You are currently browsing the tag archive for the ‘Inflation’ tag.

I, for the life of me, can not understand where Stephen Williamson is coming from in the recent posts he’s done claiming that Quantitative Easing is ineffective, and that the Fed is completely out of tools which it can use to boost the economy. Here are the points he made from his most recent post, entitled “Mark, Brad, and Ben“:

- Accommodative monetary policy causes inflation, but with a lag. I think Brad’s inflation forecast is on the low side, as maybe Ben does as well. The policy rate has been at essentially zero since fall 2008. Sooner or later (and maybe Ben is thinking sooner) we’re going to see the higher inflation in core measures.

- Maybe Ben is more worried about headline inflation (as I think he should be) than he lets on.

- Maybe in his press conference Ben did not want to spend his time explaining why the Fed spends its time focusing on core inflation. What every consumer sees is headline inflation, and they are much more aware of the food and energy component than the rest of it.

- As with my comments on Thoma, there is really no current action that the Fed can take to increase the inflation rate. More quantitative easing won’t do anything, so the Fed is stuck with saying things about extended periods with zero nominal interest rates in order to have some influence through anticipated future inflation on inflation today.

Most of the list simply baffles me. First of all, accommodative monetary policy can cause inflation. And of course in the long run, a stable monetary policy only affects prices…but the blanket statement that monetary policy causes inflation is misleading, and highlights a problem with even talking about inflation. In a standard AS/AD model, the determinant of the composition of NGDP growth is the slope of the SRAS curve. In recessions, it is generally understood that the SRAS curve is relatively flat. In that case (arguably the case we are dealing with right now), an accommodative monetary policy which shifts the AD curve to the right would result in much higher output growth than inflation. As for the lag part, monetary policy has an almost immediate (< one quarter) impact on many markets; including interest rates, stock/commodity prices, inflation expectations, etc. Here is a chart of those market reactions to both QE's courtesy of Marcus Nunes:

[Click Image to Enlarge]

In each case, you can see that asset prices had a quite immediate response to quantitative easing. QE2 performing poorly doesn’t indicate that QE doesn’t work, it highlights problems with how the policy was implemented. Specifically, the Fed structured the policy around purchasing a specific quantity of Treasuries ($600bn) instead of setting a target level of nominal spending, or even a price level target, and then commit to purchases until that target has been reached.

Second, why would Ben Bernanke be worried about headline inflation when nearly every forecast from the Federal Reserve views the current rise in headline as temporary? Here is the SF Fed, which I posted earlier:

[Click Image to Enlarge]

Indeed, the FOMC’s own report states as much. Furthermore, we have a good idea of what is causing the bump in headline inflation, and that is the energy prices. We also have good reason to believe that this is due to rising demand in the briskly growing emerging markets, and the inability to ramp up supply. What in the world is monetary policy supposed to do about that? Is Williamson advocating tightening policy while NGDP is still FAR below trend, and we are not experiencing enough growth to catch up to the previous trend?

I don’t have many quibbles with the third point, but the fourth point is the one that floored me the most. I’ll outsource commentary to David Beckworth in a comment on Williamson’s post:

Steve,

Why do you keep saying there is nothing the Fed can do? You acknowledged in the comment section in your last post that the Fed could do something more via a price level or ngdp level target. By more forcefully shaping nominal expectations with such a rule the Fed could do a lot.

It is worth remembering that folks were saying the same thing about monetary policy in the early 1930s. They were certain there was nothing more the Fed could do and as a consequence of this consensus we get tight monetary policy and the Great Depression. Then FDR came along and change expectations by devaluing the gold content of the dollar and by not sterilizing gold inflows. His “unconventional” monetary policy packed quite a punch.

And here is my comment:

I’m with David on NGDP targeting. But even if the Fed didn’t do that, it has its interest on reserves policy, and the last I checked, it hasn’t set an explicit inflation level target, and there is ~$14 trillion in outstanding Treasury debt held by the public that the Fed does not yet own…something Andy Harless has pointed out on numerous occasions.

Here is a word cloud of words used by Bernanke during the press conference which was held today:

[Click Image to Enlarge]

As you notice, inflation was mentioned quite a bit, which, really, is something that you should expect from a QA with a monetary policymaker. Many are lamenting the fact that unemployment took a back seat, and Reuter’s itself challenges us to find the word “jobs” in the word cloud. Personally, I enjoyed the fact that Bernanke basically said jobs are someone else’s policy purview — which I view as the right response. However, the fact remains that monetary policy is not on target, and that is a problem for Bernanke. A bigger problem may be that 2% inflation isn’t a target at all! Could the US be following Japan’s lead into self-induced paralysis?

