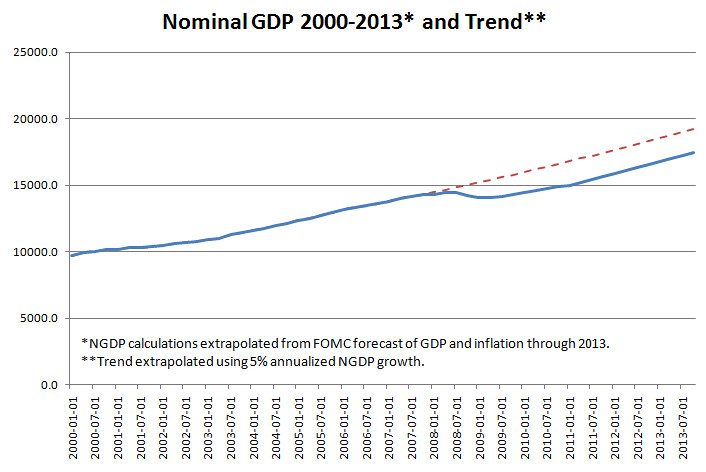

“A slow sort of country!” said the Queen. “Now, here, you see, it takes all the running you can do, to keep in the same place. If you want to get somewhere else, you must run at least twice as fast as that!” -Lewis Carroll, Through the Looking Glass

I have constructed a chart extrapolating the trend growth in nominal GDP* through 2013, along with the FOMC’s forecast of nominal growth through 2013.** Have a look:

[Click Image to Enlarge]

As you can see, by the Fed’s own forecast, we will remain under trend growth in NGDP through 2013. Indeed, by the fourth quarter, we will be 10.2% below the trend. That is roughly $1.7 trillion in potential output! I regard this as the “one chart to rule them all”, and it is what I point to when people ask me why we are experiencing a sluggish “jobless” recovery.

Always keep in mind, though, prediction is a fools errand over anything but the shortest of time spans. The key here is that there is only one way the prediction can be off such that it would benefit the economy. Those aren’t good odds to take.

*FRED

**Average of the central tendency.

I, for the life of me, can not understand where Stephen Williamson is coming from in the recent posts he’s done claiming that Quantitative Easing is ineffective, and that the Fed is completely out of tools which it can use to boost the economy. Here are the points he made from his most recent post, entitled “Mark, Brad, and Ben“:

- Accommodative monetary policy causes inflation, but with a lag. I think Brad’s inflation forecast is on the low side, as maybe Ben does as well. The policy rate has been at essentially zero since fall 2008. Sooner or later (and maybe Ben is thinking sooner) we’re going to see the higher inflation in core measures.

- Maybe Ben is more worried about headline inflation (as I think he should be) than he lets on.

- Maybe in his press conference Ben did not want to spend his time explaining why the Fed spends its time focusing on core inflation. What every consumer sees is headline inflation, and they are much more aware of the food and energy component than the rest of it.

- As with my comments on Thoma, there is really no current action that the Fed can take to increase the inflation rate. More quantitative easing won’t do anything, so the Fed is stuck with saying things about extended periods with zero nominal interest rates in order to have some influence through anticipated future inflation on inflation today.

Most of the list simply baffles me. First of all, accommodative monetary policy can cause inflation. And of course in the long run, a stable monetary policy only affects prices…but the blanket statement that monetary policy causes inflation is misleading, and highlights a problem with even talking about inflation. In a standard AS/AD model, the determinant of the composition of NGDP growth is the slope of the SRAS curve. In recessions, it is generally understood that the SRAS curve is relatively flat. In that case (arguably the case we are dealing with right now), an accommodative monetary policy which shifts the AD curve to the right would result in much higher output growth than inflation. As for the lag part, monetary policy has an almost immediate (< one quarter) impact on many markets; including interest rates, stock/commodity prices, inflation expectations, etc. Here is a chart of those market reactions to both QE's courtesy of Marcus Nunes:

[Click Image to Enlarge]

In each case, you can see that asset prices had a quite immediate response to quantitative easing. QE2 performing poorly doesn’t indicate that QE doesn’t work, it highlights problems with how the policy was implemented. Specifically, the Fed structured the policy around purchasing a specific quantity of Treasuries ($600bn) instead of setting a target level of nominal spending, or even a price level target, and then commit to purchases until that target has been reached.

Second, why would Ben Bernanke be worried about headline inflation when nearly every forecast from the Federal Reserve views the current rise in headline as temporary? Here is the SF Fed, which I posted earlier:

[Click Image to Enlarge]

Indeed, the FOMC’s own report states as much. Furthermore, we have a good idea of what is causing the bump in headline inflation, and that is the energy prices. We also have good reason to believe that this is due to rising demand in the briskly growing emerging markets, and the inability to ramp up supply. What in the world is monetary policy supposed to do about that? Is Williamson advocating tightening policy while NGDP is still FAR below trend, and we are not experiencing enough growth to catch up to the previous trend?

