You are currently browsing the tag archive for the ‘Federal Reserve’ tag.

The US, and world economy needs the Fed to act today, and markets seem to be indicating that they believe that the Fed will act. This is the same situation we found ourselves in during the fall of ’08. Growth is barely even anemic, and markets are indicating that they expect future NGDP growth to slow. Headline inflation has subsided, and the recent “major” blip in core inflation has turned out to to be a fluke — inflation is still running below the Fed’s implicit target. Combined with that, markets have roundly given the finger to S&P, and world troubles are pushing people into dollar assets, exacerbating the problems that we are experiencing with elevated money demand.

[Click Image to Enlarge]

The Fed needs to do something bold today, before we fall off the cliff again, just like in October/November 2008…we’ve seen when happens when passively tight monetary policy causes the economy to limp along…once the buildup of balance sheet problems, falling asset prices, and increased demand for money reaches a head, the tipping point comes quickly and painfully. However, this time we’ll likely experience actual deflation, which will likely become a deflationary trend due to the timidity of our central bank.

So Bernanke, please give the hawks the finger for now, and do the right thing. The future of the US economy desperately needs it.

Today, Barney Frank introduced legislation in committee to remove regional Fed presidents from the FOMC:

U.S. Rep. Barney Frank (D., Mass) Tuesday introduced a bill that would let interest rates be set only by Federal Reserve officials picked by the government, a new attempt to move power away from regional Fed officials chosen by the private sector.

The bill would remove from the 12-member policy-setting Federal Open Market Committee the five members who represent regional Fed banks. Only the seven-member board in Washington, which currently has two vacant seats, would get to vote on interest rates. The congressman said this would make the Fed more democratic and increase “transparency and accountability on the FOMC” by eliminating those officials who are effectively picked by business executives

Now, I have never been a fan of Barney Frank, but I do see merits in this legislation. However, first a contrary opinion, courtesy of Mark Thoma:

I can support – and have advocated — reforming the way in which regional bank presidents are selected. But this proposal, which removes geographical representation even though recessions do not hit each area of the country equally, is a bad idea (the Board of Governors can already veto the appointment of a regional bank president, though I don’t know of any instances where this power has been used). It takes us further away from the populist roots of the Fed’s structure, a structure that tried hard to represent all interests in policy. It also furthers the concentration of power in Washington that has been occurring slowly but surely ever since the Bank Reform Acts in the wake of the recession established the Fed’s current structure. In addition, it takes another step toward increasing the power of Congress over day to day monetary policy…I hate to even imagine how bad things would be if Congress had been in charge of monetary policy.

…reform the selection process for regional bank presidents, but don’t increase the concentration of power in Washington…I would like to see, at a minimum, less representation of business so that the public interest generally can take center stage.

While I can stand broadly stand behind the anti-concentration of power sentiment, if you have regions of a country which fluctuate so wildly from baseline that their performance creates a necessity for special accommodation from monetary policy in general, that is an OCA argument against having a single currency area. David Beckworth has argued that the “rust belt” in the US could have possibly benefited from its own currency over the last decade, and I agree!

Do we need regional Fed presidents at the table? After all, in the Great Contraction of 2008, and the ensuing recession, it has been the regional presidents that have provided the voice of hawkishness, even through tumultuous 2009! So when the chips are down, and adequate monetary policymaking is at its highest stakes, these guys were wrong…and being that they largely represent banking interests, they are likely biased against inflation at all costs. This certainly hasn’t been any help to our recovery!

Thoma is worried about Congressional power eroding sound monetary policy decision-making…but our current Fed structure doesn’t prevent that, indeed, it probably enhances it!* After all, Bernanke held the first press conference amid rising populist fears stoking an encroaching Congress’ ire regarding monetary policy. When Mark hopes that public interest would take center stage — and I do as well — but I don’t see how reforming the Fed presidents’ selection process is superior to having a board that is wholly selected by the President, and approved by Congress. If you want to do 12 members that way, so be it!