In any case, here is the question (and rest of the e-mail, references removed) that I sent to be asked, which did not get asked:

First, thank you for sending me your e-mail address. I’m tepidly excited about Bernanke’s press conference tomorrow…but I have a lot of reservations. You could probably call me old-fashioned, but I’m always leery of public policy “rock stars”, like the “Committee to Save the World”, and Ben Bernanke being “Man of the Year”. In any case, I think there is going to be a strong focus on grilling Bernanke on employment levels (I see that David Leonhardt wrote a column urging that to be so). I view this as very counter-productive.

But I did tweet you my question, which was this:

“As recently as 2003, Bernanke [You] championed price level targeting as a remedy for the ‘liquidty trap’. Many other economists also endorse this idea. Given the failure of monetary policy in preventing a sharp fall in GDP in Oct 2008 w/ inflation targeting, what are your thoughts on NGDP lvl targeting? Implementation challenges? Benefits or costs that you see?”

I wanted to provide some background for this question, because it can seem like it is kind of out of left-field, given a “mainstream” interpretation of events. As you may know, many prominent economists (Krugman, DeLong, Blanchard) have publicly advocated an explicit inflation of greater than 2%. A subset of this work was done by Lars Svensson[1] and Ben Bernanke himself[2], only instead of using inflation targeting, both economists have advocated setting an explict price level target in order to escape the “liquidity trap”. Another strain of this work that has been popularized recently by Scott Sumner, David Beckworth, Marcus Nunes, Josh Hendricksen, and myself, (among others!) involves monetary policy targeting nominal cash expenditures in the economy, or NGDP. More “academically”, Robert Hetzel[3] and Michael Belognia[4] have advocated that cash grow at a steady pace.

A common theme among those who push the “NGDP level targeting” view and others is that we tend to believe that causality in this recession runs (roughly) this course: mild supply shock (subprime) > tight money (Jun – Nov 2008) > large crash (Oct 2008) > inadequate Fed accommodation (2009/2010) > sluggish and “jobless” recovery. Indeed, even Christina Romer seems to be on board with something like this interpretation[5]. In my opinion, the Fed should target like a laser on the long-run growth path of NGDP, and keep it growing on a stable path (5% was the trend of the Great Moderation, but some economists advocate a transition to 3% nominal growth), making up for slack and overshooting when it happens by loosening or tightening money (respectively) such that the market forecast and the Fed’s forecast are basically one-in-the-same. This leaves little room for paying much attention to the level or rate of employment in the economy. The only time that should concern the Fed is if there is a large enough structural change that they should revise their NGDP target based on a sustainable increase (or decrease) in productivity (be it labor, capital, or TFP).

As an aside, David Beckworth has urged the Fed to target the cause of macroeconomic instability, and not symptoms of it[6]. Unemployment is one symptom, as is inflation/disinflation/deflation. From this perspective, NGDP level targeting is far superior to price level (and inflation) targeting.

I hope that gave you a brief (but adequate) overview to acquaint yourself with the NGDP level targeting position if you were unfamiliar, so you’re not shooting in the dark. I know you probably won’t get to the references. As a tactical request, if you see it fit to use my question, I’d work hard to get an answer out of Bernanke regarding NGDP targeting rather than price level targeting. The reason I bring this up is that if you mention “price level targeting” in the question, while you make the question more likely to get answered (price level targeting is more mainstream), you also give Bernanke an out in that he can simply muse about price level targeting and avoid the NGDP targeting question altogether, even though they’re different concepts. It’s a tricky pole to balance.

Thanks for allowing me to participate!

Niklas Blanchard

http://www.modeledbehavior.com[1] http://papers.ssrn.com/

[2] http://www.federalreserve.gov/ and http://people.su.se/

[3] http://www.richmondfed.org

[4] http://mpra.ub.uni-muenchen.de/

[5] http://emlab.berkeley.edu/

[6] http://macromarketmusings.blogspot.com/ and http://macromarketmusings.blogspot.com/

Sadly, there were no intrepid reporters in the audience venturing these grounds.

