You are currently browsing the monthly archive for December 2011.

At Barry Ritholtz’s place a blogger writes

Example of 5 times leverage:

When we buy a house and put 20% down, we buy a house worth 5 times as much as the down payment. If we put $100 thousand down we can buy a house worth $500 thousand. $500 thousand divided by the $100 thousand we put down equals 5 times leverage.

100 times leverage:

By the same calculation ZERO down mortgages were suffice it to say, 100 times leverage, it’s actually more but that’s a discussion for later. Repeat after me, no money down mortgages equal 100 times leverage.

. . .

100 times leverage on the borrowers side times 30 times leverage on the [Too Big To Fail] banks’ side is 3,000 times leverage ON house prices.

Now there is the obvious issue that 100% down is not 100 times leverage but infinite leverage. I think the author knew this but thought that 100 would make more sense and make the numerical demonstration easier.

However, that’s a bad idea, because using INFINITY would have shown you that your numerical example is doesn’t really make sense or at least isn’t telling you what you think.

In particular, since 30 times INF is still INF, the leverage at the bank side is irrelevant to the calculation. Yet, the author set out to show how excessive bank leverage contributed to the crisis. Thus, something went wrong if these measures tell you bank leverage is irrelevant.

The second issue is the phrase ON house prices. Yet, its not on house prices at all. Its on houses. In particular, if you like your house, want to keep it, can afford the payment, etc then movements in its price are not necessarily important to you.

They certainly don’t bankrupt you. They don’t make the house any less house-y. They don’t make the roof stop keeping out the rain, etc.

Leverage has important properties. And, leveraging purely for the purpose of speculating on the market value of some asset is relatively dangerous for the creditor – though not necessarily for the borrower.

This is why creditors are typically loathe to let you do this. However, for the most part neither banks nor home buyers were speculating on the price of houses. They expected both the loans and the homes to produce yield and that yield to exceed the cost of funding.

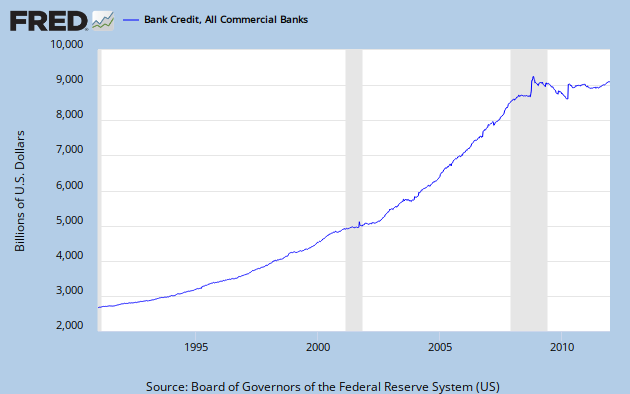

Matt Yglesias pens an extremely readable version of the Smithian view on the near future of the US economy.

What will this recovery look like in concrete terms? Total bank credit, which collapsed during the crisis, is growing again and will keep growing. That will make it easier for Americans to buy new cars and reverse the four years of growth in the average age of America’s passenger vehicles. Families will also invest in other kinds of durable goods—refrigerators, washing machines, etc.—that they’ve been hesitant to upgrade or replace. The housing bust, meanwhile, has been followed by an epic construction slump that’s actually left us with a shortage of homes. But every downward tick in the unemployment rate is another twentysomething moving out of his parents’ basement, stimulating a return to a more normal level of construction. Multifamily housing starts are already up 80 percent over the past year to accommodate the likely coming flood of renters, and there’ll be more to come once people have more cash in their pockets.

This increase in economic activity will boost state and local tax revenue and end the already slowing cycle of public sector layoffs. Re-employment in the construction, durable goods, and related transportation and warehousing functions will bolster income and push up spending on nondurables, restaurants, leisure and hospitality, and all the rest

Not everyone is convinced. Kelly Evans writes

Along with nascent signs of recovery in the housing market, it is tempting to forget about 2011’s disappointments and think 2012 will be the year economists aimed not too high, but too low. Trouble is, recent history suggests it usually turns out the other way around.

Some of this skepticism is I think fueled by the fact that in the winters of 2009 and 2010, things were looking up as well, only to fall apart as the Spring and Summer came along.

This, it appears, was largely a computational artifact. The winter of 2008 was so shockingly and inexplicably bad that the computer programs designed to analyze economic data concluded that winter must be the most perilous time for an economy.

When they saw tepid but not disastrous winters in 2009 and 2010 the computers concluded that the economy must be on sure footing. If the winter isn’t awful then how bad could things really be they reasoned.

Of course, there was nothing about the “winter” itself that was so bad in 2008. It was simply that most dramatic drop in 75 years occurred after Lehman collapsed in mid-October.

Smithianism, however, is not charting. It asks fundamental questions about how people are going to live and work. It then combines that with what we know about the way money and finance work to produce a forecast for the overall economy.

I should resist the urge to wax more philosophic but of course I won’t.

Part of the underlying view here as well is that there is only one world, though there are dozens if not hundreds of reasonable narratives about that world. To the extent that those narratives reflect the world they have to be using different words and phrases for the same thing.

So despite radically different frames, New Keynesianism, Old Keynesianism, Monetarism, Market Monetarism, Modern Monetary Theory, New Monetarism, Vector Autoregression Forecasting, the kitchen table economics of the average family and the synergistically strategic jargon of corporate board rooms, must all be referring to the same underlying mechanics.

Some typical assumptions might be faulty or tweaks necessary to make them give the same answer. But, we should be able to do it. Indeed, much of the time the answers aren’t even substantively different, its just a hidden normative spin that’s different.

What all these narratives tell us is that a recession is somehow related to people not buying stuff. So, the natural questions then are

1) What are they not buying?

2) Why are they not buying it?

A cursory look at the data makes the answer to the first question abundantly clear: cars and houses. Or, more generally, transportation equipment and structures.

Its not even really a close call here. At the nadir of the recession year-over-year sales of motor vehicles and parts was collapsing at, $240 Billion, faster than all other non-gasoline retail and food service sales combined.

The peak-to-trough fall in total final sales of domestic product was roughly $400 Billion. During that same period residential construction spending fell by $200 Billion and from its peak-to-trough residential construction spending fell by close to $500 Billion.

Here is a rough and ready comparison of final sales of domestic product with and without construction and transportation.

The data series aren’t fully comparable, so don’t take that graph to the bank, but it gives you a sense of the importance of those areas to US sales.

Now you can pipe this through any narrative you want and say that:

- Once consumer balance sheets collapsed even a zero federal funds rate was too high to make it optimal for consumers to keep buying transportation and structures.

- Fear among investors and consumers caused them to scale back purchases of long lived items like transportation and structures

- The federal reserve failed to accommodate a huge spike in the demand for money leading to a fall in the demand for transportation and structures

- The federal reserve tightened monetary policy in late 2008 causing a decline in the demand for transportation and structures

- Total debt levels in the economy began to decline in 2008 leading to inadequate demand for transportation and structures

- Failures in the banking system caused a tightening of credit in 2008, leading to less purchases of transportation and structures

- The shock from the fall in asset values in 2007-2008 rippled through the economy leading to a decline in the purchase of transportation and structures

- With retirement accounts and homes collapsing in value, folks thought twice about going out and making big ticket purchases like transportation and structures.

- Consumer deleveraging led to a decline in discretionary purchases of transportation and structures.

However, these are all talking about the same thing. Something happened to credit markets that made people unwilling or unable to purchase transportation and housing.