However, while Barney Frank’s motivation is mostly suspect, sometimes even then you stumble upon a good idea…but this idea isn’t good enough. If you are in a position where your legislation has little chance of making it out of committee, my play would be to lay all of my cards on the table: rewrite the Fed charter such that it requires the Fed to set one nominal target, and keep it on a level growth path. I would prefer NGDP, as I believe that targeting nominal spending is far superior to targeting inflation. This is obviously not Frank’s goal, and it would likely go against Franks (poor) instincts as it removes the unemployment portion of the mandate…but the level of employment in an economy is a real variable.

So what if trend NGDP was perfectly on target, but unemployment remained uncomfortably high. Is that a reason for monetary policy to act? Well, it could be…but there are other questions to ask of other policymakers. What are the structural problems? If there are supply side rigidities, look at removing them (not just removing specific laws, but increasing education, etc.). If you are uncomfortable with removing them, then live with higher joblessness. If there happened to have been an extremely productivity-enhancing technological development (like mass teleportation?) that is causing persistent unemployment because it significantly increases the return on capital investment vs labor investment, then perhaps the long-run growth potential of the economy has been increased — if that is the case, monetary policy may need to target a higher growth path for NGDP.

So, to sum it up, I think removing regional Presidents does make the board more accountable, and it would probably also improve the decision-making process. And if you really wanted to reform the Fed with an eye toward independence, remove the dual mandate and institute a explicit nominal target.

*Imagine a Congressional hearing under an NGDP targeting rule. What would it consist of?

Congressman: “Is NGDP on target”?

Fed Chair: “Yeop”.

Congressman: “Lets get lunch”.

That is obviously a joke, but it is the wiggle room created by the confusing dual mandate that allows Congress to leverage nearly all of its power against the bank.

“A slow sort of country!” said the Queen. “Now, here, you see, it takes all the running you can do, to keep in the same place. If you want to get somewhere else, you must run at least twice as fast as that!” -Lewis Carroll, Through the Looking Glass

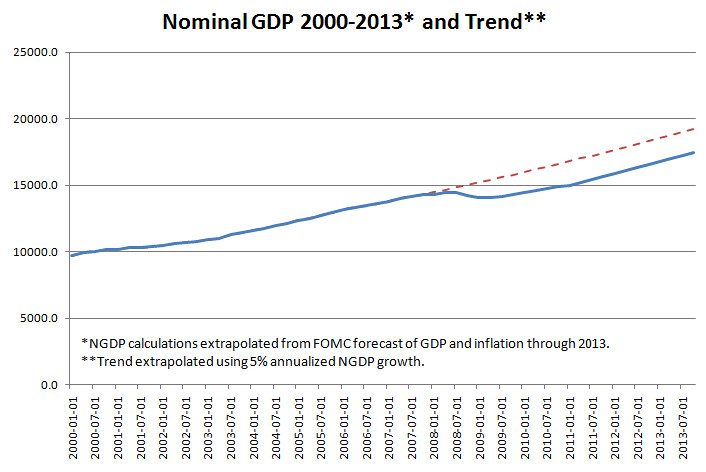

I have constructed a chart extrapolating the trend growth in nominal GDP* through 2013, along with the FOMC’s forecast of nominal growth through 2013.** Have a look:

[Click Image to Enlarge]

As you can see, by the Fed’s own forecast, we will remain under trend growth in NGDP through 2013. Indeed, by the fourth quarter, we will be 10.2% below the trend. That is roughly $1.7 trillion in potential output! I regard this as the “one chart to rule them all”, and it is what I point to when people ask me why we are experiencing a sluggish “jobless” recovery.

Always keep in mind, though, prediction is a fools errand over anything but the shortest of time spans. The key here is that there is only one way the prediction can be off such that it would benefit the economy. Those aren’t good odds to take.