[h/t Paul Krugman]

Here is a data point given by Glenn Rudebusch (h/t Mark Thoma), vice president of the San Francisco Fed, in the recent FedView:

A simple rule of thumb that summarizes the Fed’s policy response over the past two decades recommends lowering the federal funds rate by 1.4 percentage points if inflation falls by 1 percentage point and by 1.8 percentage points if the unemployment rate rises by 1 percentage point. Either headline inflation or core inflation can be used with this rule to construct policy recommendations. Relative to a core inflation formulation, a policy rule using headline inflation would have called for a higher fed funds rate in 2005-2006 before the recession and in 2008 in the midst of a deepening recession. Currently, both formulations call for substantial monetary accommodation.

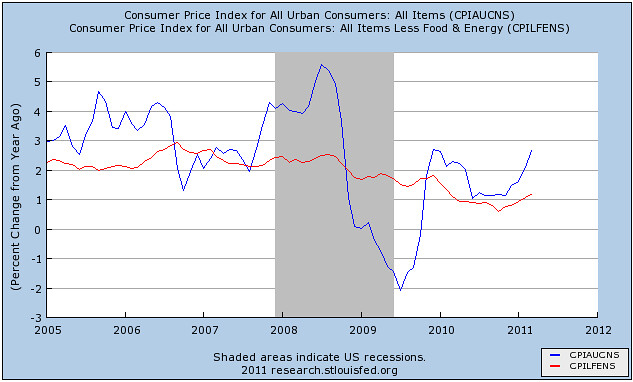

The Fed, in it’s October meeting (after Lehman had failed on Sept. 16th) lowered their target fed funds rate only 50 basis points to 1.50. That week (Dec. 6th-10th), the DJIA fell 18%, but it wasn’t until Oct. 29th that the Fed met hastily in an emergency meeting to cut rates…50 basis points, to 1.00. What metric could they have been watching that would suggest (in a historical sense) that inflation was the problem, and not deflation? It could only have been headline inflation!

[Click Image to Enlarge]

Core inflation has closely tracked a median ever since the Fed concerned itself with keeping inflation low (and stable). But what you really have to ask yourself is; what good is having a target when you are able to move between whatever measure suits your inclination at the moment? There is, of course, a mechanism by which inflation in energy prices (and thus broad inputs) can translate into a higher trend in core inflation (60’s-80’s), but this hasn’t been the case for thirty years.

The key here is that monetary policy should not be engaged in inflation targeting. Inflation is a symptom of an underlying problem (AD or AS shock), for which the Fed can only react to AD. If the Fed concerns itself with reacting to AS shocks, then we end up where we were in late 2008, with plummeting NGDP. The Fed should target the variable that it has control over, and keep it growing at a stable long-run rate.

Update: Accidentally hit the “Publish” button instead of preview. In any case, the SF Fed’s forecast is that the rise in commodity prices is unsustainable given the level of depressed aggregate demand in much of the world economy. Here is the chart:

The SF Fed also predicts a persistent (and rather large) output gap through 2012! That is a monumental failure of monetary policy.

In his Kentucky Day with the Commissioner (?) presentation today, James Bullard makes the case for targeting headline inflation. This is likely consistent with the recent hawkish turn he has taken, but is it correct? Is it true that we should expect core inflation to be a predictor of headline inflation, as he suggests?

First things first, though. Bullard proclaims victory for the quasi-monetarists:

This experience [rising asset prices in multiple markets, including stocks, bonds, commodities, as well as declining real interest rates and a depreciated dollar] shows that monetary policy can be eased aggressively even when the policy rate is near zero.

But then Bullard takes a turn toward hawkish land, with five points regarding core vs. headline inflation:

- Headline inflation refers to overall price indexes.

- Core inflation refers to the same indexes, but without the food and energy components.

- Core inflation is often smoother than headline inflation.

- Core eliminates 20% or so of the prices in the index.

- The “core” concept has little theoretical backing. It is very arbitrary.

Here is my problem: Our measures of inflation are both dubious at best, and a lagging indicator. The focus on headline inflation in the run-up to the crash of 2008 is the reason why monetary policy failed. Nowhere in the talk did Bullard mention unemployment, which I view as a good thing. However, he could have mentioned that a wage-price spiral requires that wages spiral, as well. That doesn’t seem to be happening:

[Click Image to Enlarge (h/t Paul Krugman)]

I didn’t hear the lecture, but from reading the notes, I’m quite confused. Does Bullard believe that the current spike in headline inflation is a trend, and why? Furthermore, should the Fed be targeting where inflation has been, or the forecast of future inflation, which is within a reasonable range as of right now.