Thus to a large extent we can judge the ebbing of this phenomenon by looking at whether people are more willing or able to purchase transportation and housing.

Part of that depends on how badly people need new transportation and structures. Part of that depends on whether they can get easy financing for transportation and structures. Both of those things are improving. This leads to a baseline view that the process causing the Great Recession is about to unwind.

I’m drawing here from the sample of economics blogging that we’ve re-blogged about at Modeled Behavior. What I’m learning about myself is I really like rebuttals, possibly to an epistemically unhealthy degree. I guess I should probably be bothered by this a little and worry that it gets in the way of truth seeking. In any case, these are my nominations, and I encourage readers to nominate their favorite posts of 2011 in the commenters.

First is a rebuttal of Steven Landsburg from Will Wilkinson that I wrote about here. It’s a victory for common sense over the familiar style of attempted uber-rationality that is too often abused by economists. Will’s original post is here:

“Economists like Mr Landsburg specialise in the study of instrumental rationality. To act rationally in this sense is to take the means most conducive to one’s ends. Sadly, means-ends rationality and epistemic rationality are often at odds. Fallacious arguments can be the best means to noble ends. If we were to concede, for the sake of argument, that Mr Wahls did fallaciously attempt to rebut a statistical argument with an anecdote, it may remain that he acted not “in the service of intellectual misdirection”, but instead acted with exemplary rationality and morality by speaking eloquently in the service of justice. The kind of humanising anecdote Mr Wahls offered does in fact tend to elicit sympathy and weaken ill-founded prejudice. Maybe the relatively tolerant attitude of people with gay friends and family flows from some kind of statistical slip-up, but that’s how we are. A rational rhetorician takes his audience’s inclinations, rational or not, into account.”

The next is Reihan Salam offering up some persuasive counterpoints against two popular examples of government spending that we tend to take as uncontroversially beneficial: the space program and the U.S. highway system. Reihan wrote:

A shockingly large number of people, including Obama, seem to believe that had the federal government not stepped up to the plate in the postwar era and invested vast sums in highways and putting a man on the moon, the United States would have wound up an economic backwater. But perhaps not building a huge network of highways would have kept American families in more compact, walkable neighborhoods. Instead of sprawling suburbs and SUVs, we’d have more high-rises and bike lanes. The Interstate Highways helped supersize America’s government, by centralizing authority in D.C., and our waistlines, by encouraging us to drive and to fatten up on fast food. It’s not obvious to me that we’re better off as a nation plagued by high taxes and heart disease.

As for Sputnik, it led to a huge increase in federal funding for scientific research and K-12 education. Had we allowed the Russians to beat us to the moon, American families and firms might have kept more of their own money. Our state universities might have devoted themselves to churning out job-ready graduates instead of chasing federal grants. While the Soviets built enormous cities on the moon and Mars, financed by forced labor, we’d have devoted ourselves to becoming a richer, freer, more creative country. I love Neil Armstrong as much as the next guy, but I’d take that trade in a heartbeat.

Next is yet another one from Reihan where he challenges another popular claim: that the U.S. should look to China to learn to how grow fast. What I liked about Reihan’s previous argument was the boldness and novel way he challenged an intuitive and widely held claim. Here the claim is much more obviously false, and I see Reihan’s argument as the most concise and definitive rebuttal, and the last one that ever needs to be written. My post on this is here, and his original is here:

To really learn from the Chinese, and to enjoy such staggering growth rates, we should go about things differently: let’s have a Maoist insurrection followed by a civil war that lasts for several years. Then let’s destroy most of the wealth in the country, and drive out millions of our most enterprising and educated citizens by launching systematic terror campaigns during which millions of others will die in violence or of starvation. Next, let’s have a modest economic opening in coastal regions: impoverished citizens will be allowed to launch small-scale township and village enterprises and components will be assembled in a handful of cities by our stunted descendants. Then let’s severely curb those township and village enterprises because they represent a potential political threat and invite large foreign multinationals and state-owned enterprises [let’s not forget those!] to work our population to the bone at artificially suppressed wage rates, threatening those who complain with serious reprisals up to and including death. Let us also initiate a population control policy designed to improve our dependency ratio for a few decades. As large numbers of workers shift from low-value agricultural work to manufacturing, we will experience … rapid growth! Mind you, getting from here to there will involve destroying an enormous swathe of our present-day GDP.

The last one is Ezra Klein’s epic smackdown of Agricultural Secretary Tom Vilsack, who sought the interview after Ezra wrote a piece critical of rural subsidies. The fact that Vilsack wanted to do the interview and clearly thought he was going to tell Ezra a thing or two adds to the impressiveness of Ezra’s smackdown. Here is my original post on it, but you should read the whole thing:

Tom Vilsack: …Rural America is a unique and interesting place that I don’t think a lot of folks fully appreciate and understand. They don’t understand that that while it represents 16 percent of America’s population, 44 percent of the military comes from rural America. It’s the source of our food, fiber and feed, and 88 percent of our renewable water resources. One of every 12 jobs in the American economy is connected in some way to what happens in rural America. It’s one of the few parts of our economy that still has a trade surplus. And sometimes people don’t realize that 90 percent of the persistent poverty counties are located in rural America.

EK: Let me stop you there for a moment. Are 90 percent of the people in persistent poverty in rural America? Or just 90 percent of the counties?

TV: Well, I’m sure that more people live in cities who are below the poverty level. In terms of abject poverty and significant poverty, there’s a lot of it in rural America…

Is this the worst paragraph about economics, at least from a major newspaper, in 2011?

North Dakota currently has the nation’s only state-run bank. Supporters point out that the state is the only one to have had a budget surplus since the economic crisis began, and has an unemployment rate below 4%.

I don’t consider the idea of public sector bank or something like it to be completely absurd, but for this reporter to allow even the hint of a connection between a public sector bank and North Dakota’s economic success is just terrible, irresponsible journalism. Perhaps North Dakota’s recent oil boom that has included a tripling of output over the past few years has something to do with the budget surplus and low unemployment rate? Or maybe it was the state bank that has existed since 1919. I guess it could be either.

One question I want to ask about public sector banks is this: would the financial positions of fiscally troubled states be better or worse if they had public sector banks over the last 15 years? What would the financial position of the State Bank of Illinois be? I know where my bet is.

Tyler Cowen gives me a smooth handle on something I have been meaning to mention.

That request was the first on the list and it came from Ezra Abrams, who wrote:

Wealth is equal to raw naked power: the power to fund PACs; the power to endow university chairs to influence people; the power to tear down neighborhoods and erect shopping malls. to what extent does the increase in wealth and income of the upper x% (relative to median or some other broad measure) mean that too much power is concentrated in the hands of too few people one amusing example is from Kahnemann’s thinking fast and slow. Small schools show the best results b gates poured money into small schools However, what gates didn’t realize is that this is a small numbers artifacts; small schools show the best and worst results cause with a small school you can deviate from the mean …there you have raw naked power having a huge influence on educational policy

I disagree with most of that. The scholarly literature suggests that campaign finance reform doesn’t matter as much as people think.

The big banks control our government less than some critics have suggested.

Academics are quite liberal/democratic, yet college students seems to be slightly more conservative than the American public as a whole. The major impact of endowed chairs is to cement the roles of Harvard, Princeton and comparable schools as intellectual leaders.

My observation is that people get the causation backwards here most of the time. People are not typically powerful because they are rich, they are rich because they are powerful.

One of the things that people tend to do with power is acquire command over good and services, which is also known as wealth.

I should like to die of consumption . . Because the ladies will say, “look at that poor [Lord] Byron, look how interesting he looks in dying.”