I don’t have many quibbles with the third point, but the fourth point is the one that floored me the most. I’ll outsource commentary to David Beckworth in a comment on Williamson’s post:

Steve,

Why do you keep saying there is nothing the Fed can do? You acknowledged in the comment section in your last post that the Fed could do something more via a price level or ngdp level target. By more forcefully shaping nominal expectations with such a rule the Fed could do a lot.

It is worth remembering that folks were saying the same thing about monetary policy in the early 1930s. They were certain there was nothing more the Fed could do and as a consequence of this consensus we get tight monetary policy and the Great Depression. Then FDR came along and change expectations by devaluing the gold content of the dollar and by not sterilizing gold inflows. His “unconventional” monetary policy packed quite a punch.

And here is my comment:

I’m with David on NGDP targeting. But even if the Fed didn’t do that, it has its interest on reserves policy, and the last I checked, it hasn’t set an explicit inflation level target, and there is ~$14 trillion in outstanding Treasury debt held by the public that the Fed does not yet own…something Andy Harless has pointed out on numerous occasions.

Here is a data point given by Glenn Rudebusch (h/t Mark Thoma), vice president of the San Francisco Fed, in the recent FedView:

A simple rule of thumb that summarizes the Fed’s policy response over the past two decades recommends lowering the federal funds rate by 1.4 percentage points if inflation falls by 1 percentage point and by 1.8 percentage points if the unemployment rate rises by 1 percentage point. Either headline inflation or core inflation can be used with this rule to construct policy recommendations. Relative to a core inflation formulation, a policy rule using headline inflation would have called for a higher fed funds rate in 2005-2006 before the recession and in 2008 in the midst of a deepening recession. Currently, both formulations call for substantial monetary accommodation.

The Fed, in it’s October meeting (after Lehman had failed on Sept. 16th) lowered their target fed funds rate only 50 basis points to 1.50. That week (Dec. 6th-10th), the DJIA fell 18%, but it wasn’t until Oct. 29th that the Fed met hastily in an emergency meeting to cut rates…50 basis points, to 1.00. What metric could they have been watching that would suggest (in a historical sense) that inflation was the problem, and not deflation? It could only have been headline inflation!

[Click Image to Enlarge]

Core inflation has closely tracked a median ever since the Fed concerned itself with keeping inflation low (and stable). But what you really have to ask yourself is; what good is having a target when you are able to move between whatever measure suits your inclination at the moment? There is, of course, a mechanism by which inflation in energy prices (and thus broad inputs) can translate into a higher trend in core inflation (60’s-80’s), but this hasn’t been the case for thirty years.

The key here is that monetary policy should not be engaged in inflation targeting. Inflation is a symptom of an underlying problem (AD or AS shock), for which the Fed can only react to AD. If the Fed concerns itself with reacting to AS shocks, then we end up where we were in late 2008, with plummeting NGDP. The Fed should target the variable that it has control over, and keep it growing at a stable long-run rate.

Update: Accidentally hit the “Publish” button instead of preview. In any case, the SF Fed’s forecast is that the rise in commodity prices is unsustainable given the level of depressed aggregate demand in much of the world economy. Here is the chart:

The SF Fed also predicts a persistent (and rather large) output gap through 2012! That is a monumental failure of monetary policy.

In his Kentucky Day with the Commissioner (?) presentation today, James Bullard makes the case for targeting headline inflation. This is likely consistent with the recent hawkish turn he has taken, but is it correct? Is it true that we should expect core inflation to be a predictor of headline inflation, as he suggests?

First things first, though. Bullard proclaims victory for the quasi-monetarists:

This experience [rising asset prices in multiple markets, including stocks, bonds, commodities, as well as declining real interest rates and a depreciated dollar] shows that monetary policy can be eased aggressively even when the policy rate is near zero.

But then Bullard takes a turn toward hawkish land, with five points regarding core vs. headline inflation:

- Headline inflation refers to overall price indexes.

- Core inflation refers to the same indexes, but without the food and energy components.

- Core inflation is often smoother than headline inflation.

- Core eliminates 20% or so of the prices in the index.

- The “core” concept has little theoretical backing. It is very arbitrary.

Here is my problem: Our measures of inflation are both dubious at best, and a lagging indicator. The focus on headline inflation in the run-up to the crash of 2008 is the reason why monetary policy failed. Nowhere in the talk did Bullard mention unemployment, which I view as a good thing. However, he could have mentioned that a wage-price spiral requires that wages spiral, as well. That doesn’t seem to be happening:

[Click Image to Enlarge (h/t Paul Krugman)]

I didn’t hear the lecture, but from reading the notes, I’m quite confused. Does Bullard believe that the current spike in headline inflation is a trend, and why? Furthermore, should the Fed be targeting where inflation has been, or the forecast of future inflation, which is within a reasonable range as of right now.