[Click Image to Enlarge]

It all seems to me to strengthen the case for NGDP level targeting. Then we wouldn’t be having these silly debates. All you have to ask is: “Is NGDP growing on target?”

[Click Image to Enlarge]

Not quite yet. And furthermore, I would argue that we need a period of above-trend growth in NGDP in order to get capacity utilization level to their previous trend as quickly as possible. There may be merit to shifting to a lower trend rate of NGDP growth, but not at a moment when capacity utilization is low, and unemployment is high. In short, I see no threat of the current headline inflation pressures translating into accelerating inflation. The Fed should continue to be accommodative until at least the point that we reach the previous trend level of NGDP.

P.S. Sorry for the incredibly bad charts. For some reason, Excel is force closing on my computer now, and I had to switch to using Openoffice.org. I am less than impressed, to say the least.

Jim Hamilton has a nice breakdown on all the positive signs for US growth. I even have a new presentation I am giving titled “Don’t Be Lulled into Fall Sense of Despair” that basically argues that if things go as planned the US economy will be growing steadily and so will profits and tax revenues.

All that having been said my worry is that this will cause the Fed to back off of its aggressive stimulus policy. The Fed should stay the course with QE2 and consider QE3.

As I have mentioned before, we are conditioned to think of 3 – 4% growth as strong. However, that is in a world where there are few slack resources. This is not our world. Our world has plenty of idle resources.

6% growth is not unrealistic. I urge the Fed to push towards that goal. High profits and growing government revenues are great but we need to put people back to work.

The Mankiw Rule for example doesn’t call for raising the funds rate above zero until the (unemployment rate – core inflation) rate drops below 6. Right now we are still above 7.5

Indeed here is what the Mankiw Rule says the Fed Funds rate should be

We are still deep into negative territory meaning that we need additional monetary stimulus above and beyond a zero interest rate.

As a side note, I would love to claim that QE2 is behind this increased growth but that is premature. The timing is right on, but we need more evidence before we can claim intellectual victory.

Karl posted something that he should have titled “Stream of Consciousness” instead of “Unsubstantiated Claims” where he thought out loud. One of those thoughts landed on the Fisher effect.

My sloppy writing makes it sound as if I am saying Reihan should read up on the Fisher effect. What I mean to say is that Reihan brought up the fact that people fear inflation eroding savings. These fears are common. I have had many a Facebook debate over them. Indeed, Ron Paul has repeatedly pointed to this has his main reason for fearing debasement of the currency.

I believe that the Fisher effect is controversial among Austrians, and Keynes didn’t believe in the relationship at all, except under hyperinflation. Using price inflation in the Fisher equation makes a lot of things confusing, because the composition of output under recession circumstances (less than full employment — or a flat SRAS) is that raising inflation expectations to, say, 3% from 2% will likely cause an increase in real output, leaving inflation at it’s long-run target. Indeed, the Fed isn’t even interested in boosting inflation expectations past its set 2%, and has made that very clear. What the Fed wants is higher NGDP…but unfortunately it operates under a target for nominal interest rates.

Scott Sumner has a post about how inflation is, counterintuitively, good for savers. The thrust of it is that raising NGDP expectations will raise the Wicksellian real interest rate. People will spend more on investment (maybe not consumption, but probably), and we will get far more output, while trend inflation remains intact (and if it doesn’t, then the Fed can act as necessary). This is a boon to savers, as it raises not only the interest rate on savings accounts, CD’s, and the yield on bonds…it raises other asset prices as well, like stocks, real estate, commodities, etc. All are vehicles for saving, and a higher level of NGDP causes every type of investment to increase its yield.

This is the fundamental reason inflation is confusing. People think a lot about cash, but not many people save in cash (as in safes) under a normal positive trend inflation rate — criminals mostly. I think that price inflation is just muddying the debate here, and is completely useless.

A little late, I know, but Happy Thanksgiving everyone!

Remarks from Ben Bernanke indicate that the Fed is shooting itself in the foot:

“I have rejected any notion that we are going to try to raise inflation to a super-normal level in order to have effects on the economy,” [Bernanke] said.