If there is scientific infighting more significant than that over macro-stabilization, it is that going on inside the Psychiatric community.

What make its particularly hard, however, is in most pursuits we can always lean back on the notion that if we hope to make the best world, then understanding the world as it is – not as we wish it to be – is our best hope. This is not true with mental disease.

In many different ways, not just in the debate over psychotropics, the truth may increase suffering. There are times when you know that forcing someone to acknowledge their insanity, is nothing less than cruel. .

Gary Greenberg gives a admirably even handed take – given what I know his beliefs to be – on the run-up to the DSM-5. Of course, he still lobs the standard grenade:

The fact that diseases can be invented (or, as with homosexuality, uninvented) and their criteria tweaked in response to social conditions is exactly what worries critics like Frances about some of the disorders proposed for the DSM-5—not only attenuated psychotic symptoms syndrome but also binge eating disorder, temper dysregulation disorder, and other “sub-threshold” diagnoses. To harness the power of medicine in service of kids with hallucinations, or compulsive overeaters, or 8-year-olds who throw frequent tantrums, is to command attention and resources for suffering that is undeniable. But it is also to increase psychiatry’s intrusion into everyday life, even as it gives us tidy names for our eternally messy problems.

Its standard to object to the medicalization of everyday disorders. Where does it stop, people ask? Is everything a disorder?

It never stops, I answer. And, it’s a disorder if you dislike it.

The normative element in non-mental health conditions is somewhat hidden because death, disability and pain are almost universally disliked. So, if I say cancer is a disease because it kills, no one is likely to object to this. It doesn’t matter that cancer is, almost as much as anything, a part of life.

As far as we can tell no human has ever been born without the propensity to develop cancer. That people don’t die of cancer is purely a function of the fact that they die of something else before the cancer gets them.

So, why is cancer not just a part of life? Part and parcel with being a multicellular organism? The simple answer is that it causes death, disability and pain. These are widely recognized as bad and so is cancer.

What about feeling sad? To my knowledge no human has ever been born without the propensity to feel sadness. Is sadness simply part and parcel with life? The answer from my corner is, not if you don’t want to be sad.

This is the rub in all mental illness. It is the malady of not wanting to experience the world as we do. And, it raises the deepest questions about what it means to improve wellness.

I stick firmly to the notion that we improve wellness when we alter physiology to produce a preferred state of being. Preference is in the eye of the patient.

However, I do know the question “Am I sick?” has moral meaning to people. Giving a name to a condition can bring comfort or despair, even when it doesn’t change the essential experiences of the person at all.

A while back Kevin Drum asked

Politicians and corporations engage in meaningless puffery all the time, but to be effective it has to be based on at least a tiny core of truth. . . .

. . . So what’s the strategy here? In the primaries, I assume he’s calculated that it just doesn’t matter.

. . . But what about the general election? Independents aren’t going to go for this stuff. They’ll just shake their heads and wonder what the hell he’s talking about. So is he going to ditch this stuff completely after he’s won the nomination and pretend that he never said it? Or will he keep pressing, literally hoping that if you say anything often enough you can get people to believe it? It is a mystery.

Actually I’ve found the question fascinating from the opposite perspective: why do politicians in particular base so much of their campaign propaganda on things that are arguably truthful?

For corporations, you have the customer disappointment problem. If you make a completely untrue statement AND that statement convinces a person to buy your product you face a disappointed customer who will not only not purchase again but bad mouth you to other people.

Note, that there are a lot of folks who won’t care. They will buy the product regardless. But, then they would have bought the product regardless, so why bother lying?

Its only the marginal customer who will be enticed by the lie and it is her who is most likely to be disappointed.

Note, also that fly-by-night operations do not suffer this problem and so do indeed rampantly lie.

What about politics?

Well, here the ability to judge what you “bought” is far harder. Moreover, I tend to think the marginal voter is not even really interested in what he or she is buying.

The marginal voter is either expressing displeasure with the current state of affairs. This underlies the “Time for a Change” models in political science. Or, he or she is responding to a message.

In the former case, it doesn’t matter much what you say. In the later case its much more important that you be clear about which tribe is which than about any policy details.

So, to bring us back to this example Romney is saying “I am of the pro-capitalist tribe” Though even that is not really accurate. Romney himself probably does care about capitalism but I doubt the marginal voter does.

He is really saying “I am of the pro-Karma tribe” in my tribe believes that people get what they deserve. Then he describes Barack Obama as wanting to institute a government that defies Karmic Justice. Its completely clear what side Romney is on.

Whether Obama wants to do this is fundamentally immaterial. The voter neither knows nor cares what Obama wants to do. The voter cares about tribal affiliation, and that’s what Romney is offering.

So, the question for me is – why isn’t this par for the course.

Part of it I think is – or at least was – a small fear that the Mainstream media would out and out call Romney a liar. That’s a horribly character tag to have and would cause voters not to want to affiliate with him. If that tag became conventional wisdom it would be damaging.

Perhaps more importantly though, I suspect much of it has to do with building a campaign team. While the average voter might not care how Romney is looked upon by the policy elite, his staff probably does. They would prefer not to associate themselves with someone who has low status in the beltway.

However, as the GOP continues to push back against the MSM, a crop of staffers has growing up who are less sensitive to such things. Thus you don’t have to worry that your entire team is looking at their shoes when you speak.

That I would guess, allows politicians to pursue a more direct strategy of agitprop.

Paul Krugman wades into debt fundamentals

People think of debt’s role in the economy as if it were the same as what debt means for an individual: there’s a lot of money you have to pay to someone else. But that’s all wrong; the debt we create is basically money we owe to ourselves, and the burden it imposes does not involve a real transfer of resources.

That’s not to say that high debt can’t cause problems — it certainly can. But these are problems of distribution and incentives, not the burden of debt as is commonly understood. And as Dean says, talking about leaving a burden to our children is especially nonsensical; what we are leaving behind is promises that some of our children will pay money to other children, which is a very different kettle of fish.

Just to keep each other honest. I am pretty sure I know what Paul means but the bolded line is not exactly true. Most likely there will be real resource transfer, just within the country not between countries. Such resource transfer is not frictionless, however.

This is easiest to see when the resources are transferred from taxpayers to bondholders . Even if these are the exact, exact same people the transfer itself involves taxation and thus deadweight loss. Whether it involves measurable loss of production is another issue, but its fairly clear that it involves deadweight loss.

More generally though I would like to encourage people to think of debt as promises.

One thing that I hope this can help us see is that there is no limit to the number of promises we can make between each other. I make a promise to you. You make a promise to me. Back and forth we go, and we just become ever more entwined with one another.

However, there is no real limit to how many promises we can make, thus there is no limit to how high debt levels can go.

The promises, that are our debt, allow us to co-ordinate our activities more tightly. If I know that you will be there for me when I need you I can take on certain tasks that I could not otherwise.

What’s dangerous about promises is that they may not be kept. When we depend on others and then others don’t come through for us we can be hurt. This is true in love, life and finance.

The more promises (debt) we have the more dependent we are on each other and the more it will hurt when one us – inevitably – doesn’t live up to those promises.

However, this alone is not a reason to fear a world of debt anymore than broken hearts are a reason to fear a world of love.

Now, in love and money people do shy away from commitment – explicit or otherwise. I think this is over done. You have to let other people make their choices. So long as you are upfront about what it is that you have to offer you should let your suitors fall in love with you if they wish and the bank loan you money if it wishes.

Their hearts and their money are their own.

Perhaps, if not bailouts you say? Well, more on that later.