[Click Image to Enlarge]

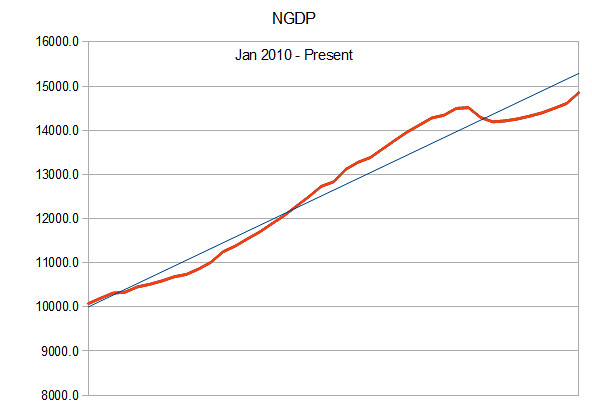

It all seems to me to strengthen the case for NGDP level targeting. Then we wouldn’t be having these silly debates. All you have to ask is: “Is NGDP growing on target?”

[Click Image to Enlarge]

Not quite yet. And furthermore, I would argue that we need a period of above-trend growth in NGDP in order to get capacity utilization level to their previous trend as quickly as possible. There may be merit to shifting to a lower trend rate of NGDP growth, but not at a moment when capacity utilization is low, and unemployment is high. In short, I see no threat of the current headline inflation pressures translating into accelerating inflation. The Fed should continue to be accommodative until at least the point that we reach the previous trend level of NGDP.

P.S. Sorry for the incredibly bad charts. For some reason, Excel is force closing on my computer now, and I had to switch to using Openoffice.org. I am less than impressed, to say the least.

Here’s a piece from David Leonhardt that has been getting some of play on blogs that I frequent. It’s definitely good to see that more of the profession are coming around to the “quasi-monetarist” view that monetary policy is not impotent at the zero bound, that it can do much more. Here’s David:

Whenever officials at the Federal Reserve confront a big decision, they have to weigh two competing risks. Are they doing too much to speed up economic growth and touching off inflation? Or are they doing too little and allowing unemployment to stay high?

It’s clear which way the Fed has erred recently. It has done too little. It stopped trying to bring down long-term interest rates early last year under the wishful assumption that a recovery had taken hold, only to be forced to reverse course by the end of year.

Given this recent history, you might think Fed officials would now be doing everything possible to ensure a solid recovery. But they’re not. Once again, many of them are worried that the Fed is doing too much. And once again, the odds are rising that it’s doing too little.

Indeed. Myself and others have been emphasizing that the passivity of the Federal Reserve in late 2008 (or, as I like to tell it, the Fed being hoodwinked by rising input costs) was indeed an abdication of its duties…but what duties are those? It’s unclear, because the nature of the Fed’s mandate allows it to slip between two opposing targets at will. Michael Belognia, of the University of Mississippi (and former Fed economist) makes a similar point in this excellent EconTalk podcast. The big issue, as I see it, is the structure of the Fed’s mandate. Kevin Drum (presumably) has a different issue in mind:

Hmmm. A big, powerful, influential group that obsesses over unemployment. Sounds like a great idea. But I wonder what kind of group that could possibly be? Some kind of organization of workers, I suppose. Too bad there’s nothing like that around.

I think this idea of “countervailing powers” needed to influence the Fed is wrong-headed. There is no clear-cut side to be on. Unions may err on the side of easy money…but then again, Wall Street likes easy money* too, when the Fed artificially holds short term rates low. It’s all very confusing. But that’s arguably great for the Fed, because confusion is wiggle room…however it’s bad for the macroeconomy, because confusion basically eliminates the communications channel, stunting the Fed’s ability to shape expectations.

Now here’s the problem as I see it: NGDP is still running below trend, and expectations of inflation are currently running too low to return to the previous trend. Notice, I said nothing about the level of employment. Unemployment is certainly a problem, but the cause of (most of the rise in) unemployment is a lower trend level of NGDP.

Given that you agree with me about the problem, which is the better solution:

- Gather a group (ostensibly of economists) to press to rewrite the Fed charter such that the Fed is now bound by a specific nominal target, and its job is to keep the long run outlook from the economy from substantially deviating from that target using any means possible.

- Find an interest group with a large focus on unemployment to back the “doves” in order to pressure the Fed into acting more aggressively.

I would back number one over number two any day. And the reason is that while I’m in the “dove” camp now, that isn’t always the case. At some time, I’ll be back in the “hawk” camp, arguing against further monetary ease. Paul Krugman has recently made the same point about using fiscal policy as a stabilization tool. My goal is to return NGDP to its previous trend, and maybe make up for some of the lost ground with above trend growth for a couple years. That would solve perhaps most of the unemployment problem.

But say it doesn’t. Say we return to a slightly higher trend NGDP growth level for the next couple years, and due to some other (perhaps “structural”) issue(s), unemployment remains above the trend rate we enjoyed during the Great Moderation. Would it be correct to say that monetary policy is still not “doing enough”? I don’t think so. At that point, we should look toward other levers of policy that can help the workforce adjust to the direction of the economy in the future.