In fact, the Fed should engage in level targeting, as I have been pushing in the last few posts. It should commit to a higher target for nominal expenditure in order to return to the previous trajectory from the Great Moderation. That requires a higher level of NGDP growth than is “normal” in order to catch up. One way to do this under the current monetary regime is to create higher inflation expectations. Do they need to be much higher? I don’t think so, but it’s not entirely unreasonable to disagree.

So we know that most members of the FOMC view 2% as the preferred inflation target. We now also know that the Fed is holding true to that target, come hell or high water. 2% is better than 1%, but a temporarily higher target would produce a much more robust recovery. Arguably, the Fed is in the business of providing stable NGDP growth consistent with high employment and low inflation. It allowed NGDP to plummet and now they should be trying to make up that lost ground as quickly as possible. This statement is clearly against that goal.

We’re in for a rocky road if our monetary authority sees it fit to tie its hands.

Inflation is confusing. The concept makes crazy people crazier. And even worse, it makes otherwise sober people disagree with eachother. Reading through the accounts of QE2 on the internet the past few days have solidified my view that inflation is a thorny enough concept that we should rid it from popular vernacular. Is inflation important? Sure…but what measure of inflation is correct? CPI-U? GDP Deflator? Your crazy uncle’s index? Does inflation help or hurt savers in the current landscape?

If there is anything that gets turned on it’s head when an AD recession hits, it is the concept of inflation. During normal times (full employment and capacity utilization), inflation is harmful as it drives up interest rates, discourages saving, and encourages misallocation of capital. However, none of those things apply to the current situation in which we find ourselves with a large output gap and high unemployment. Thus, we need higher inflation in order to close the output gap (the difference in money expenditures between where we are currently, and the trend rate from the Great Moderation…currently about -13%), but that turns everything that everyone knows about inflation backward. All of a sudden inflation is good for savers, good for the unemployed, and good for economic growth. Well, stable inflation expectations are key…but it’s hard to steer a ship, and it’s hard to get a non-confusing answer out of pundits and other commentators.

In order to square this circle, I propose we forget about inflation. And not just forget about talking about it, but forget about its use in the setting of monetary policy. Instead, we should target nominal expenditure at a steady growth rate (3% a la Woolsey, or 5% a la Sumner, Beckworth, etc.) with level targeting. What advantages does targeting nominal expenditure have? Well…

- Targeting nominal expenditure (NGDP for short) allows monetary policy to better address recessions which arise from both aggregate supply and aggregate demand shocks. David Beckworth has an excellent discussion of this point.

- NGDP is a better indicator of monetary shocks than inflation indicators like CPI. Because prices are sticky, and because measures of inflation are so problematic, a fall in NGDP won’t immediately show up in inflation numbers. Also, if there is a large price shock in something like oil, this will raise the money price of all goods and services, causing anyone focusing on inflation to miss the underlying weak economy…and thus potentially set monetary policy to be too contractionary (sound familiar?).

- NGDP allows us to broaden our focus to aggregates like MZM, asset prices, yields, excess reserves etc. We’ll relinquish our inane focus on interest rates, which are a very problematic indicator of the stance of monetary policy, and have a much better picture of the health of the economy.

- NGDP sounds better. People have an innate fear of inflation. Inflation destroys savings, after all…and we all know frugal people are virtuous. Well, how about, in the event of a recession, instead of economists clamoring against the crowd that we need inflation, they say that we want aggregate expenditures (and thus nominal income) to be at some level higher than it currently is? Money illusion is a powerful motivator. Who would argue with that?

Targeting nominal expenditure would be a beneficial step from both an economic theory perspective, and a public relations perspective. Lets take the confusing concept of price inflation out of our discourse, so that we can see the world more clearly.

P.S. We are currently 13% below the target path from the Great Moderation, and are where we were at before the crash of Sept/Oct 2008. To make that up by 2011:Q3, the Fed would have to target NGDP at $17.6bn (to continue on a 5% NGDP growth path). However, Bill Woolsey favors a 3% growth path for money expenditures, which means that the Fed would only have to target a 13.8% increase by 2011:Q3 (or $16.4bn), and then continue on with 3% growth, level targeting, from then.

Update: Found the link to Beckworth’s article!

Another chart to steal from Real Time Economics, this time provided by Justin Lahart.