Paul Krugman wades into debt fundamentals

People think of debt’s role in the economy as if it were the same as what debt means for an individual: there’s a lot of money you have to pay to someone else. But that’s all wrong; the debt we create is basically money we owe to ourselves, and the burden it imposes does not involve a real transfer of resources.

That’s not to say that high debt can’t cause problems — it certainly can. But these are problems of distribution and incentives, not the burden of debt as is commonly understood. And as Dean says, talking about leaving a burden to our children is especially nonsensical; what we are leaving behind is promises that some of our children will pay money to other children, which is a very different kettle of fish.

Just to keep each other honest. I am pretty sure I know what Paul means but the bolded line is not exactly true. Most likely there will be real resource transfer, just within the country not between countries. Such resource transfer is not frictionless, however.

This is easiest to see when the resources are transferred from taxpayers to bondholders . Even if these are the exact, exact same people the transfer itself involves taxation and thus deadweight loss. Whether it involves measurable loss of production is another issue, but its fairly clear that it involves deadweight loss.

More generally though I would like to encourage people to think of debt as promises.

One thing that I hope this can help us see is that there is no limit to the number of promises we can make between each other. I make a promise to you. You make a promise to me. Back and forth we go, and we just become ever more entwined with one another.

However, there is no real limit to how many promises we can make, thus there is no limit to how high debt levels can go.

The promises, that are our debt, allow us to co-ordinate our activities more tightly. If I know that you will be there for me when I need you I can take on certain tasks that I could not otherwise.

What’s dangerous about promises is that they may not be kept. When we depend on others and then others don’t come through for us we can be hurt. This is true in love, life and finance.

The more promises (debt) we have the more dependent we are on each other and the more it will hurt when one us – inevitably – doesn’t live up to those promises.

However, this alone is not a reason to fear a world of debt anymore than broken hearts are a reason to fear a world of love.

Now, in love and money people do shy away from commitment – explicit or otherwise. I think this is over done. You have to let other people make their choices. So long as you are upfront about what it is that you have to offer you should let your suitors fall in love with you if they wish and the bank loan you money if it wishes.

Their hearts and their money are their own.

Perhaps, if not bailouts you say? Well, more on that later.

In a previous post I quoted a financial advisor who called Ron Paul’s portfolio “a half-step away from a cellar-full of canned goods and nine-millimeter rounds”, and I argued this reflected his crazy beliefs about the probability of economic collapse. It might be worth noting then, as commenter Ragout points out, that two of the other GOP candidates probably literally have a cellar-full of canned goods in preparation for a disaster scenario:

So Ron Paul, by investing in gold stocks, is preparing for a hyperinflation apocalypse where the stock market still functions. Note that the Mormon church calls upon its members to store 2 years of dried food, if they can afford it. So it’s likely that Mitt Romney is preparing for a real apocalypse, where there isn’t enough food to feed America.

Of course Jon Huntsman is the other Mormon in the race, which makes two candidates that are potentially literally preppers. This is from the official website of the LDS church:

“Our Heavenly Father created this beautiful earth, with all its abundance, for our benefit and use. His purpose is to provide for our needs as we walk in faith and obedience. He has lovingly commanded us to ‘prepare every needful thing’ (see D&C 109:8) so that, should adversity come, we may care for ourselves and our neighbors and support bishops as they care for others.

“We encourage members worldwide to prepare for adversity in life by having a basic supply of food and water and some money in savings.

“We ask that you be wise as you store food and water and build your savings. Do not go to extremes; it is not prudent, for example, to go into debt to establish your food storage all at once. With careful planning, you can, over time, establish a home storage supply and a financial reserve.”

They advise the creation of a 3 month supply of food, but also suggest if possible storing for longer-term:

For longer-term needs, and where permitted, gradually build a supply of food that will last a long time and that you can use to stay alive, such as wheat, white rice, and beans.

If Romney and Huntsman are actually prepping, what does it tell them about them? Should this be considered a “crazy belief” of theirs as Paul’s prepping is for him? I don’t think so. Their preparations don’t tell us much about how probable they actually think a disaster is, but rather reflect them adhering to a tradition.

You might argue that preparing for disaster because you believe God wants you to is in fact a crazy belief. But religious belief comes bundled with group membership, and many acts are just adherence to tradition, not wanting to rock the boat, or signaling required to maintain group membership rather than true expressions of literal belief. And at the very least religious beliefs are so widespread that I don’t think they all have the same correlation with other crazy beliefs as, say, believing an society destroying economic collapse is coming soon. I think some religious groups and people manage to hold what I’ll politely call highly unlikely beliefs in one part of their brains, and a pretty non-crazy overall set beliefs in the other part.

In any case, I do find it amusing that there are a grand total of three candidates who are preparing in some form for an extreme disaster.

Bill Gross wrote in the FT that zero interest rates could actually contract the economy. That’s wrong but I want to spell out in greater detail than I have seen, exactly why.

Here is Gross

If a bank can borrow at near 0 per cent, then theoretically it should have no problem making a profit. What is important, however, is the flatness of the yield curve and its effect on lending across all credit markets. Capitalism would not work well if Fed funds and 30-year Treasuries coexisted at the same yield, nor if commercial paper and 30-year corporates did as well. It is not only excessive debt levels, insolvency and liquidity trap considerations that delever both financial and real economic growth; it is the zero-bound nominal yield, the assumption that it will stay there for an "extended period of time" and the resultant flatness of yield curves which are the culprits.

Gross is concerned that flattening the yield curve destroys the traditional business of banking. Part of the confusion is not separating the difference between what I call financing and carrying.

Financing in my terms is generating liquidity from a non-liquid asset. One does this by rolling over or otherwise juggling short-term liabilities in such away that you always have enough net borrowing to fund a long term investment.

If you keep shifting your balance from one credit card to another so as to keep your interest payments low enough to make that deck renovation affordable then you are self-financing the deck. This will work so long as you can always find a new low introductory rate. However, this is risky which is why most people just get a home equity loan from a bank and let the bank juggle its deposits to make sure the money is always there.

Carrying is when you borrow money cheaply and then lend it out more expensively, or otherwise take advantage of a higher return. Carry is generally available to you because you are taking on some risk that the original lender did not want to take on. Indeed, you are carrying that risk for her.

So, if your neighbor needs a deck renovation badly but has awful credit, then you can take out a home equity loan at 5% and the loan the money to him at 7% and earn the 2% spread. You have not created any liquidity nor are you juggling claims. You are just carrying your neighbor for the bank.

Though we think of banks as making money by financing the fact that they have a huge capital stock and lots of detailed information on borrowers means that they can also profit by carry. Lending at least ought to be fundamentally less risky for them because they have more information and a larger buffer. This is why a bank can make money selling you Certificates of Deposit.

Certificates of Deposit, if used to fund a loan of equal duration are purely a carry trade.

Now, Gross is right. If in the extreme the Fed guaranteed a 0% Federal Funds rate for the next 30 years it would eliminate liquidity risk. Remember that the Fed Funds market is unsecured overnight lending.

The Fed would essentially be saying that for the next 30 years banks will always be able to borrow whatever they need to make sure that you have funds on hand and they will be able to do it for free.

Since, liquidity risk has been eliminated the profit from financing has been eliminated – or should be arbitraged away by competing banks – and so there is no money to be made in financing.

Yet, oh heaven is there money to be made in carry.

So much money.

So, so, so, so, so much money.

The chaos and pandemonium in the wake of such a (credible) announcement would be unlike anything you have probably ever imagined. It would dwarf any global financial crisis in history except it would be in reverse. It would be the melt-up to end all melt-ups.