*FRED

**Average of the central tendency.

I, for the life of me, can not understand where Stephen Williamson is coming from in the recent posts he’s done claiming that Quantitative Easing is ineffective, and that the Fed is completely out of tools which it can use to boost the economy. Here are the points he made from his most recent post, entitled “Mark, Brad, and Ben“:

- Accommodative monetary policy causes inflation, but with a lag. I think Brad’s inflation forecast is on the low side, as maybe Ben does as well. The policy rate has been at essentially zero since fall 2008. Sooner or later (and maybe Ben is thinking sooner) we’re going to see the higher inflation in core measures.

- Maybe Ben is more worried about headline inflation (as I think he should be) than he lets on.

- Maybe in his press conference Ben did not want to spend his time explaining why the Fed spends its time focusing on core inflation. What every consumer sees is headline inflation, and they are much more aware of the food and energy component than the rest of it.

- As with my comments on Thoma, there is really no current action that the Fed can take to increase the inflation rate. More quantitative easing won’t do anything, so the Fed is stuck with saying things about extended periods with zero nominal interest rates in order to have some influence through anticipated future inflation on inflation today.

Most of the list simply baffles me. First of all, accommodative monetary policy can cause inflation. And of course in the long run, a stable monetary policy only affects prices…but the blanket statement that monetary policy causes inflation is misleading, and highlights a problem with even talking about inflation. In a standard AS/AD model, the determinant of the composition of NGDP growth is the slope of the SRAS curve. In recessions, it is generally understood that the SRAS curve is relatively flat. In that case (arguably the case we are dealing with right now), an accommodative monetary policy which shifts the AD curve to the right would result in much higher output growth than inflation. As for the lag part, monetary policy has an almost immediate (< one quarter) impact on many markets; including interest rates, stock/commodity prices, inflation expectations, etc. Here is a chart of those market reactions to both QE's courtesy of Marcus Nunes:

[Click Image to Enlarge]

In each case, you can see that asset prices had a quite immediate response to quantitative easing. QE2 performing poorly doesn’t indicate that QE doesn’t work, it highlights problems with how the policy was implemented. Specifically, the Fed structured the policy around purchasing a specific quantity of Treasuries ($600bn) instead of setting a target level of nominal spending, or even a price level target, and then commit to purchases until that target has been reached.

Second, why would Ben Bernanke be worried about headline inflation when nearly every forecast from the Federal Reserve views the current rise in headline as temporary? Here is the SF Fed, which I posted earlier:

[Click Image to Enlarge]

Indeed, the FOMC’s own report states as much. Furthermore, we have a good idea of what is causing the bump in headline inflation, and that is the energy prices. We also have good reason to believe that this is due to rising demand in the briskly growing emerging markets, and the inability to ramp up supply. What in the world is monetary policy supposed to do about that? Is Williamson advocating tightening policy while NGDP is still FAR below trend, and we are not experiencing enough growth to catch up to the previous trend?

I don’t have many quibbles with the third point, but the fourth point is the one that floored me the most. I’ll outsource commentary to David Beckworth in a comment on Williamson’s post:

Steve,

Why do you keep saying there is nothing the Fed can do? You acknowledged in the comment section in your last post that the Fed could do something more via a price level or ngdp level target. By more forcefully shaping nominal expectations with such a rule the Fed could do a lot.

It is worth remembering that folks were saying the same thing about monetary policy in the early 1930s. They were certain there was nothing more the Fed could do and as a consequence of this consensus we get tight monetary policy and the Great Depression. Then FDR came along and change expectations by devaluing the gold content of the dollar and by not sterilizing gold inflows. His “unconventional” monetary policy packed quite a punch.

And here is my comment:

I’m with David on NGDP targeting. But even if the Fed didn’t do that, it has its interest on reserves policy, and the last I checked, it hasn’t set an explicit inflation level target, and there is ~$14 trillion in outstanding Treasury debt held by the public that the Fed does not yet own…something Andy Harless has pointed out on numerous occasions.

Here’s a piece from David Leonhardt that has been getting some of play on blogs that I frequent. It’s definitely good to see that more of the profession are coming around to the “quasi-monetarist” view that monetary policy is not impotent at the zero bound, that it can do much more. Here’s David:

Whenever officials at the Federal Reserve confront a big decision, they have to weigh two competing risks. Are they doing too much to speed up economic growth and touching off inflation? Or are they doing too little and allowing unemployment to stay high?