I’m not say that is even a remotely likely scenario, I’m just trying to illustrate the complexity and possible confusion (and bad policy) that could come out of a situation that Drum seems to be advocating. Better in my mind to have a rules-based policy than an interest group-pressure based policy.

P.S. This was the first post I’ve ever written using my new Motorola XOOM tablet. It wasn’t the hardest thing I’ve ever done, but it was by no means easy. And I wanted to add some charts, but that would be particularly annoying.

*Which, of course, is not necessarily easy money, just low interest rates.

He’s always taking hiatuses from blogging, and claiming to be “travelling”. Now I know that he has been leading a double life. From Romer’s interview with Ezra Klein:

EK:You’ve also criticized the Federal Reserve for not doing more. What would you like to see them doing?

CR:I’m teaching a course this semester on macro policy from the Depression to today. One thing I had the class read was Ben Bernanke’s 2002 paper on self-induced paralysis in Japan and all the things they should’ve been doing. My reaction to it was, ‘I wish Ben would read this again.’ It was a shame to do a round of quantitative easing and put a number on it. Why not just do it until it helped the economy? That’s how you get the real expectations effect. So I would’ve made the quantitative easing bigger. If you look at the Fed futures market, people are expecting them to raise interest rates sooner than I think the Fed is likely to raise them. So I think something is going wrong with their communications policy. They could say we’re not going to raise the rate until X date. Those would be two concrete things that wouldn’t be difficult for them to do. More radically, they could go to a price-level target, which would allow inflation to be higher than the target for a few years in order to compensate for the past few years, when it’s been lower than the target.

All kidding aside, this is policy advice gold. I can broadly agree with all that Romer is saying in the whole thing. I’m not gung-ho about using fiscal policy and expecting it to “work” in the sense that it raises NGDP to a level which is consistent with returning to trend quickly (especially with a conservative central bank), however I don’t see anything wrong with smoothing the edges of recession by helping people through the tough time using fiscal policy (mostly simple transfers), and of course reducing employment during a recession. As prescribed here (not by Mark Thoma, but by a paper circulated by John Boehner), is asinine.

P.S. I think that the level of suffering an economy would have to deal with as the result of sharp deficit reduction is directly related to the willingness of a central bank to accommodate the policy.

Karl posted something that he should have titled “Stream of Consciousness” instead of “Unsubstantiated Claims” where he thought out loud. One of those thoughts landed on the Fisher effect.

My sloppy writing makes it sound as if I am saying Reihan should read up on the Fisher effect. What I mean to say is that Reihan brought up the fact that people fear inflation eroding savings. These fears are common. I have had many a Facebook debate over them. Indeed, Ron Paul has repeatedly pointed to this has his main reason for fearing debasement of the currency.

I believe that the Fisher effect is controversial among Austrians, and Keynes didn’t believe in the relationship at all, except under hyperinflation. Using price inflation in the Fisher equation makes a lot of things confusing, because the composition of output under recession circumstances (less than full employment — or a flat SRAS) is that raising inflation expectations to, say, 3% from 2% will likely cause an increase in real output, leaving inflation at it’s long-run target. Indeed, the Fed isn’t even interested in boosting inflation expectations past its set 2%, and has made that very clear. What the Fed wants is higher NGDP…but unfortunately it operates under a target for nominal interest rates.

Scott Sumner has a post about how inflation is, counterintuitively, good for savers. The thrust of it is that raising NGDP expectations will raise the Wicksellian real interest rate. People will spend more on investment (maybe not consumption, but probably), and we will get far more output, while trend inflation remains intact (and if it doesn’t, then the Fed can act as necessary). This is a boon to savers, as it raises not only the interest rate on savings accounts, CD’s, and the yield on bonds…it raises other asset prices as well, like stocks, real estate, commodities, etc. All are vehicles for saving, and a higher level of NGDP causes every type of investment to increase its yield.

This is the fundamental reason inflation is confusing. People think a lot about cash, but not many people save in cash (as in safes) under a normal positive trend inflation rate — criminals mostly. I think that price inflation is just muddying the debate here, and is completely useless.

A little late, I know, but Happy Thanksgiving everyone!

Remarks from Ben Bernanke indicate that the Fed is shooting itself in the foot:

“I have rejected any notion that we are going to try to raise inflation to a super-normal level in order to have effects on the economy,” [Bernanke] said.

In fact, the Fed should engage in level targeting, as I have been pushing in the last few posts. It should commit to a higher target for nominal expenditure in order to return to the previous trajectory from the Great Moderation. That requires a higher level of NGDP growth than is “normal” in order to catch up. One way to do this under the current monetary regime is to create higher inflation expectations. Do they need to be much higher? I don’t think so, but it’s not entirely unreasonable to disagree.

So we know that most members of the FOMC view 2% as the preferred inflation target. We now also know that the Fed is holding true to that target, come hell or high water. 2% is better than 1%, but a temporarily higher target would produce a much more robust recovery. Arguably, the Fed is in the business of providing stable NGDP growth consistent with high employment and low inflation. It allowed NGDP to plummet and now they should be trying to make up that lost ground as quickly as possible. This statement is clearly against that goal.