So rather than try to step you through the event chain associated with that stampede of insanity. Let’s think about what would happen if this was offered to just one bank. This institution now has access to unsecured financing at zero percent for 30 years.

Lets start with equities. An equity that has any dividend yield at all is now a good buy at any price less than what you think the nominal price will be 30 years from now. So suppose there is no real growth in stock values. But there is 2% inflation for 30 years. Then right now, today, you’d be willing to pay at least 80% more than the current trading price for any stock with any dividend whatsoever.

The same thing goes for real estate. So, long as a property has any positive rent flow you’d be willing to pay at least more than its current value. Even if you thought real estate prices were going to fall another 30%, you’d still be willing to pay 50% more than the current values for it.

This means an instant and huge rise in stock and real estate values, which in turn means an instant repairing of household net worth.

Yet, we are really understating the case here for simplicity. We can look at rent-ratio on real property. Even if you knew that at the end of 30 years the property you were buying was going to be completely worthless. We are talking ghost town level value collapse. Neither the land nor the building materials are worth a dime.

You would still be willing to pay roughly 30 times the annual rental price, assuming no inflation, 40 times assuming 2% inflation.

Here is a chart of the rent ratios in major cities over the course of the housing bubble.

At two percent inflation San Francisco would be fair priced at the peak, even assuming that in 30 years a massive earthquake would come in and destroy your property and leave you with no insurance settlement whatsoever.

The Northeast Corridor would be a steal even in a zero inflation environment. A guaranteed zero rate for 30 years would allow you to buy up almost every real asset in America at well inflated prices and make a killing.

Of course, the attempt to do that would not only increase the paper wealth of all American but for those who actually sold it would should money in their pockets. If you were able to buy even 10% of the assets that it would be profitable to buy at prices 50% above where they are today then you push roughly $5 Trillion dollars of cash into the hands of households and firms.

That money will need to be spent on something. It can’t be reinvested in existing assets because the very reason it cashed out of the market was because you as the bank drove up prices to the point where these folks wanted out.

Almost certainly most of it would be used to finance new investment. New companies, new housing, new capital. Some of it would be used for consumption. And, much of it would go overseas.

In all cases, however, it raises US aggregate demand and by an enormous amount. At a velocity of 1.5 on MZM it would raise Aggregate Demand by 7.5 Trillion or roughly 50%. This means nominal would rise $22 Trillion. That’s well above the CBO projected potential nominal GDP of $16 Trillion or a straight line 5% extrapolation from 2007 of $19.5 Trillion.

This implies that not only would the economy hit full employment but very rapid inflation would ensue as well.

And, remember that this in turn means that the price you would be willing to pay for real assets rises further still. This means a greater injection of money and even more inflation.

Rather than being contractionary, the credible promise of a zero percent funds rate for 30 years would be hyper-inflationary.

This is precisely why

A) Central Banks are weary of long term promises

B) Such promises are not in fact credible

However, there is nothing about the zero interests that produces the opposite effect from lowering interest rates in general.

I have a lot of posts I’d like to get up before the New Year, but one thing I’ll note quickly is how revelatory the blogosphere has been.

One thing that can easily pass you by is the dearth of analytical ability in the world. When you talk to experts you can be confused into thinking that they are sharper than they are because they have been thinking and talking about the same things for a long time.

However, in the fast and furious world of the blogosphere it quickly becomes apparent how shallow much of that understanding is and how widespread the inability to transfer insights between domains is as well.

Obviously I wouldn’t be so crass as to name names but the overall pattern is impressive.

There’s a lot of justifiable shock today at a Wall Street Journal report on what Ron Paul’s portfolio consists of:

Most members of Congress, like many Americans, hold some real estate, a few bonds or bond mutual funds, some individual stocks and a bundle of stock funds….But Ron Paul’s portfolio isn’t merely different. It’s shockingly different.

Yes, about 21% of Rep. Paul’s holdings are in real estate and roughly 14% in cash. But he owns no bonds or bond funds and has only 0.1% in stock funds. Furthermore, the stock funds that Rep. Paul does own are all “short,” or make bets against, U.S. stocks. One is a “double inverse” fund that, on a daily basis, goes up twice as much as its stock benchmark goes down.

The remainder of Rep. Paul’s portfolio – fully 64% of his assets – is entirely in gold and silver mining stocks.

This tells us a few interesting things about Ron Paul. First, it is more evidence of his distrust of experts or of experts with beliefs within the mainstream. You would be hard pressed to find a non-crank economist or financial advisor who would suggest such a portfolio. Is there any economic issue about which Paul does not have extreme beliefs?

The investment advisor the WSJ talked to had this to say:

Mr. Bernstein says he has never seen such an extreme bet on economic catastrophe. ”This portfolio is a half-step away from a cellar-full of canned goods and nine-millimeter rounds,” he says.

What would it tell us about Ron Paul if he literally had a cellar-full of canned goods and nine-millimeter rounds? And what does it tell us about the average person who chooses the so-called “prepper” lifestyle?

In effect you are spending a lot of time and money insuring against one highly unlikely outcome. Either these people have extreme preferences or extreme probability beliefs. Extreme preferences would mean they would hate being unprepared in a post-apocalyptic U.S. way, way, way more than the rest of us would. Given how much almost any of us would hate it, it’s hard to imagine how their expected disutility in this outcome could be large enough to justify the tens of thousands of times more they spend on insuring than the rest of us do (“But I’m insuring against this zero” you object, but admit it: when you spend that extra $10 on the fancy maglite flashlight, visions of a post-apocaplyse and a thought of “just in case…” zipped through your mind. Don’t worry, I won’t tell your wife* you’re a prepping just a little bit). So I think this rules out extreme preferences as the primary determinant, which leaves you with extreme beliefs.

What do extreme beliefs about the odds of complete economic disaster tell you? One thing it suggests to me is bad economic theories. This is the point Krugman his rightly been making about those who have predicted we’d be facing hyperinflation by now. We didn’t need this datapoint to tell us Ron Paul has extreme and crankish ideas about economics, but it certainly reinforces the idea that he is not faking it.

In some part I think beliefs like this also reflect wishful thinking. There is a lot of moralizing that accompanies bad economic theories. As if our failure to adhere to the crank theories makes us in a way deserve economic collapse. The ability to yell “you should have listened to me!” and “I told you so!” from a well prepared bunker as society collapses is every crank’s fantasy. I’m not going to psychoanalyze too deeply, but I do think there is something sociopathic about a desire to be right that is so strong it makes people, even subconsciously, kind of want a global disaster to happen. To the preppers and doomsayers in the room: you can object all day you don’t want it to happen, but I have spoken to many of you in real life, and I have seen the wishful glimmer in many of your eyes**.

So what does this belief tell us about Ron Paul in particular? Well we can say something additional about his beliefs based on the fact that he is running for president. As Will Wilkinson pointed on on twitter, his insurance against disaster tells us either Paul thinks he has no shot at being president, or that even if he becomes president he can do nothing to prevent economic doom. So which is it? This is actually an important question and one that reporters should be asking him.

Another thing I think you can arguably take from this relates to the re-emerging scandal of Paul’s racist newsletters. Racism, especially of the kind espoused by whoever wrote Paul’s newsletter, can be thought of as another crazy belief. It is my contention that crazy beliefs tend to be correlated. For any given crazy claim, people who hold another crazy belief are more likely to accept it, and those who hold dozens of crazy beliefs are way more likely to accept it. Because of this phenomenon, of I think it is more likely that Ron Paul actually believes the crazy things published in his newsletters than it is that Barack Obama believes the crazy things Reverend Wright said. Ron Paul is on the record as holding many crazy beliefs, whereas Barack Obama is not (that creating green jobs is something for policy to target may be wrong, but it’s not crazy).

