You are currently browsing the tag archive for the ‘Monetary policy’ tag.

I’m headed off to a conference, but I just wanted to voice my disgust with Ben Bernanke quickly. Here is what I gathered from his speech in Jackson Hole:

1. The Fed has the tools to offset shocks to money demand, but only sees fit to use them in the event that the country is facing actual deflation.

2. The Fed is highly committed to memory-less inflation targeting, and is happy living with inflation below 2%.

3. The Fed will not offset contractionary fiscal policy, handing proponents of active demand management victory on a silver platter, though they don’t deserve it.

We will have to wait until the next Fed meeting to see Bernanke’s “real” intentions on monetary policy. Will he steer the committee into a more aggressive stance? The stock market is very slightly up on the speech, so maybe WAll Street knows something that I don’t…but I just can’t see how an aggressive policy move is in the cards.

Here is a data point given by Glenn Rudebusch (h/t Mark Thoma), vice president of the San Francisco Fed, in the recent FedView:

A simple rule of thumb that summarizes the Fed’s policy response over the past two decades recommends lowering the federal funds rate by 1.4 percentage points if inflation falls by 1 percentage point and by 1.8 percentage points if the unemployment rate rises by 1 percentage point. Either headline inflation or core inflation can be used with this rule to construct policy recommendations. Relative to a core inflation formulation, a policy rule using headline inflation would have called for a higher fed funds rate in 2005-2006 before the recession and in 2008 in the midst of a deepening recession. Currently, both formulations call for substantial monetary accommodation.

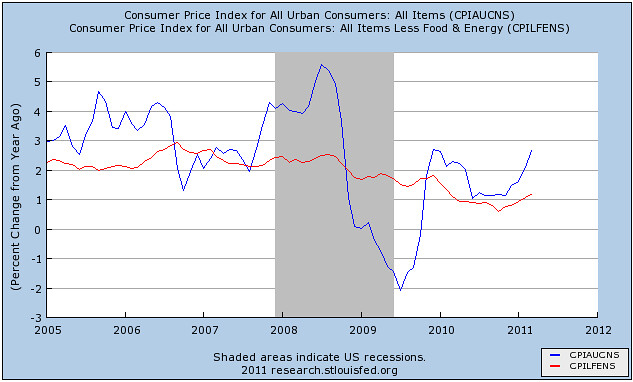

The Fed, in it’s October meeting (after Lehman had failed on Sept. 16th) lowered their target fed funds rate only 50 basis points to 1.50. That week (Dec. 6th-10th), the DJIA fell 18%, but it wasn’t until Oct. 29th that the Fed met hastily in an emergency meeting to cut rates…50 basis points, to 1.00. What metric could they have been watching that would suggest (in a historical sense) that inflation was the problem, and not deflation? It could only have been headline inflation!

[Click Image to Enlarge]

Core inflation has closely tracked a median ever since the Fed concerned itself with keeping inflation low (and stable). But what you really have to ask yourself is; what good is having a target when you are able to move between whatever measure suits your inclination at the moment? There is, of course, a mechanism by which inflation in energy prices (and thus broad inputs) can translate into a higher trend in core inflation (60’s-80’s), but this hasn’t been the case for thirty years.

The key here is that monetary policy should not be engaged in inflation targeting. Inflation is a symptom of an underlying problem (AD or AS shock), for which the Fed can only react to AD. If the Fed concerns itself with reacting to AS shocks, then we end up where we were in late 2008, with plummeting NGDP. The Fed should target the variable that it has control over, and keep it growing at a stable long-run rate.

Update: Accidentally hit the “Publish” button instead of preview. In any case, the SF Fed’s forecast is that the rise in commodity prices is unsustainable given the level of depressed aggregate demand in much of the world economy. Here is the chart:

The SF Fed also predicts a persistent (and rather large) output gap through 2012! That is a monumental failure of monetary policy.