We’re in for a rocky road if our monetary authority sees it fit to tie its hands.

In a Times article a few days ago is this interesting quote from Laurence Meyer, a former Fed governor:

It was this impending gridlock that might have pushed Mr. Bernanke to move, said Laurence H. Meyer, a former Fed governor. “Bernanke has said that fiscal stimulus, accommodated by the Fed, is the single most powerful action the government can take for lowering the unemployment rate, when short-term rates are already at zero,” Mr. Meyer said. “He has nearly pleaded with Congress for fiscal stimulus, but he can’t count on it.”

I’m taking this as a explicit, and unshrouded nod to the concept of “money financed fiscal policy”. Or, what is lovingly referred to in the press as “monetizing debt”. This is a situation where the government draws up a plan to distribute money, whether through direct transfers or increases in government consumption/investment, has the Treasury issue debt in the amount decided upon Congressionally, which the Fed then purchases with newly-coined money (and for hysterics, this money is created “out of thin air”!).

As Karl has noted, and as concurred upon by commenter Jazzbumpa, a program such as this would inevitably “work”. And by work, I mean it would raise inflation expectations such that businesses would be induced out of cash and into consumption and capital goods. This, of course, is something that the ARRA failed to do. This is true, but it is optimal policy?

I say no. I don’t think that fiscal policy need ever enter the picture. I think that the Federal Reserve should announce an explicit target to get the growth path of nominal expenditure to the previous level from the Great Moderation, and then continue to level target a stable growth path from there. In doing so, the Fed should immediately stop sterilizing its own open market operations by paying interest on excess reserves (indeed, the interest in reserves should be slightly negative, reflecting real rates). The Fed could then move down the yield curve, and buy Treasury debt that currently resides on the balance sheets of banks, businesses, and individuals; moving the price up while moving the yield down to zero. I suspect that there is enough debt out there that it would not run out of things to buy before hitting its nominal target. However, if it does, then it can move on to other assets.

The key thing here is that there are many interest rates in the economy, and not all of them are pegged at zero. My point is that far from needing to bring fiscal policy into the picture, monetary policy could go it alone. If the SRAS curve is relatively flat, which is a prediction of macro models, then the resultant inflation expectations would produce much more real output than inflation (lets ballpark and say 5% real growth, 2% inflation), up until full employment is reached — at which point, the Fed would revert to its normal level target. I do not think that Bernanke is “pleading with Congress” for fiscal policy. Why would he? If he identifies that aggregate demand is low relative to the Fed’s own target, then by all means, he should be taking steps to move aggregate demand to where the Fed is most likely to hit their target goals.

To those who say that it is unrealistic that the Fed would do this, is it any more unrealistic than hoping for money-financed fiscal policy?

Inflation is confusing. The concept makes crazy people crazier. And even worse, it makes otherwise sober people disagree with eachother. Reading through the accounts of QE2 on the internet the past few days have solidified my view that inflation is a thorny enough concept that we should rid it from popular vernacular. Is inflation important? Sure…but what measure of inflation is correct? CPI-U? GDP Deflator? Your crazy uncle’s index? Does inflation help or hurt savers in the current landscape?

If there is anything that gets turned on it’s head when an AD recession hits, it is the concept of inflation. During normal times (full employment and capacity utilization), inflation is harmful as it drives up interest rates, discourages saving, and encourages misallocation of capital. However, none of those things apply to the current situation in which we find ourselves with a large output gap and high unemployment. Thus, we need higher inflation in order to close the output gap (the difference in money expenditures between where we are currently, and the trend rate from the Great Moderation…currently about -13%), but that turns everything that everyone knows about inflation backward. All of a sudden inflation is good for savers, good for the unemployed, and good for economic growth. Well, stable inflation expectations are key…but it’s hard to steer a ship, and it’s hard to get a non-confusing answer out of pundits and other commentators.

In order to square this circle, I propose we forget about inflation. And not just forget about talking about it, but forget about its use in the setting of monetary policy. Instead, we should target nominal expenditure at a steady growth rate (3% a la Woolsey, or 5% a la Sumner, Beckworth, etc.) with level targeting. What advantages does targeting nominal expenditure have? Well…

- Targeting nominal expenditure (NGDP for short) allows monetary policy to better address recessions which arise from both aggregate supply and aggregate demand shocks. David Beckworth has an excellent discussion of this point.

- NGDP is a better indicator of monetary shocks than inflation indicators like CPI. Because prices are sticky, and because measures of inflation are so problematic, a fall in NGDP won’t immediately show up in inflation numbers. Also, if there is a large price shock in something like oil, this will raise the money price of all goods and services, causing anyone focusing on inflation to miss the underlying weak economy…and thus potentially set monetary policy to be too contractionary (sound familiar?).

- NGDP allows us to broaden our focus to aggregates like MZM, asset prices, yields, excess reserves etc. We’ll relinquish our inane focus on interest rates, which are a very problematic indicator of the stance of monetary policy, and have a much better picture of the health of the economy.