Overall though, I think Conor Friedersdorf is correct when he argues that it is unlikely Ron Paul truly believes these crazy racist things given everything else we hear out of him. But I do think the odds that he does are higher than they would be if he didn’t hold all the other crazy beliefs, and they are higher than the odds Obama believes the crazy things Wright said.

I don’t think this is a partisan argument, and I think even Ron Paul supporters should agree with me. This is because you can believe something is true and still agree it is crazy relative to expert consensus, and you can also agree crazy beliefs, defined as such, are highly correlated.

*Yes, I am implying here that the tendency to insure even the tiniest bit against doomsday scenarios is a primarily male tendency.

**Then again, who am I to judge? Some part of me wants a zombie invasion to happen.

I want to reply to this Paul Krugman post on mercury regulations, but let me start with some important caveats. First, I have no idea if the new regulations are desirable, but if he’s correct that “it will save tens of thousands of lives every year and prevent birth defects, learning disabilities, and respiratory diseases” then I have a hard time imagining the costs exceeding these benefits. Also, Krugman is correct that there have been big successful environmental regulations in the past where the benefits clearly and largely exceed the costs. So to be clear: this post isn’t really about the mercury regulations at hand. What I really want to discuss is his more abstract and general point about when the best time to make these sorts of large regulatory changes is.

Krugman argues:

…if we’re going to have to scrap some power plants and replace them, it’s hard to think of a better time to do it than now, when the workers and resources needed to do the replacing would largely have been unemployed otherwise.

There’s certainly a valid point here. Spending like this, or any spending, in non-recessionary times has a crowding out cost, in that the resources being used to make new power plants would have gone to some other use and must be diverted. Labor and capital that had some other use must be bid away from those uses.

In a recession this is not necessarily true, as lots of capital and labor lays unused. Thus you are bringing unused inputs into use rather than diverting inputs from another use. Or at least you might, if you use the right inputs.

And here is one problem with big regulatory changes in a recession that Krugman ignores: the workers who are displaced from dirty factories may not be the same ones hired to build the new, cleaner factories. Are the skills necessary to build a new power plant the same as those necessary to run it? For that matter will clean power output replace dirty power output one-for-one, or will higher costs shift the supply curve leftward and increase prices? Both of these are possible reasons why workers at the dirty plant could become unemployed as a result of this policy.

And for these disemployed workers the costs are much higher if the regulatory change happens in a recession than if it happens out of a recession. I have voiced this concern about simplifying taxes right now: if you’re going to undertake large structural change that will require capital and labor to shift to different firms, and especially if it is to different industries, then those adjustment costs will be higher for the unemployed if the changes happen during a recession.

I am a big fan of creative destruction, and that’s kind of what we’re talking about when we talk about better policies causing industrial shifts. And even given the added costs of doing this in a recession, there are many policies where the benefits of doing it now outweigh the costs. This mercury regulation may very well be one of them. So too might tax simplification. Also the benefits of lower opportunity costs might outweigh the higher adjustment costs for workers. But we shouldn’t pretend that making big changes like this is better along every dimension during a recession than during times of healthy economic growth.

Kevin Drum writes

Karl Smith keeps telling me that [the aging auto fleet] is what’s going to spark a strong recovery in 2012. At some point, all those cars just have to be replaced, and that spending will drive improvement in the economy. Ditto for pent-up demand for houses and apartments.

I really want to believe this. I do, I do, I do. But with wages stagnant, credit tight, unemployment high, and the world economy flatlining, where’s the money going to come from?

The core answer comes from the Chairman of the Federal Reserve.

But the U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost. By increasing the number of U.S. dollars in circulation, or even by credibly threatening to do so, the U.S. government can also reduce the value of a dollar in terms of goods and services, which is equivalent to raising the prices in dollars of those goods and services. We conclude that, under a paper-money system, a determined government can always generate higher spending and hence positive inflation.

Of course, the U.S. government is not going to print money and distribute it willy-nilly (although as we will see later, there are practical policies that approximate this behavior).8 Normally, money is injected into the economy through asset purchases by the Federal Reserve. To stimulate aggregate spending when short-term interest rates have reached zero, the Fed must expand the scale of its asset purchases or, possibly, expand the menu of assets that it buys. Alternatively, the Fed could find other ways of injecting money into the system–for example, by making low-interest-rate loans to banks or cooperating with the fiscal authorities. Each method of adding money to the economy has advantages and drawbacks, both technical and economic. One important concern in practice is that calibrating the economic effects of nonstandard means of injecting money may be difficult, given our relative lack of experience with such policies.

In practice the functional limitation of non-standard methods of injecting money into the economy was the freak-out on the part of hard money advocates both on the FOMC, the policy world and amongst the chattering classes generally.

This dynamic creates the potential for a strong non-linearity in the economy.

When the natural rate of interest is below zero you drift along in a funk boosted only by productivity increases, but if the natural rate of interest creeps even the tiniest bit above zero you will blow it out of the water in roaring boom that returns you to full employment.

The reason is without non-standard measures Fed Policy can’t be stimulative. But, as soon as they are a little stimulative, that stimulus raises capacity utilization, employment and inflation, which in turn makes the exact same policy even more stimulative.

In the same way that the Fed needs to move the interest rate faster than the rate of inflation to stabilize inflation, if the Fed stays still in the face of a growing economy it will “destabilize” growth, which means growth will feed on itself.

In real life this it works like this:

As the vehicle fleet ages used car prices begin to rise. You can think of this as pushing down money demand for those folks in the market for cars over the next few years.

I prefer to think of it as raising the marginal return to capital which is equal to the interest rate.

In either case borrowing becomes a better idea. Healthy banks will then respond to that increase in consumer demand by increasing loans. Those loans create new money. In practice you will see excess reserves being turned into required reserves.

That money will then become income to car dealers and manufacturers, who will pass it along to employees or spend it themselves. Those folks will then have the income to allow them to take out further loans which becomes income to someone else, which allows further lending and so forth.

In particular, it will allow kids to move out of their parents basement which will push up rents which will encourage apartment developers to take out large loans.

As long as interest rates stay low this process will feed on itself rapidly increasing the lending and undoing this carve out.

I see that I do have some new readers. Gene Callahan says

Your “ridiculous” answer on obesity seems obviously correct to me — maybe insufficient, but fine as far as it goes — and the answer to the “puzzle” also obvious — adjust calories in and calories out until you are at a stable weight that you like. What is “ridiculous” about that?

The first issue is that saying one ate too much or too exercised too little is a non-answer. It simply takes the equation of motion and applies a normative frame to it.

I could say that rocks fall because they have too little resistance to the propensity to fall. This is a non-answer. It simply takes the analytical notion that resistance impedes motion and the observation that things fall and applies a normative frame to it.

How would we know if the resistance is too little? Because the rock fell. How would we know if the resistance is enough? Because the rock did not fall.

This tells us little, except that you are aware that things fall.

What we would like is something that takes parameter values and then tell us what result we should expect.

Now, the second part of Gene comment is slouching towards a model. He words it as instructions but if we recast it as a general framework we get something like this.

- Weight change is the residual of the choice variables calories-in and calories-out

- When people are unsatisfied with their weight the adjust one or both of these variables to make the residual positive or negative.

- When they are satisfied with their weight they adjust one or both of these variables to make the residual zero.

This has the virtue of being the beginning of a model. It has the vice of being at odds with the facts.