Here’s a piece from David Leonhardt that has been getting some of play on blogs that I frequent. It’s definitely good to see that more of the profession are coming around to the “quasi-monetarist” view that monetary policy is not impotent at the zero bound, that it can do much more. Here’s David:

Whenever officials at the Federal Reserve confront a big decision, they have to weigh two competing risks. Are they doing too much to speed up economic growth and touching off inflation? Or are they doing too little and allowing unemployment to stay high?

It’s clear which way the Fed has erred recently. It has done too little. It stopped trying to bring down long-term interest rates early last year under the wishful assumption that a recovery had taken hold, only to be forced to reverse course by the end of year.

Given this recent history, you might think Fed officials would now be doing everything possible to ensure a solid recovery. But they’re not. Once again, many of them are worried that the Fed is doing too much. And once again, the odds are rising that it’s doing too little.

Indeed. Myself and others have been emphasizing that the passivity of the Federal Reserve in late 2008 (or, as I like to tell it, the Fed being hoodwinked by rising input costs) was indeed an abdication of its duties…but what duties are those? It’s unclear, because the nature of the Fed’s mandate allows it to slip between two opposing targets at will. Michael Belognia, of the University of Mississippi (and former Fed economist) makes a similar point in this excellent EconTalk podcast. The big issue, as I see it, is the structure of the Fed’s mandate. Kevin Drum (presumably) has a different issue in mind:

Hmmm. A big, powerful, influential group that obsesses over unemployment. Sounds like a great idea. But I wonder what kind of group that could possibly be? Some kind of organization of workers, I suppose. Too bad there’s nothing like that around.

I think this idea of “countervailing powers” needed to influence the Fed is wrong-headed. There is no clear-cut side to be on. Unions may err on the side of easy money…but then again, Wall Street likes easy money* too, when the Fed artificially holds short term rates low. It’s all very confusing. But that’s arguably great for the Fed, because confusion is wiggle room…however it’s bad for the macroeconomy, because confusion basically eliminates the communications channel, stunting the Fed’s ability to shape expectations.

Now here’s the problem as I see it: NGDP is still running below trend, and expectations of inflation are currently running too low to return to the previous trend. Notice, I said nothing about the level of employment. Unemployment is certainly a problem, but the cause of (most of the rise in) unemployment is a lower trend level of NGDP.

Given that you agree with me about the problem, which is the better solution:

- Gather a group (ostensibly of economists) to press to rewrite the Fed charter such that the Fed is now bound by a specific nominal target, and its job is to keep the long run outlook from the economy from substantially deviating from that target using any means possible.

- Find an interest group with a large focus on unemployment to back the “doves” in order to pressure the Fed into acting more aggressively.

I would back number one over number two any day. And the reason is that while I’m in the “dove” camp now, that isn’t always the case. At some time, I’ll be back in the “hawk” camp, arguing against further monetary ease. Paul Krugman has recently made the same point about using fiscal policy as a stabilization tool. My goal is to return NGDP to its previous trend, and maybe make up for some of the lost ground with above trend growth for a couple years. That would solve perhaps most of the unemployment problem.

But say it doesn’t. Say we return to a slightly higher trend NGDP growth level for the next couple years, and due to some other (perhaps “structural”) issue(s), unemployment remains above the trend rate we enjoyed during the Great Moderation. Would it be correct to say that monetary policy is still not “doing enough”? I don’t think so. At that point, we should look toward other levers of policy that can help the workforce adjust to the direction of the economy in the future.

I’m not say that is even a remotely likely scenario, I’m just trying to illustrate the complexity and possible confusion (and bad policy) that could come out of a situation that Drum seems to be advocating. Better in my mind to have a rules-based policy than an interest group-pressure based policy.

P.S. This was the first post I’ve ever written using my new Motorola XOOM tablet. It wasn’t the hardest thing I’ve ever done, but it was by no means easy. And I wanted to add some charts, but that would be particularly annoying.

*Which, of course, is not necessarily easy money, just low interest rates.