- NGDP sounds better. People have an innate fear of inflation. Inflation destroys savings, after all…and we all know frugal people are virtuous. Well, how about, in the event of a recession, instead of economists clamoring against the crowd that we need inflation, they say that we want aggregate expenditures (and thus nominal income) to be at some level higher than it currently is? Money illusion is a powerful motivator. Who would argue with that?

Targeting nominal expenditure would be a beneficial step from both an economic theory perspective, and a public relations perspective. Lets take the confusing concept of price inflation out of our discourse, so that we can see the world more clearly.

P.S. We are currently 13% below the target path from the Great Moderation, and are where we were at before the crash of Sept/Oct 2008. To make that up by 2011:Q3, the Fed would have to target NGDP at $17.6bn (to continue on a 5% NGDP growth path). However, Bill Woolsey favors a 3% growth path for money expenditures, which means that the Fed would only have to target a 13.8% increase by 2011:Q3 (or $16.4bn), and then continue on with 3% growth, level targeting, from then.

Update: Found the link to Beckworth’s article!

I was going to write up a post on my exasperation at the Fed’s recent meeting statement, but Ezra Klein got to it before me and did a good job, so you should go read what he has to say. One point that I want to highlight, because I have made the point that the dual mandate is mostly just an insiders joke:

Paragraph two: We admit everything is terrible. In fact, it’s so terrible that it means we’re failing our mandate. “Measures of underlying inflation are currently at levels somewhat below those the Committee judges most consistent, over the longer run, with its mandate to promote maximum employment and price stability. With substantial resource slack continuing to restrain cost pressures and longer-term inflation expectations stable, inflation is likely to remain subdued for some time before rising to levels the Committee considers consistent with its mandate.”

[Image Courtesy of David Beckworth]

How many of you wish that you had a job where you could consistently fail at the very time when it is clutch that you deliver in a big way? How many of you would like to say, “Well, I have a model of the economy that says we won’t be hitting any of our own targets…but oh well”? The Federal Reserve is in the exact position in the economy where they can act quickly and decisively and actually make a large impact on nominal spending. I would even go as far as to say that they can do so without “long and variable lags”, as markets should price in actions by the Fed nearly immediately, and indeed they have been.

Contrary to the popular narrative, I believe that it is this very passivity by the Fed that brought us to the brink in the fall of 2008, when every indicator of economic activity (industrial output, consumer spending, business confidence, NGDP expectations, etc.) were found to be in sudden free-fall mode. At that time, interest rates were in the 1.5%-2% range, and the Fed’s target was still 2% until October 2008!

And here we are, fully two years later, and we still cannot get the Fed to act…nor can we get the executive branch of government to take the problem seriously! This inaction belies an institution that either is ill-equipped to respond when necessary, or is structured in a way that prevents decisive action. Since I believe that the Fed has all the tools it needs (it being a monetary superpower), I would place the blame on the structure of the network.

There is nothing more important on the Fed’s plate right now than bringing nominal spending back in line with the previous trajectory of NGDP. Not only to assist 50 million people who are currently unemployed, and help numerous others rebuild their balance sheets…but to save our economy from the whims of populist sentiment that will likely take hold if our economic malaise continues for very much longer. That means rounds and rounds of fiscal stimulus. That means the development of an entire class of freeters who never reach full potential. And most importantly, that means the loss of real goods and services that could otherwise be produced in our economy — which translates into a lower real standard of living for everyone.

At this point I would do anything for a little more monetary stimulus.

Scott Sumner routinely forgets my name when listing people who thought money was tight, and favored unconventional monetary responses to the recession…but that’s okay. I wasn’t blogging that much in late 2008. In any case, I would like to provide a concise answer to a question Scott raises on his blog today:

The very fact that Congress and the President are ignoring this issue (confirming FRB nominations), pretty much tells me that they are clueless on monetary policy. On the other hand, both groups do favor more AD, so their “heart” is in the right place. And of course I’m a big believer in democracy. So who do I favor making the decisions; the clueless or the heartless? I’m tempted to say “Whoever agrees with me; first tell me the target Congress would set.” But of course that’s cheating. The honest answer is that I don’t know. But it is becoming increasingly clear that we won’t get good policy until this dilemma is resolved.

In my mind, the myth of an independent central bank has pretty much been shattered (Karl’s as well). Every time the theory of why we have an independent central bank has been put to the test in a big way, the Fed has failed miserably.

But maybe the answer is more nuanced than that. Perhaps the Federal Reserve itself is simply a proximate cause. If you take the view that the actions of the Fed represent the consensus of the economics profession, then perhaps it is the economics profession who are the underlying cause.

In either case, it is clear that there should be hard rules in place that the Fed must abide by. At the same time, I think that the Fed should have maximum room to act independent of politics when it really needs to. Our current “dual mandate” provides nothing but an excuse for the Fed to shirk its duties. Thus, I believe that the Federal Reserve Charter should be rewritten to state that it is the Fed’s contractual duty to set an explicit nominal target, level targeting, and do everything in their power to hit that target. If you ask me I favor NGDP, but some people favor price level, and some favor inflation…if you really want to pin the Fed down, write which nominal target the Fed needs to hit into the charter. NGDP will still be here 100 years from now.