Lets set aside for a moment the issue how would we know if people are satisfied with their weight because I think it is too emotionally loaded. Instead, lets investigate the dynamics of this model with exogenous shocks.

First, imagine a young teenager who is temporarily at some stable weight and so presumably is satisfied and has chosen a residual of zero. Then the teenager hits a growth spurt. Under our model the teenager’s weight does not change.

He or she will grow taller but will not grow heavier. And, so BMI will fall and at the square of height change. If at this new BMI the teenager is unsatisfied with his or her weight then he or she may alter calories-in and calories-out to achieve a new weight, but in the absence of such conscious alteration weight will be fixed as height extends and so BMI will fall.

Does this appear to be what’s going on? Are teenagers accidently getting thinner as they grow taller and then moving to correct that?

Second, imagine a woman who gets pregnant. Again, under our model her weight will not change. Thus in the absence of conscious alteration of her caloric balance her core body will lose at least as much weight as the fetus and placenta gain. Indeed, she will lose more because the fetus and the placenta produce metabolic waste.

Now she may become unsatisfied with the loss of core body weight and move to alter caloric balance but in the absence of such unsatisfaction she will lose core body weight. Moreover, once the fetus and placenta exit the residual will exogenously rise and her core weight will move back to its original amount.

Does this seem at all like the patterns we observe?

Not to give away the show, but one might suspect that there is a mechanism which works to adjust either calories-in or calories-out in response to growth spurts and pregnancy. Our questions might be, does such a mechanism exist? How does operate? Is it present even when these events are not occurring?

There has been lots of handwringing over the issue of labor force participation and its decline during the Great Recession. The most straight forward comes from Mike Konczal

It’s always a challenge to find new and interesting ways to describe how terrible the labor market it. This is even more true as the unemployment rate is starting to decline though the employment-to-population ratio is roughly staying the same.

. . .

Even though the population is growing, the labor force has been flat for about four years now. Even worse, we don’t have a similar flatline anywhere else in the post-Great Depression to study to get some sense of the consequences of this. The recessions of the early 1960s and 1990s had flatlined labor force growth, but nothing like what we see how. How do we even go about understanding if and when it’ll converge back to trend?

I understand the intuition here, I really do. But, I just can’t get on this train.

We say markets work when every buyer can find a seller and every seller can find a buyer. Now, obviously in the intricate matching and commitment involved in the labor market this becomes complex.

Hiring a worker is a big deal. Why its such a big deal and why everyone doesn’t work for the equivalent of temp or consulting firms is a interesting question in itself. However, we do know that it in this world they do not. And, in this world hiring and firing workers is a process many folks don’t take lightly.

Nonetheless, when we are trying to analyze the distance of the economy from equilibrium, from a market characterized by equalized marginal utility products across resources, then I am really, really stuck to the notion that every seller finds a buyer and every buyer finds a seller.

In the absence of strong evidence our baseline conclusion has to be that something real about the economy is changing. That real thing might be unfortunate, but its not the same as the labor markets failing to clear.

I haven’t been keeping up with Scott Sumner lately, which is clearly my loss, for he has the following post.

The commenter Jason sent me a great Wittgenstein quotation, and I immediately knew I had to use it somewhere. It took me 10 seconds to decide where:

“Tell me,” the great twentieth-century philosopher Ludwig Wittgenstein once asked a friend, “why do people always say it was natural for man to assume that the sun went around the Earth rather than that the Earth was rotating?” His friend replied, “Well, obviously because it just looks as though the Sun is going around the Earth.” Wittgenstein responded, “Well, what would it have looked like if it had looked as though the Earth was rotating?”

It’s quotations like this that make life worth living. So I wondered what Wittgenstein would have thought of the current crisis:

Wittgenstein: Tell me, why do people always say it’s natural to assume the Great Recession was caused by the financial crisis of 2008?

Friend: Well, obviously because it looks as though the Great Recession was caused by the financial crisis of 2008.

Wittgenstein: Well, what would it have looked like if it had been caused by Fed policy errors, which allowed nominal GDP to fall at the sharpest rate since 1938, especially during a time when banks were already stressed by the subprime fiasco, and when the resources for repaying nominal debts come from nominal income?

OK, not nearly as elegant as Wittgenstein’s example. But you get the point.

Scott, goes on to make a slightly different point, but mine is this. Things always look like what they are. That is what it means to look like something.

The degree to which something looks like a bear is the extent to which its appearance matches the appearance of a bear. Thus a bear must look exactly like a bear.

What you mean to say is that I did not recognize it to be a bear. However, that is simply to say that you were unaware of what a bear looked like under those circumstances. Which in turn is to say that your assumptions about what a bear would look like under those circumstances were false.

Thus if you ask, why was it natural for you to assume that it was not a bear. And, you reply because it did not look like a bear, then you are saying it was natural for me to assume it was not a bear because I held false assumptions about the appearance of bears.

This tells you virtually nothing.

What you want to say is it was natural for me to assume it wasn’t a bear because in my previous experiences all bears were brown, yet this animal was white.

Or, it was natural for me to assume that the sun went around the earth because in my previous experiences treating the earth as my frame of reference allowed for the simplest laws of physics.

Or, in Scott’s case, it was natural for me to assume that the Great Recession was caused by the financial crisis of 2008 because in my previous experience using the overnight interest rate as an indicator of Fed Policy allowed for the simplest description of monetary economics.

After reading Kevin Drum, I got ready to go off on a long tangent about how if you just sit down and think about it you can tell that the standard explanation of how an airplane flies is shaky at best.

Interestingly, Mike then brings up an analogous scientific question that I was going to mention because I got it wrong for a very long time myself. Namely, how does an airplane wing work? I had long been under the impression that it had something to do with air traveling faster over the top surface, thus producing a vacuum and generating lift. But just like the orbit of the earth, which is quite obviously not a good explanation for the seasons since it’s summer in Australia at the same time it’s winter in London, this is quite obviously a lousy explanation for lift since planes can fly upside down.

But, I’ll resist the full tangent and try to make this more tolerable and productive.

At the core we always want to appeal to simplest and most direct law we can think of. The airplane is thrown “up”. Conservation of momentum then says something in the universe must be thrown “down.”

Our most likely candidate is the air. Then the answer to how the plane goes up must be the answer to how the air goes down. Does your standard explanation tell you that?

My larger point though is though is this

When analyzing things that have a political dimension – like economic policy – people suddenly become aware of the shakiness of the scientific lessons they have been taught. However, this pervades all of science. Its just that most of the time people don’t stop and ask.

In one case that I face all of the time, I talk to lots of folks about the obesity epidemic. The baseline assumption for people at all sorts of levels on this issue is that obesity results from people eating too much and exercising too little.

To explain that this is a maddeningly ridiculous non-answer is like pulling teeth. I am not going to do the whole dog and pony show but for those who might be hearing this from me for the first time ask yourself: how then do people wind up eating and exercising the “right amount.” Because, the answer to that question must be dual to how they might end up eating and exercising the “wrong amount” – whether too little or too much of either.

In any case this is repeated over and over again through pop science. Few people question ideas that if you stopped to question you would see that the standard answer is ridiculous and likely something someone told you so you would stop bothering them.

Indeed, we have textbooks full of “stop bothering me” answers to questions about how the world works. Still, many of these answers are quite useful for common purposes even if they don’t make any sense.

So, what you’ve uncovered with economics and public policy is not how a weirdly shaky discipline but simply how shaky our understanding of the world is generally. Or, at a minimum how complex and narrow the solid answers are.