The classic hydraulic macro story would imply that someone is hoarding cash. It would be really nice then if we could look around and see some cash being hoarded. Indeed, we do.

A point I want to make is that none of these pieces of evidence is in-and-of itself conclusive: The small business survey, the flow of funds, inflation expectations, etc.

There could be explanations for all of them that involve something other than the traditional liquidity demand story: that is that recessions are caused by excess demand in the market for cash/bonds/safety.

However, the liquidity demand story suggests that certain things should all be happening at the same time: a decline in the demand for labor, a decline in the purchase of durables, a decline in consumer prices and business’s pricing power, a decline in asset prices, a decline in inflation expectations, an increase in cash holdings, an increase in the ease of finding workers, etc.

And, all of those things are happening.

I like to focus on inflation because I think just about all of us have agreed that inflation is primarily controlled by actions at the Fed. Thus close patterns between inflation and other variables should suggest that they are also controlled by the Fed.

Here is fraction of income spent on durables and inflation.

Ed Leamer likes to say that its all durables and housing. I think there is more going on in housing than money creation but lets check the Leamer story versus inflation.

Looking at durables only suggests that inflation might flatten out soon. Looking at durables and new houses suggests that deflation will be upon us for sure. It will be interesting to see what happens.

Note, however, that this is not saying that a reduction in income spent on durables and housing will cause a decline in inflation. Its saying the Fed has already taken certain actions. The immediate result of those actions is a decline the fraction of income spent on durables and new houses. The future impact of those same actions will be a decline in inflation.

In other words the inflation decline is already baked in. What we have to ask ourselves now is whether we want to take actions that would raise inflation expectations for the medium future.

Update: I probably should have put “during the recession” in the title. Unfortunately it’s gone to press.

Chevelle, at Models and Agents, explains why the previous round of “quantitative easing” performed by the Fed did not have a [sufficient] expansionary effect:

By that metric, the Fed’s past LSAPs have probably fallen short. Clearly, measuring the counterfactual is impossible, but there are reasons to believe that the impact on aggregate demand was small. Why? First, because the reduction in mortgage rates boosted refinancings only by people who could refinance—i.e. people with jobs and some positive equity in their home. Not exactly the most cash-strapped ones who would have spent the extra cash.

Second, the portfolio-balance effect of the LSAPs on the prices of assets like corporate bonds or equities is at best weak, if not counterproductive. The reason (which I explained in detail here) has to do with the fact that US Treasuries and MBS are not “similar in nature” to corporate debt and equities. Unlike the latter, Treasuries/MBS have more of a “safe haven” nature—so that removing them from investors’ portfolios create demand for more “safe” assets, rather than boosting the prices of equities, high yield bonds, etc.

Luckily, one Benjamin S. Bernanke explained how to perform private asset purchases that would, in fact, have an expansionary effect:

If the Treasury issued debt to purchase private assets and the Fed then purchased an equal amount of Treasury debt with newly created money, the whole operation would be the economic equivalent of direct open-market operations in private assets.

If you see that guy around, tell him to talk to the Federal Reserve. I remember hearing a podcast with Scott Sumner a while back where he floated the idea of the Fed buying bonds off of the public (i.e. You and I), and paying for them with cash. Lets get to it!

Will make our lives less worth living until our eventual death anyway.

Paul Krugman complains that its not only the Austerity crowd but the Tight Money crowd that’s switching its tune on the bond markets

So will the OECD call for a drastic shift toward expansionary [monetary] policies, since the clear and present danger, at least according to the bond market, is disinflation (and possibly deflation)?

No, it won’t. The bond market only rules if it tells people what they want to hear.

The odd thing isn’t that people only hear what they want. Confirmation bias is ubiquitous. The odd thing is that so many in positions of authority only want to hear that which justifies greater indifference to human suffering.

Others will see more cynical causes but, my current explanation is that this is a transfer of logic from the way certain body tissues operate. Its clearly the case that skin, muscle and connective tissue respond to stress by growing: a process known as hypertrophy. This might also be the case with nervous tissue and some other, though importantly not all, tissues. This is an interesting and important phenomenon that details the power of highly complex evolutionary systems. Yet, it is a fool’s errand to apply this to the world writ large.