It’s clear which way the Fed has erred recently. It has done too little. It stopped trying to bring down long-term interest rates early last year under the wishful assumption that a recovery had taken hold, only to be forced to reverse course by the end of year.

Given this recent history, you might think Fed officials would now be doing everything possible to ensure a solid recovery. But they’re not. Once again, many of them are worried that the Fed is doing too much. And once again, the odds are rising that it’s doing too little.

Indeed. Myself and others have been emphasizing that the passivity of the Federal Reserve in late 2008 (or, as I like to tell it, the Fed being hoodwinked by rising input costs) was indeed an abdication of its duties…but what duties are those? It’s unclear, because the nature of the Fed’s mandate allows it to slip between two opposing targets at will. Michael Belognia, of the University of Mississippi (and former Fed economist) makes a similar point in this excellent EconTalk podcast. The big issue, as I see it, is the structure of the Fed’s mandate. Kevin Drum (presumably) has a different issue in mind:

Hmmm. A big, powerful, influential group that obsesses over unemployment. Sounds like a great idea. But I wonder what kind of group that could possibly be? Some kind of organization of workers, I suppose. Too bad there’s nothing like that around.

I think this idea of “countervailing powers” needed to influence the Fed is wrong-headed. There is no clear-cut side to be on. Unions may err on the side of easy money…but then again, Wall Street likes easy money* too, when the Fed artificially holds short term rates low. It’s all very confusing. But that’s arguably great for the Fed, because confusion is wiggle room…however it’s bad for the macroeconomy, because confusion basically eliminates the communications channel, stunting the Fed’s ability to shape expectations.

Now here’s the problem as I see it: NGDP is still running below trend, and expectations of inflation are currently running too low to return to the previous trend. Notice, I said nothing about the level of employment. Unemployment is certainly a problem, but the cause of (most of the rise in) unemployment is a lower trend level of NGDP.

Given that you agree with me about the problem, which is the better solution:

- Gather a group (ostensibly of economists) to press to rewrite the Fed charter such that the Fed is now bound by a specific nominal target, and its job is to keep the long run outlook from the economy from substantially deviating from that target using any means possible.

- Find an interest group with a large focus on unemployment to back the “doves” in order to pressure the Fed into acting more aggressively.

I would back number one over number two any day. And the reason is that while I’m in the “dove” camp now, that isn’t always the case. At some time, I’ll be back in the “hawk” camp, arguing against further monetary ease. Paul Krugman has recently made the same point about using fiscal policy as a stabilization tool. My goal is to return NGDP to its previous trend, and maybe make up for some of the lost ground with above trend growth for a couple years. That would solve perhaps most of the unemployment problem.

But say it doesn’t. Say we return to a slightly higher trend NGDP growth level for the next couple years, and due to some other (perhaps “structural”) issue(s), unemployment remains above the trend rate we enjoyed during the Great Moderation. Would it be correct to say that monetary policy is still not “doing enough”? I don’t think so. At that point, we should look toward other levers of policy that can help the workforce adjust to the direction of the economy in the future.

I’m not say that is even a remotely likely scenario, I’m just trying to illustrate the complexity and possible confusion (and bad policy) that could come out of a situation that Drum seems to be advocating. Better in my mind to have a rules-based policy than an interest group-pressure based policy.

P.S. This was the first post I’ve ever written using my new Motorola XOOM tablet. It wasn’t the hardest thing I’ve ever done, but it was by no means easy. And I wanted to add some charts, but that would be particularly annoying.

*Which, of course, is not necessarily easy money, just low interest rates.

In the comments to a post by Tyler Cowen, George Selgin describes the use and potential for free banking from a gradualist perspective:

The debate about whether the Fed has failed or not shouldn’t be confused with a debate about whether we should, were it possible to do so, want to flip a switch today that would shut the FOMC and discount window, leaving us with a frozen base, and then let private markets take charge from there.