However, and this is important, that is the end of Congress’ power. Once they have arbitrated as to what the Fed needs to do, Congress gets out of the way and lets the Fed act. The only point at which Congress should have the authority to intervene is if the Fed is off-target, in which case Congress should have the power to remove the current board (or specific members) and appoint a new one. But, and this should be written into the charter as well, the only circumstances in which Congress can do so is if the Fed is missing its target (or criminal behavior, or other things that don’t have to do with monetary policymaking).

Separating politics from policymaking is definitely a good thing (I even came around on TARP), especially in monetary policymaking. However, having a monetary authority that is gallivanting around, allowing NGDP expectations to plummet 8% with zero recourse is unacceptable.

Karl has a post today arguing that Brian Wesbury is wrong for taking the view that fiscal stimulus is not effective (indeed harmful!) for two reasons: 1) that it pushes up interest rates through government borrowing (crowding out), and 2) people will expect future taxes to pay for the stimulus.

Unfortunately these are annoying arguments that get conservatives in a lot of trouble with smart commentators on the other side, and then tend to discredit their entire enterprise. Paul Krugman has made a cottage industry out of sniping these crude arguments from otherwise distinguished economists (see Robert Barro via flexible-price models).

However, while Googling Mr. Wesbury, I came across an article that I want to dredge up from February 2008. I want to do this not to point out that Wesbury has no credibility (like some commentators *ahem*), but to show how thinking in terms of interest rates screws people up, and how uncertainty is very dangerous to reputations. The title of the article is “Brian Wesbury Sees No Recession Ahead“.

Q: You say we are not in a recession and we are not even headed for one, right?

A (Wesbury): That is correct. Every single recession in the United States for the last 80 years has been preceded by a tight Federal Reserve policy — in other words, excessively high interest rates. And we clearly don’t have that today. Recessions are also preceded frequently by tax hikes or protectionism. So I would say that today we have very low interest rates, we have low tax rates, and we are not moving in a protectionist direction. As a result, those conditions that have led to recessions in the past don’t exist. One last point: I know of no point in history where we have ever scared ourselves into a recession. It just has never happened before and I don’t think it will happen this time, either.

This is a bombshell of a quote. My main point is that given the events that had happened up until then, saying that we won’t experience a terrible-horrible recession was not an unreasonable position to take. The problem is equating the setting of interest rates with the stance of monetary policy. I also know of no correlation between taxes and recession, and I’m sure he had in mind Smoot-Hawley when he was talking about protectionism…but that tariff was a drop in the bucket of what the actual problem was (then and today): falling NGDP.

By late 2008, in hindsight, Wesbury looks like a fool…but how would he have possibly known that the Fed would let NGDP fall at the fastest rate since 1938 later in the year? As a counterfactual, had the Fed kept up expectations that it would hit its 5% NGDP growth target, Wesbury’s statement wouldn’t look so bad today.

Arthur Laffer was (YouTube) famously in the same boat while talking with Peter Schiff, and of course made to look like a moron. My first piece of advice would be to not attempt to make public predictions. Since that is impossible, my second piece of advice would be to err on the side of caution when making predictions based on models (that is also true with NK multiplier models)…especially when facing strong headwinds.

P.S: I’m happy about the “Babble” tag.

There has been a lot of chatter around the blogosphere about Narayana Kocherlakota’s speech in Michigan last week, and seeing as I am trying to catch up on news, I think that is a good a place as any to start. First, here is the whole speech, so that you can read it if you would like.

The big focus, especially among left-leaning commentators, has of course been Kocherlakota’s comments on the unemployment situation. The only troubling thing to me about a monetary policymaking body discussing unemployment is the fact that it is happening at all. I don’t believe that there is anything “special” that monetary policy can do to alleviate unemployment — even in a booming economy. The capacity of monetary policy to act is to keep nominal GDP growing at a constant rate, year over year, and to tighten a little when it overshoots and loosen a little when it undershoots — such that the trend path of NGDP is a constant upward slope. I’m not an expert on the welfare-maximizing trend rate of NGDP…but people who are much smarter than me on average advocate 5% NGDP growth.

In any case, in the speech, Kocherlakota breaks down how Fed meetings operate, and then breaks down his “forecast speech” that he gave to the FOMC. Along those lines, he has three points: GDP (real), inflation, and unemployment. On those three points, he has this to say:

Typically, real GDP per person grows between 1.5 and 2 percent per year. If the economy had actually grown at that rate over the past two and a half years, we would have between 7 and 8.2 percent more output per person than we do right now. My forecast is such that we will not make up that 7-8.2 percent lost output anytime soon.