When you stress most things they don’t grow back stronger, they break. When you apply job losses to an economy people don’t become hardier, they become poorer. The idea that tough love will lead to a better economy in the long run is just wrong. Not mean. Not heartless. Not insensitive. Wrong.

Monetary policy doesn’t work that way. Fiscal stimulus doesn’t work that way.

More importantly, I want people to question whether or not you believe in economic toughness primarily because you are extrapolating from your experience with muscle fatigue. Human bias is elusive and works in mysterious ways. You may have learned from an early age that “no pain means no gain” and at a minimum that’s a good rule of thumb when dealing with sarcoplasm. However, this phenomenon is deeply dependent on the nature of sarcoplasm and the metabolic process generally. It does not carry over to the world or equilibrium systems on the whole. You will make deep logical errors if you believe that it does.

And getting the right answer matters. What’s important is not whether what you are saying “feels” true. Unlike Paul, I don’t doubt your sincerity. What matters is whether it is true. The world operates on objective facts and their relationships. The world does not operate on whether you subjectively feel like you did the right or responsible thing. We can talk more later about how responsibility – or compassion for that matter – are mental interpretations. Real world events are the result of the interaction of subatomic particles. Responsibility or irresponsibility can’t cause anything to happen they can only provide an interpretation of events that have actual physical causes. But, like I said more on that later.

The issue today is: what series of logical steps is telling you that we should listen to bond markets when they suggest tighter polices but not when they suggest loose ones?

There is no reason to fear deflation in the price of movie tickets. According to the National Association of Theater Owners, prices have increased $0.40 in 2010, which is an over 5% increase.

This is not entirely price inflation, as part of it reflects a growing number of 3D movies, which charge higher prices. So prices are going up, but you get to see Shrek in 3D, so it all evens out right?

Apparently the industry is beginning to believe they are pushing prices up to the point where consumers are becoming more price sensitive. The article linked above has this account:

Notable was an AMC statement in late May, which called the $20 list price for an IMAX-3D “Shrek Forever After” presentation in Manhattan “incorrect.” Just two months earlier, the chain had raised its premium 3D admissions cost from $16.50 to $19.50.

I know, I know, you’d gladly pay $50 for Shrek in 3D, but not apparently not all consumers feel the same way.

There has been a lot of chatter around the blogosphere about Narayana Kocherlakota’s speech in Michigan last week, and seeing as I am trying to catch up on news, I think that is a good a place as any to start. First, here is the whole speech, so that you can read it if you would like.

The big focus, especially among left-leaning commentators, has of course been Kocherlakota’s comments on the unemployment situation. The only troubling thing to me about a monetary policymaking body discussing unemployment is the fact that it is happening at all. I don’t believe that there is anything “special” that monetary policy can do to alleviate unemployment — even in a booming economy. The capacity of monetary policy to act is to keep nominal GDP growing at a constant rate, year over year, and to tighten a little when it overshoots and loosen a little when it undershoots — such that the trend path of NGDP is a constant upward slope. I’m not an expert on the welfare-maximizing trend rate of NGDP…but people who are much smarter than me on average advocate 5% NGDP growth.

In any case, in the speech, Kocherlakota breaks down how Fed meetings operate, and then breaks down his “forecast speech” that he gave to the FOMC. Along those lines, he has three points: GDP (real), inflation, and unemployment. On those three points, he has this to say:

Typically, real GDP per person grows between 1.5 and 2 percent per year. If the economy had actually grown at that rate over the past two and a half years, we would have between 7 and 8.2 percent more output per person than we do right now. My forecast is such that we will not make up that 7-8.2 percent lost output anytime soon.

[…]

The Fed’s price stability mandate is generally interpreted as maintaining an inflation rate of 2 percent, and 1 percent inflation is often considered to be too low relative to this stricture. I expect it to remain at about this level during the rest of this year. However, our Minneapolis forecasting model predicts that it will rise back into the more desirable 1.5-2 percent range in 2011.[1]

[…]

Monetary stimulus has provided conditions so that manufacturing plants want to hire new workers. But the Fed does not have a means to transform construction workers into manufacturing workers. […] Given the structural problems in the labor market, I do not expect unemployment to decline rapidly. My own prediction is that unemployment will remain above 8 percent into 2012.

[1]5yr TIPS spread is at 1.43, 10yr @ 1.55.