Long time readers know that one of my big questions is why Plutocracy cannot be made to work. In particular, I wonder why society ruled by the owners of land combined with a “no serfdom” condition, doesn’t produce great outcomes.

We can argue over whether “no serfdom” is a stable equilibrium, but in the sweep of history so far all other arrangements are consistently beat out by liberal democracies which are a far, far cry from this.

Most of the standard answers to this I find interesting but unsatisfying, though if folks want to argue for them in the comments feel free.

Increasingly, however, I think it has something to do with the problem Paul Krugman outlines here.

One of the disadvantages of being very wealthy may be that you end up surrounded by sycophants, who will never, ever tell you what a fool you’re making of yourself. That’s the only way I can make sense of the farcical behavior of the wealthy described in this new report from Max Abelson:

Cooperman, 68, said in an interview that he can’t walk through the dining room of St. Andrews Country Club in Boca Raton, Florida, without being thanked for speaking up. At least four people expressed their gratitude on Dec. 5 while he was eating an egg-white omelet, he said.

“You’ll get more out of me,” the billionaire said, “if you treat me with respect.”

What I want to know is, how did these people get where they are with such incredibly thin skins? Can you become a Master of the Universe while screaming “Ma, he’s looking at me funny!” at every hint of criticism?

The lesson I would take is as follows. Profit or consumption maximizing incentives are just incredibly weak. We think we see consumption incentives in the general populace but we are really seeing status seeking. Folks earn or consume more in an effort to raise their status relative to others.

However, at very high income/status levels this has odd results. When Jaime Dimon or Leon Cooperman say that what they really want is to be loved, they mean it.

Indeed, twitter was ablaze a few weeks back over the fact that Jamie Dimon objected to his taxes being raised, but thought that he was already paying what Obama proposed raising his tax rate to.

This makes perfect sense if you note that Jamie doesn’t care about his tax rate. He cares about his taxes being raised. He cares about that because it sends a signal to him about how he is viewed in society and that really matters to him.

I see this in lobbying all the time. Because, I am a soulless technician who will faithfully advise anyone and everyone who asks I see the back rooms of opposing lobbyists all the time.

Here at the state level I can safely say that virtually no one has any idea what they are doing. That is, for the most part the lobbyist do not know and indeed are not particularly interested in what is in the best interest of their clients.

Further, this seems to stem from the fact that the clients are not particularly interested in what is in their best interests.

What they are very interested in is whether legislation is pro them or anti them. However, if you begin to talk about the economy as a complex system full of unintended consequences where anti legislation could be in their best interests their eyes glaze over.

Moreover, a very large number of business lobbyists are not even that interested in efforts that are pro or anti their business. They are more interested in legislation that is pro-business in general and that they perceive as being fair.

There are some notable exceptions but I will not name names.

My sense is that there is a huge but odd policy lesson here. I am still working to untangle what it is.

These are a few things I threw together to get a better sense of how I think about housing.

First, I take housing units completed and compare that to Census’s estimate of the number of new households formed each year. Thus, we can compare household growth to housing unit growth. Though, there is no demolition in this comparison.

As always one of the major things to notice is how the drift upward in housing units added was small compared to the bust. This is especially noticeable, when you see that over the whole period the deviation from household formation was not that extreme.

However, household formation has already turned around and we would expect it to make up lost ground unless there is a permanent change in living arrangements.

We can also look at a similar phenomenon by taking cumulative additions to the stock of both households and housing units. Then taking the ratio. Here I use a demolition percentage of 0.35% per year for two reasons. First, it gives me the near term estimate of about 200K demolitions per year that is standard. Second, it eliminates most of the trend drift in the ratio.

When you’re building up a stock from flow data it takes a while for the thing to settle down. Nonetheless, because specific dates are likely to be of interest to folks I’ll give you the whole series.

Now we can focus on the last few decades

Now, obviously the census data is kind of junky and the huge correction in household numbers we got in 2001 brought down the ratio to unlikely levels.

Nonetheless, we can see that we are currently crossing the lows seen in the early 90s and to the extent this imputation is decent we are not that far from 1-to-1.

Combined with the slowdown in household formation that is likely to reverse this is at least suggestive that there is a looming outright housing shortage.

From my Deep Dive at FP

Before anything else, the banks must be saved, most likely through an open-ended lending facility like the Federal Reserve’s Term Auction Facility (TAF). They must come before taxpayers, before pensioners, before the reforms that might transform southern Europe into a dynamic player in the global economy.

Not because it is fair or just or right. It is none of these things.

It must happen because we have constructed a global economy that has massive international banks at its heart. Money, banking, and credit lubricate the billions of transactions that happen around the world every day. If the global financial system collapses, so will trade.

Though, I lied. There will be lots of crying.

The series also contains pieces from some lesser known – but still quite good – economists like Barry Eichengreen and Larry Summers.

The whole thing is self-recommending – as in, I am recommending myself. And, I am an excellent judge of character, if I do say so myself.

I still see folks suggesting that the ECB’s Long Term Refinancing Operation (LTRO) be used as a Carry Trade for Sovereign Debt. Banks will buy up a bunch of Sovereign Debt, stick it into the and earn the spread.

However, you can’t really carry trade a marked-to-market fully collateralized loan because the collateral you have to post will move as spreads widen or shrink. This means that moving assets on the LTRO does not dispose of liquidity risk. If the price of the debt falls you still have to immediately come up with funds from somewhere.

If you borrow cheap and lend dear but retain all liquidity risk then this is just ordinary financing.

However, what you can do by moving more non-marketable assets on to the LTRO is free up liquidity, which in turn allows banks to play their traditional role in arbitraging away spreads.

I’ve received a lot of requests, mostly private, to explain Europe. In part, this results from a call I made on Italian Bond yields in late Oct to private correspondents.

However, much of it also has to do with my emphasis on the complete breakdown of ECB monetary policy and the similarities to 2008 in terms of money market shutdown. The fact, which I‘ve tried to call attention to, is that monetary policy as we think of it simply cannot operate without the money markets in general and the repo markets in particular. They are the marginal transmissions channel.

However, everything I know about the details of this situation come from Izabella Kaminska, which means that if you are not reading her you should be.

I have been off the case, but thankfully Izzy has not. She confirms that all of the ECB moves were about collateral crunch fears and concerns that it no longer had control over monetary policy.

Finally — and this is the clincher we feel — the measures as a whole were designed to give the ECB back some control of interest rates in private collateralised funding markets, which are now veering off official policy course:

Overall, all measures mentioned aim to ensure enhanced access of the banking sector to liquidity and facilitate the functioning of the euro area money market, thereby avoiding severe limitations to the real economy from a lack of financing possibilities. This also helps ensure that the official interest rates set by the ECB are transmitted in an appropriate way to the economy, and in that way help maintaining price stability in the medium term.

If that’s not a clue to the fact that the ECB is worried about losing control of transmission mechanisms, we don’t know what is.

I have been calling for some time for “a kick” in the US economy that would begin with rising auto sales and multifamily starts and then spread throughout the whole economy into a roaring boom.

Auto sales have been rising and now multi-family is moving higher

According to census, 5 unit or more starts are up 16% from last month and up 80% year over year. Right now, multi-family is pulling down 250K SAAR. I still think a rise to mulit-family at 1 million SAAR by late 2012, earl 2013 is completely realistic though unprecedented in the last 40 years

However, I caution that this is not yet the “kick” I am looking for These stats are all moving in the right direction but for a full on reinforcing cycle we need more. I would also like to see and end to government sector layoffs. This is something that I expected we would see by now, but it looks like we could have more layoffs going into early next year.