He’s always taking hiatuses from blogging, and claiming to be “travelling”. Now I know that he has been leading a double life. From Romer’s interview with Ezra Klein:

EK:You’ve also criticized the Federal Reserve for not doing more. What would you like to see them doing?

CR:I’m teaching a course this semester on macro policy from the Depression to today. One thing I had the class read was Ben Bernanke’s 2002 paper on self-induced paralysis in Japan and all the things they should’ve been doing. My reaction to it was, ‘I wish Ben would read this again.’ It was a shame to do a round of quantitative easing and put a number on it. Why not just do it until it helped the economy? That’s how you get the real expectations effect. So I would’ve made the quantitative easing bigger. If you look at the Fed futures market, people are expecting them to raise interest rates sooner than I think the Fed is likely to raise them. So I think something is going wrong with their communications policy. They could say we’re not going to raise the rate until X date. Those would be two concrete things that wouldn’t be difficult for them to do. More radically, they could go to a price-level target, which would allow inflation to be higher than the target for a few years in order to compensate for the past few years, when it’s been lower than the target.

All kidding aside, this is policy advice gold. I can broadly agree with all that Romer is saying in the whole thing. I’m not gung-ho about using fiscal policy and expecting it to “work” in the sense that it raises NGDP to a level which is consistent with returning to trend quickly (especially with a conservative central bank), however I don’t see anything wrong with smoothing the edges of recession by helping people through the tough time using fiscal policy (mostly simple transfers), and of course reducing employment during a recession. As prescribed here (not by Mark Thoma, but by a paper circulated by John Boehner), is asinine.

P.S. I think that the level of suffering an economy would have to deal with as the result of sharp deficit reduction is directly related to the willingness of a central bank to accommodate the policy.

So that San Francisco Fed says that the natural rate of unemployment may have risen to nearly 7%.

Mounting evidence suggests that structural factors may have increased the “normal” rate of unemployment to about 6.7%. Much of this increase is likely to be temporary. In particular, the extension of unemployment benefits probably accounts for about half of the increase. But, even with a 6.7% natural rate, current and forecasted levels of unemployment imply that significant labor market slack will persist for several years.

Its important to remember that monetary policy itself can influence the natural rate.

When we look at the history of Eurosclerosis, the tendency of many European countries to have stubbornly high unemployment despite growing economies, we see that those nations most aggressive in bringing down inflation had the worse cases of sclerosis. More importantly, countries which reversed tight money policies in the face of severe unemployment saw the natural rate of unemployment fall.

Laurence Ball does a nice review.

Another way of saying all of this: Recession are caused by money, either a change in the demand for it or the supply of it. This is not to say fiscal policy plays no role but simply that unemployment rises sharply when people cannot build a cushion of savings as fast as they would like to. Broad based tax cuts for example, could allow people to build up their savings faster than they would otherwise.

However, once going, unemployment can beget unemployment as people who haven’t had a job in a while are less employable. One of the things we notice even from recessions of old is that unemployment rises faster than it falls.

This suggests that getting a job is not simply the inverse of losing one. The labor force is changed by mass layoffs. That change has to be undone.

What does all of that mean?

It means that we shouldn’t be inclined to “settle” for an unemployment rate of 7% or see that as the new target. Sustained aggressive monetary policy will bring the natural rate down over time. We should be aiming to “shoot past” 7%, knowing that the new target will be lower than 7% by the time we get there.

As a side note, I am unsure how to approach the hard money folks, who at the moment I see as the greatest immediate impediment to the health of the nation. On the one hand we can make the very true case that inflation is nothing to be worried about now. The Fed can continue to press forward without fear of rising much above its presumed target of a 2% core rate, anytime soon.

My fear is that this doesn’t address the long run issue, that we may need to go above that comfort zone to undo some of the damage of this recession. That kind of talk gets a lot of people nervous and may even hurt efforts at current monetary expansion.

Yet, resorting to the “but inflation is low now” position almost concedes that any inflation rate higher than 2% is indeed undesirable. That is not what I mean at all.