[…]

The Fed’s price stability mandate is generally interpreted as maintaining an inflation rate of 2 percent, and 1 percent inflation is often considered to be too low relative to this stricture. I expect it to remain at about this level during the rest of this year. However, our Minneapolis forecasting model predicts that it will rise back into the more desirable 1.5-2 percent range in 2011.[1]

[…]

Monetary stimulus has provided conditions so that manufacturing plants want to hire new workers. But the Fed does not have a means to transform construction workers into manufacturing workers. […] Given the structural problems in the labor market, I do not expect unemployment to decline rapidly. My own prediction is that unemployment will remain above 8 percent into 2012.

[1]5yr TIPS spread is at 1.43, 10yr @ 1.55.

Now, not making up the lost employment is partially a function of his previous point about per capita GDP remaining under trend for an extended period of time. This is the cyclical component of unemployment. Cyclical unemployment is created due to the relationship of the economy to the cycle of time. As such, the level of cyclical unemployment correlates well with the business cycle, seasonal factors, etc. I believe that most of the unemployment we are currently experiencing is of cyclical nature.

I think the error in Kocherlakota’s thinking stems from this quote:

Monetary stimulus has provided conditions so that manufacturing plants want to hire new workers. But the Fed does not have a means to transform construction workers into manufacturing workers.

This is wildly baffling. Not only does Kocherlakota make the forecast above — i.e. we will not be hitting any of our targets (nominal or otherwise) any time soon — he also states that he believes that money has been easy. That implies that monetary policy has zero effect on the economy, any time. He also identifies that low rates for an extended period of time are a sign of monetary failure, but does so in a future-orientation. While it is true that low rates can (and do) accompany* a deflationary “trap”, the policy prescription that follows is not to raise short-term rates regardless of the composition of employment. The proper policy response in that situation is to set a positive nominal target, level targeting and commit to move heaven and earth to hit that target.

That, rather than his statements about unemployment, is what I view as Kocherlakota’s underlying problem.

*H/T to Andy Harless in the comments. Also, read his post about Kocherlakota’s statements.

In a blog post today, Paul Krugman outlines a hypothetical situation that we could find ourselves in:

And this raises the specter what I think of as the price stability trap: suppose that it’s early 2012, the US unemployment rate is around 10 percent, and core inflation is running at 0.3 percent. The Fed should be moving heaven and earth to do something about the economy — but what you see instead is many people at the Fed, especially at the regional banks, saying “Look, we don’t have actual deflation, or anyway not much, so we’re achieving price stability. What’s the problem?”

I wonder if, on a particularly lazy day when Paul Krugman finds it difficult walk upstairs, he claims that he is in the “main floor trap”? But I digress. There is only one culprit in this situation: the dual mandate.

I’m not an expert on the history of the dual mandate, but I would venture a guess that it was the result of a grand bargain in which “price stability” came from the “hawkish” right, and “unemployment” came from the “dovish” left. The nature of the Fed’s dual mandate is such that it allows the central bank to wiggle out of nearly any situation if finds itself in with little consequence. Since the Fed is aiming at two diametrically opposed targets at once (price stability and full employment), it has large discretion upon which it can draw to justify its policy actions.

Is unemployment 9.5% with core CPI inflation falling below 1% and future expected inflation well below target as well? Well, that’s price stability!

How about persistent inflation rates bordering on double-digits while employment booms? Pat yourselves on the back guys!

In reality, and much to the chagrin of leftists everywhere, the modern Fed (1980’s+) has mostly erred on the side of price stability, which in the recent context has meant 5% NGDP growth with a rough average of 3% real growth and 2% inflation. This has allowed for a NAIRU of around 4-5% for the United States as a whole. Of course, that is a rate…and as long as the unemployed are continually in flux — that is, as long as hires outpaces quits and fires — that rate isn’t much of a problem. What is a problem is that the same dual mandate that was praised by some economists during the Great Moderation is now enabling the Fed to shirk its duties (and perhaps even worse, providing cover for “leveling down” with an implicit policy of opportunistic deflation…which is what Krugman implies above).

The Federal Reserve’s mandate is unique in the world. Most other central banks operate under a “hierarchical mandate” which generally stipulates an inflation target. It is hierarchical, because the central bank can set any target other targets it wants, and pursue them in order as long as they have hit their mandated target. The results of this kind of target vary from country to country.

In my opinion, Congress should scrap the Fed’s dual mandate, and instead mandate that the Federal Reserve set an explicit nominal target, and do everything in their power to hit that target (level targeting). If they’re feeling generous, they can give the Fed discretion as to which target they would like to set. If not, I would specify NGDP. I don’t think that the monetary policymaking body of the Federal Reserve should even look at a single unemployment number. They should focus like a laser on their keeping their nominal target in a very narrow range and leave the question of unemployment (which is a real variable) to other policymakers.

Stabilize monetary policy around a nominal aggregate, and I would wager that unemployment would find a way to work itself out with minimal intervention.

P.S. I kind of smile when I think about the Fed “moving heaven and earth to do something about the economy”. I suppose that is because 1) I think that monetary policy can do so and 2) I’m a huge nerd.