Free banking isn’t what we’d have if we did that. Free banking is the sort of private market banking system that develops over time in the absence of special regulatory restrictions on banks. Our banking system hasn’t developed in that (I believe) healthy manner. It now has some features of free banking, like nationwide branching and market-based interest rates, that it was long denied. But in other respects, and especially that of being utterly dependent on explicit and implicit guarantees, it is less free than ever, and therefore less capable of standing on its own feet and of being able to reliably meet this country’s monetary needs without breaking down.

So I personally am too much a gradualist to want to flip that switch. I favor gradualist reforms that take account of the weakness of the present private banking system. Nevertheless, I think that free banking does offer a long-run ideal worth taking seriously in light of historical experience. And I also believe that continued attempts to reform our monetary and banking system without heeding the lessons of that experience, including attempts to shore up the system by expanding the Fed’s discretionary powers, while continuing to treat guarantees as a substitute for market discipline, are doomed to fail.

I’m not agreeing with Selgin’s argument, but many appeals against the Fed are wrapped in radical free market rhetoric, and it’s worth reading how one could cautiously support free banking and avoid calling for radical changes. One of my chief concerns is that even if free bankers are right and we can never count on the Fed for effective countercyclical monetary policy, if you remove the possibility for monetary policy it will not remove the demand for countercyclical policies. In a recession people will demand something be done, and this will leave only fiscal policy. However bad monetary policy is -if free banking critics are right- fiscal policy is worse.

In a Times article a few days ago is this interesting quote from Laurence Meyer, a former Fed governor:

It was this impending gridlock that might have pushed Mr. Bernanke to move, said Laurence H. Meyer, a former Fed governor. “Bernanke has said that fiscal stimulus, accommodated by the Fed, is the single most powerful action the government can take for lowering the unemployment rate, when short-term rates are already at zero,” Mr. Meyer said. “He has nearly pleaded with Congress for fiscal stimulus, but he can’t count on it.”

I’m taking this as a explicit, and unshrouded nod to the concept of “money financed fiscal policy”. Or, what is lovingly referred to in the press as “monetizing debt”. This is a situation where the government draws up a plan to distribute money, whether through direct transfers or increases in government consumption/investment, has the Treasury issue debt in the amount decided upon Congressionally, which the Fed then purchases with newly-coined money (and for hysterics, this money is created “out of thin air”!).

As Karl has noted, and as concurred upon by commenter Jazzbumpa, a program such as this would inevitably “work”. And by work, I mean it would raise inflation expectations such that businesses would be induced out of cash and into consumption and capital goods. This, of course, is something that the ARRA failed to do. This is true, but it is optimal policy?

I say no. I don’t think that fiscal policy need ever enter the picture. I think that the Federal Reserve should announce an explicit target to get the growth path of nominal expenditure to the previous level from the Great Moderation, and then continue to level target a stable growth path from there. In doing so, the Fed should immediately stop sterilizing its own open market operations by paying interest on excess reserves (indeed, the interest in reserves should be slightly negative, reflecting real rates). The Fed could then move down the yield curve, and buy Treasury debt that currently resides on the balance sheets of banks, businesses, and individuals; moving the price up while moving the yield down to zero. I suspect that there is enough debt out there that it would not run out of things to buy before hitting its nominal target. However, if it does, then it can move on to other assets.

The key thing here is that there are many interest rates in the economy, and not all of them are pegged at zero. My point is that far from needing to bring fiscal policy into the picture, monetary policy could go it alone. If the SRAS curve is relatively flat, which is a prediction of macro models, then the resultant inflation expectations would produce much more real output than inflation (lets ballpark and say 5% real growth, 2% inflation), up until full employment is reached — at which point, the Fed would revert to its normal level target. I do not think that Bernanke is “pleading with Congress” for fiscal policy. Why would he? If he identifies that aggregate demand is low relative to the Fed’s own target, then by all means, he should be taking steps to move aggregate demand to where the Fed is most likely to hit their target goals.

To those who say that it is unrealistic that the Fed would do this, is it any more unrealistic than hoping for money-financed fiscal policy?