Now, not making up the lost employment is partially a function of his previous point about per capita GDP remaining under trend for an extended period of time. This is the cyclical component of unemployment. Cyclical unemployment is created due to the relationship of the economy to the cycle of time. As such, the level of cyclical unemployment correlates well with the business cycle, seasonal factors, etc. I believe that most of the unemployment we are currently experiencing is of cyclical nature.

I think the error in Kocherlakota’s thinking stems from this quote:

Monetary stimulus has provided conditions so that manufacturing plants want to hire new workers. But the Fed does not have a means to transform construction workers into manufacturing workers.

This is wildly baffling. Not only does Kocherlakota make the forecast above — i.e. we will not be hitting any of our targets (nominal or otherwise) any time soon — he also states that he believes that money has been easy. That implies that monetary policy has zero effect on the economy, any time. He also identifies that low rates for an extended period of time are a sign of monetary failure, but does so in a future-orientation. While it is true that low rates can (and do) accompany* a deflationary “trap”, the policy prescription that follows is not to raise short-term rates regardless of the composition of employment. The proper policy response in that situation is to set a positive nominal target, level targeting and commit to move heaven and earth to hit that target.

That, rather than his statements about unemployment, is what I view as Kocherlakota’s underlying problem.

*H/T to Andy Harless in the comments. Also, read his post about Kocherlakota’s statements.

In a blog post today, Paul Krugman outlines a hypothetical situation that we could find ourselves in:

And this raises the specter what I think of as the price stability trap: suppose that it’s early 2012, the US unemployment rate is around 10 percent, and core inflation is running at 0.3 percent. The Fed should be moving heaven and earth to do something about the economy — but what you see instead is many people at the Fed, especially at the regional banks, saying “Look, we don’t have actual deflation, or anyway not much, so we’re achieving price stability. What’s the problem?”

I wonder if, on a particularly lazy day when Paul Krugman finds it difficult walk upstairs, he claims that he is in the “main floor trap”? But I digress. There is only one culprit in this situation: the dual mandate.

I’m not an expert on the history of the dual mandate, but I would venture a guess that it was the result of a grand bargain in which “price stability” came from the “hawkish” right, and “unemployment” came from the “dovish” left. The nature of the Fed’s dual mandate is such that it allows the central bank to wiggle out of nearly any situation if finds itself in with little consequence. Since the Fed is aiming at two diametrically opposed targets at once (price stability and full employment), it has large discretion upon which it can draw to justify its policy actions.

Is unemployment 9.5% with core CPI inflation falling below 1% and future expected inflation well below target as well? Well, that’s price stability!

How about persistent inflation rates bordering on double-digits while employment booms? Pat yourselves on the back guys!

In reality, and much to the chagrin of leftists everywhere, the modern Fed (1980’s+) has mostly erred on the side of price stability, which in the recent context has meant 5% NGDP growth with a rough average of 3% real growth and 2% inflation. This has allowed for a NAIRU of around 4-5% for the United States as a whole. Of course, that is a rate…and as long as the unemployed are continually in flux — that is, as long as hires outpaces quits and fires — that rate isn’t much of a problem. What is a problem is that the same dual mandate that was praised by some economists during the Great Moderation is now enabling the Fed to shirk its duties (and perhaps even worse, providing cover for “leveling down” with an implicit policy of opportunistic deflation…which is what Krugman implies above).

The Federal Reserve’s mandate is unique in the world. Most other central banks operate under a “hierarchical mandate” which generally stipulates an inflation target. It is hierarchical, because the central bank can set any target other targets it wants, and pursue them in order as long as they have hit their mandated target. The results of this kind of target vary from country to country.

In my opinion, Congress should scrap the Fed’s dual mandate, and instead mandate that the Federal Reserve set an explicit nominal target, and do everything in their power to hit that target (level targeting). If they’re feeling generous, they can give the Fed discretion as to which target they would like to set. If not, I would specify NGDP. I don’t think that the monetary policymaking body of the Federal Reserve should even look at a single unemployment number. They should focus like a laser on their keeping their nominal target in a very narrow range and leave the question of unemployment (which is a real variable) to other policymakers.

Stabilize monetary policy around a nominal aggregate, and I would wager that unemployment would find a way to work itself out with minimal intervention.

P.S. I kind of smile when I think about the Fed “moving heaven and earth to do something about the economy”. I suppose that is because 1) I think that monetary policy can do so and 2) I’m a huge nerd.